David Rees, Senior Emerging Markets Economist at Schroders

Bad economic news could eventually become good news for Chinese equities if the rising risk of outright deflation prompts the authorities to take more aggressive fiscal and monetary action.

Investors are crying out for a catalyst to trigger a turnaround in Chinese equities. While we have nudged up our growth forecasts, marginally better activity data seem unlikely to drive a major rally. Instead, the trigger is more likely to come from an about-turn in policymaking. In this respect, while there was little to cheer at the National People’s Congress (NPC) this week, bad news could eventually become good news if the rising risk of outright deflation forces Beijing into action.

Coming into this year we expected China’s economy to enjoy a mild pick-up in growth in the first half of the year. This was anticipated on the back of an improvement in manufactured exports along with the effects of some easing of policy. However, we did not think the improvement would last long, given that sluggish global growth was unlikely to support a strong export cycle, while policy support was relatively small.

Strong external versus fragile domestic picture

Our view from last summer that a recovery in the global manufacturing cycle would support China’s exports is starting to become more mainstream after the recent surge in manufacturing PMIs. Several leading indicators are now consistent with China’s nominal exports reaching growth of about 15% year-on-year (y/y) by mid-2024. Chinese exports have certainly got off to a good start to 2024, with growth in January and February much stronger than expected at 7.1% y/y. The January and February data is reported together to account for disruption around the annual lunar new year holiday.

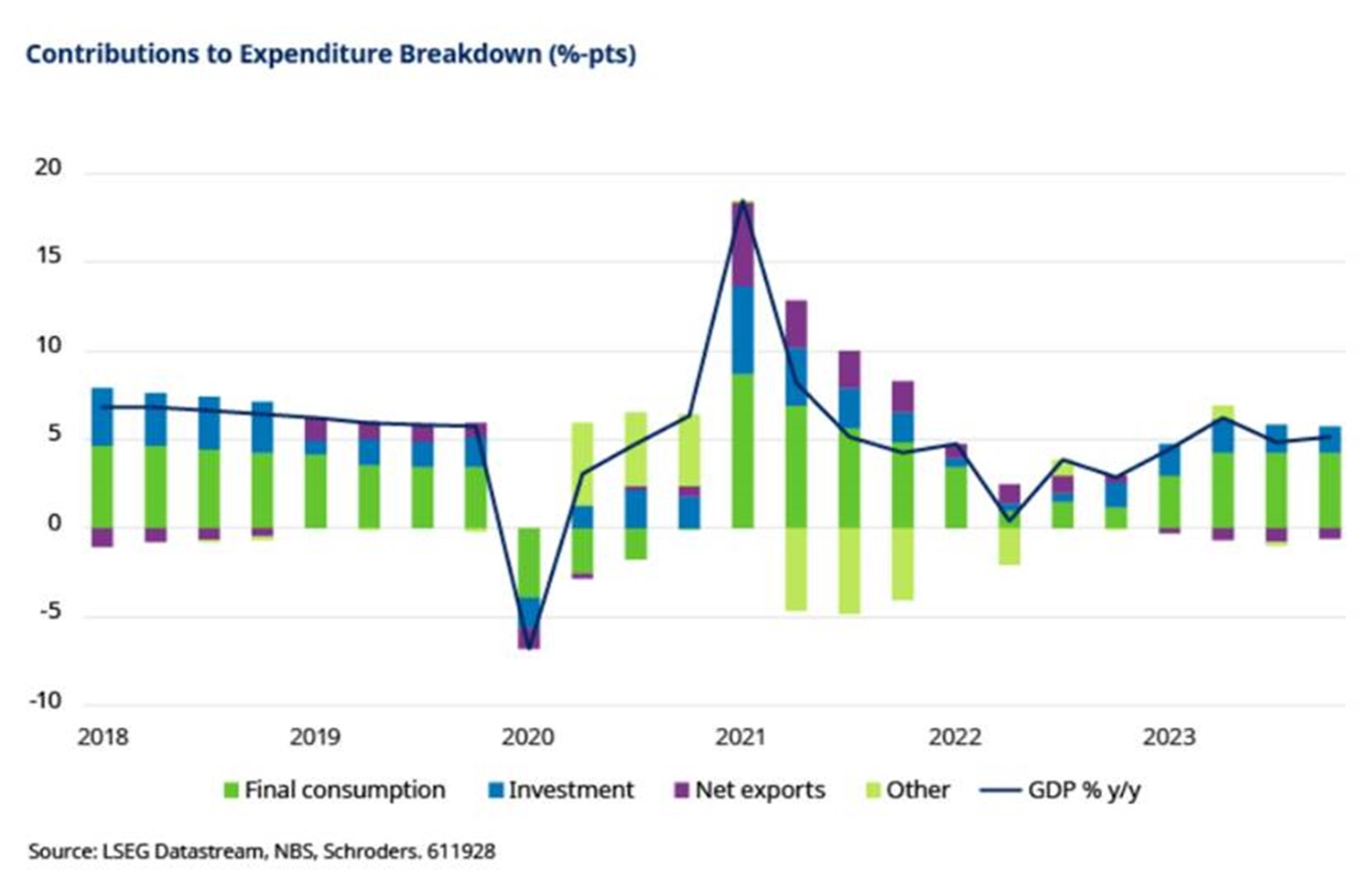

Meanwhile, we’ve significantly upgraded our global growth in our latest forecast round, particularly in the US where the consumer picture is robust. This implies that final demand will be strong enough to support further gains in exports than we had previously assumed. There is some evidence that Chinese firms are having to cut prices to clear output, with exports growing far more quickly when measured in volume rather than value terms. But while that is a concern for producer margins, it is good news for real GDP growth. As such, whereas net trade subtracted around 1 percentage point from GDP growth over the past year, it should start to add a similar amount in the months ahead.

