Kyle Hulett, Sygnia’s Co-Head of Investments

Amidst the looming spectre of elections in both the United States and South Africa, investors find themselves perched on the edge of uncertainty, anxiously pondering potential impacts on markets. In the United States, the stakes are high as the battle for a second term between incumbent Joe Biden and challenger Donald Trump unfolds, with each candidate embodying starkly different visions for the nation’s future. Meanwhile, a similarly tense atmosphere prevails in South Africa as the ANC grapples to retain power in a landscape of shifting alliances and ideological currents.

USA elections

The dollar, the reserve currency of the world, is driven primarily by global interest rate differentials, secondly by global growth differentials and then at varying times and by varying degrees by global risk appetite. Right now, the US elections are affecting the dollar, with the dollar strengthening as Donald Trump’s probability of winning increases. Trump is seen to be far more focused on US growth at the expense of the rest of the world, while Democrats are more cognisant of their NATO partners. Trump’s foreign policy is also more likely to result in escalating tensions, which would see a return to the risk-off environment – so the dollar would strengthen on both more US exceptionalism and the higher probability of global geopolitical incidents.

A Trump presidency would increase the risk of unexpected outcomes in all major regions, but the main potential for a policy shift is on Ukraine, where Trump is likely to cut off all aid. With Biden currently leading by 1% point, this election will be closely contested. Meanwhile, the Biden administration has implemented far fewer anti-trust enforcements than is typical for Democrats, and we may yet see an attack on US corporate greed as part of Biden’s election campaign.

South African elections

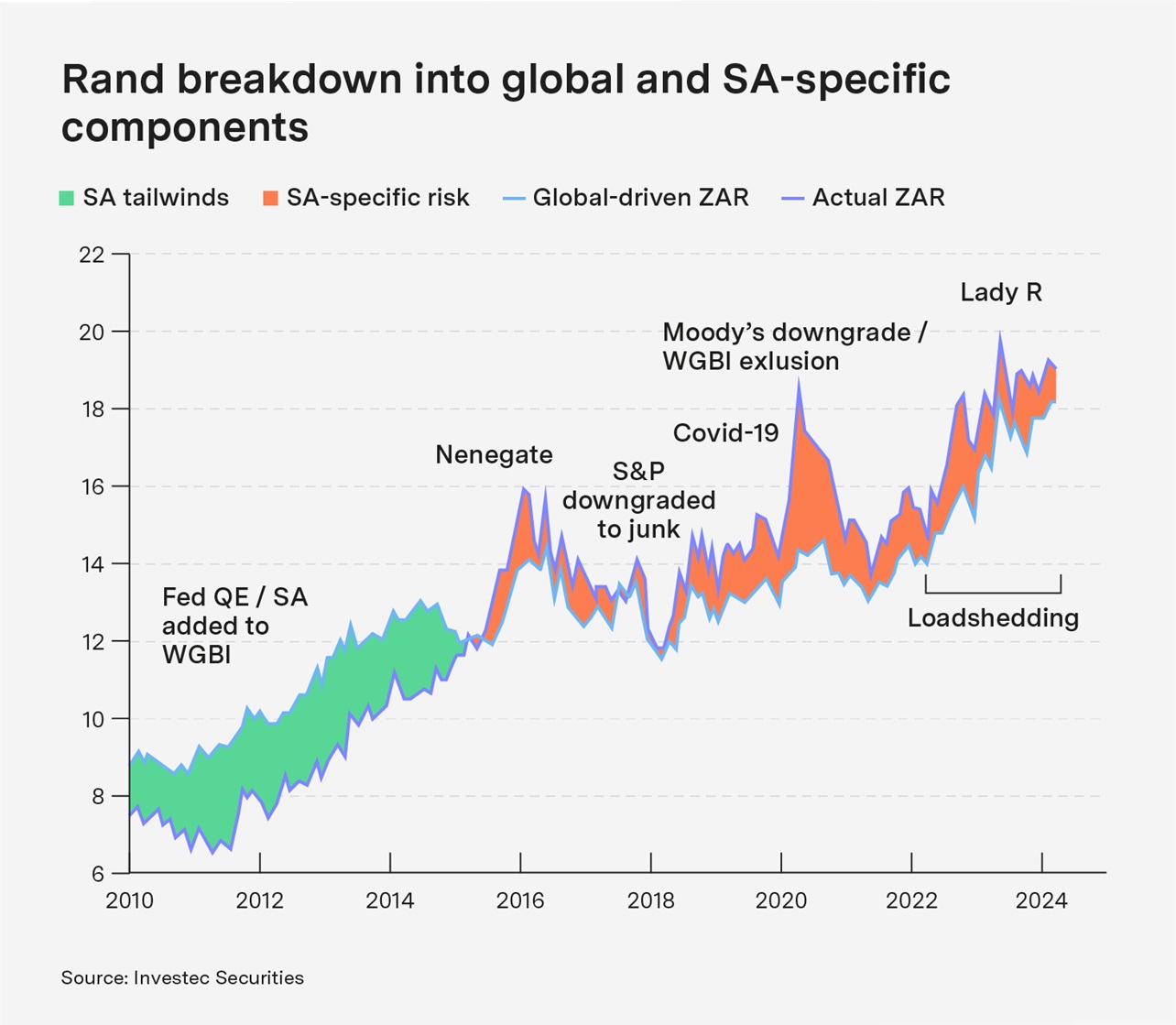

Looking at South Africa, three outcomes seem most likely. In the first, the ANC wins between 45% and 55% of the vote; if needed, it can form a coalition with one or a few of the smaller political parties. This is our base case and would be a status quo event – the ZAR would likely strengthen, possibly to R18, as the worst-case scenario fails to take place (Investec models show the rand has a R1 risk premium built in (see chart)).

In the second scenario, the ANC gets 40% to 45% of the vote and forms a coalition with the Multi-Party Charter or the DA. This could see a big SA rally on the back of escalated reforms, with the rand possibly strengthening to R17.

And in our final outcome, the ANC gets close to or less than 40% of the vote and forms a coalition with the EFF and/or MK parties, causing the rand to sell off dramatically to over R21 as more radical economic policies are put in place.

Chart: Rand breakdown into global and SA-specific components

Source: Investec Securities

ENDS