Adriaan Pask, Chief Investment Officer at PSG Wealth

Monetary policy, or more specifically the way reserve banks and policy makers manage interest rates, is the default mechanism for combatting inflation worldwide at the moment. However, the drivers of supply-side inflation (energy cost for example) and demand side inflation (cyclically higher prices due to strong demand) are fundamentally different. It begs the question, are interest rate hikes the right mechanism for fighting inflation in all environments?

This is a particularly relevant question in the South African context where higher interest rates are placing additional strain on an economy that is already grappling with growth.

South Africa’s unemployment and poverty statistics make for notoriously painful reading, yet interest rates are being increased to reduce prices. It is important to remember that monetary policy theory suggests that higher prices are reduced by muting what is assumed to be cyclically higher demand, but in South Africa we don’t have too much demand, we clearly have too little, the economy is under significant pressure. In fact, consumer confidence is back to the deep lows experienced during the COVID-19 pandemic, yet interest rates are at their highest levels in 14 years.

Graph 1: Local interest rate compared with consumer confidence

Source: FactSet (as at 3 July 2023)

Much of what South Africans are experiencing in the form of higher prices are related to issues on the supply-side. The inflationary effects caused by a lack of a steady and stable supply of energy globally has been exacerbated locally by the impact of electricity shortages and loadshedding. Businesses are increasing prices to offset the additional costs they have to incur, in the form of diesel for generators for example, a cost already running into the billions. In addition, a weaker currency has resulted in expensive imports. With economic growth under pressure, sales volumes are suffering, so businesses are in no position to take on additional margin pressure and pass these costs on to the consumers who are already feeling the brunt of increased costs. In such an environment, hitting the economy with higher interest rates is hardly going to do much to reduce the prevailing inflation drivers.

Even though there are other legitimate reasons for increasing interest rates beyond just fighting inflation it does seem that the interest rate mechanism is a rather blunt tool for reducing inflation. If there were additional policies and protocols in place to ensure that we manage supply-side issues more effectively, perhaps inflation would not be a problem right now. It is difficult to see how demand in our weak economy would be responsible for driving inflation.

If these additional policies and protocols are possible, it also implies that interest rates could potentially remain at lower levels. This in turns promotes economic growth, the only sustainable way to increase productivity, lift output, create jobs and reduce poverty. Not only is such an approach more supportive to consumer confidence and growth, but it is also positive from a business and investor confidence perspective. Countries that manage supply-side cost effectively are more productive, and also more competitive on the international stage. Second-round benefits then also pass through in the form of a stronger currency, which reduces input cost and so the virtuous cycle continues.

Another useful approach could be improved fiscal discipline. Cost of funding is increasing as the perceived risk of lending in South Africa has increased. By improving fiscal discipline, lending cost decreases, effectively reducing input costs.

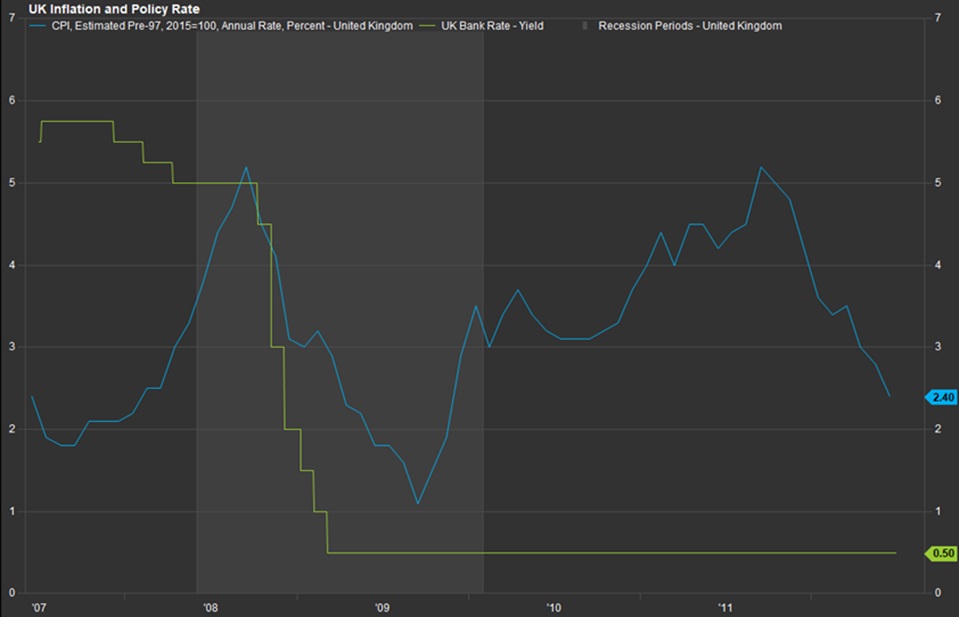

A good example of where monetary policymakers were willing to tolerate higher inflation while supply-side challenges subsided was when the United Kingdom experienced higher inflation and strained growth for periods between 2007 and 2012. Over this period inflation surged twice from 2% to 5%, high by developed market standards, yet the Bank of England either reduced interest rates or kept them stable to support economic stimulus.

Graph 2: History of UK inflation and monetary policy action

Source: FactSet

In fairness, we have seen some new developments that are helpful to reduce supply side inflation in South Africa. Some of the cumbersome application process steps imposed on IPPs have been reduced substantially to reduce energy supply constraints for example, and since then, we have seen this space accelerate in growth and create jobs. These polices will support our efforts to have stable and sufficient energy supply, and ultimately reduce inflation more structurally and sustainably. The challenge with such projects, however, remains the significant delays to bring new supply online, so measures that focus on the immediate environment can also play an important role. The temporary reduction of the general fuel levy by R1.50c per litre, for the period from 6 April 2022 to 31 May 2022 offers another example. These are just some examples of policies that drive prices lower, while supporting economic growth, not constraining it.

In the end we need a robust combination of practical monetary policy and strict fiscal discipline supported by business-friendly regulations, all of which need to focus on not only prevailing inflation, but also long-term inflation drivers.

ENDS