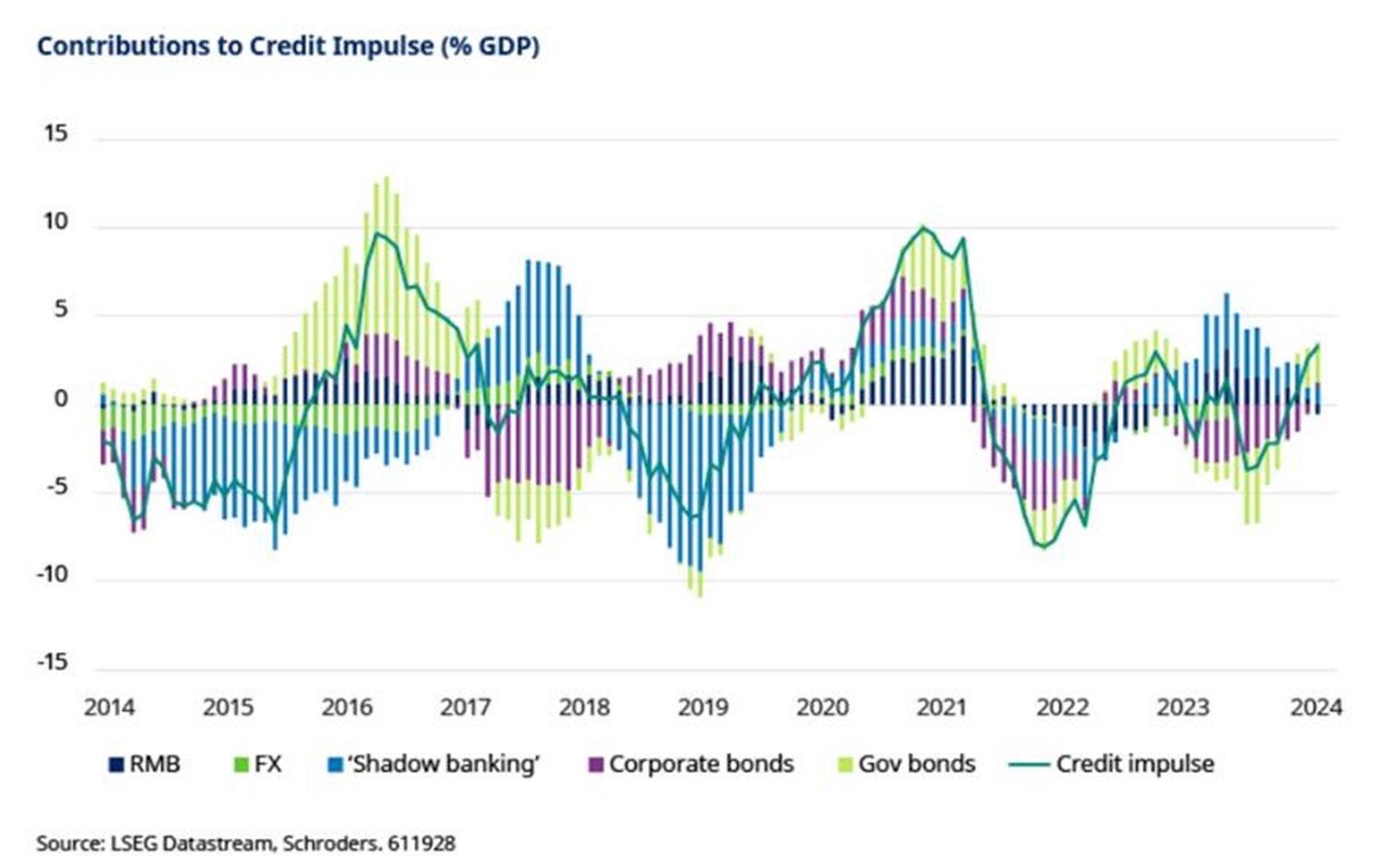

However, the domestic picture remains fragile. There has been an improvement in the credit impulse in recent months on the back of government bond issuance as looser fiscal policy has started to show up in the data. The poor state of local government finances suggests that this fiscal support will be less effective than in the past. But history shows that the credit impulse typically leads activity by nine months meaning that this should offer some support to activity in the months ahead. The issue is that stimulus has so far been piecemeal and the NPC signalled only a marginal planned additional easing of fiscal policy this year. As a result, this prop to growth is likely to fade later this year, exposing very weak underlying private sector demand for credit.

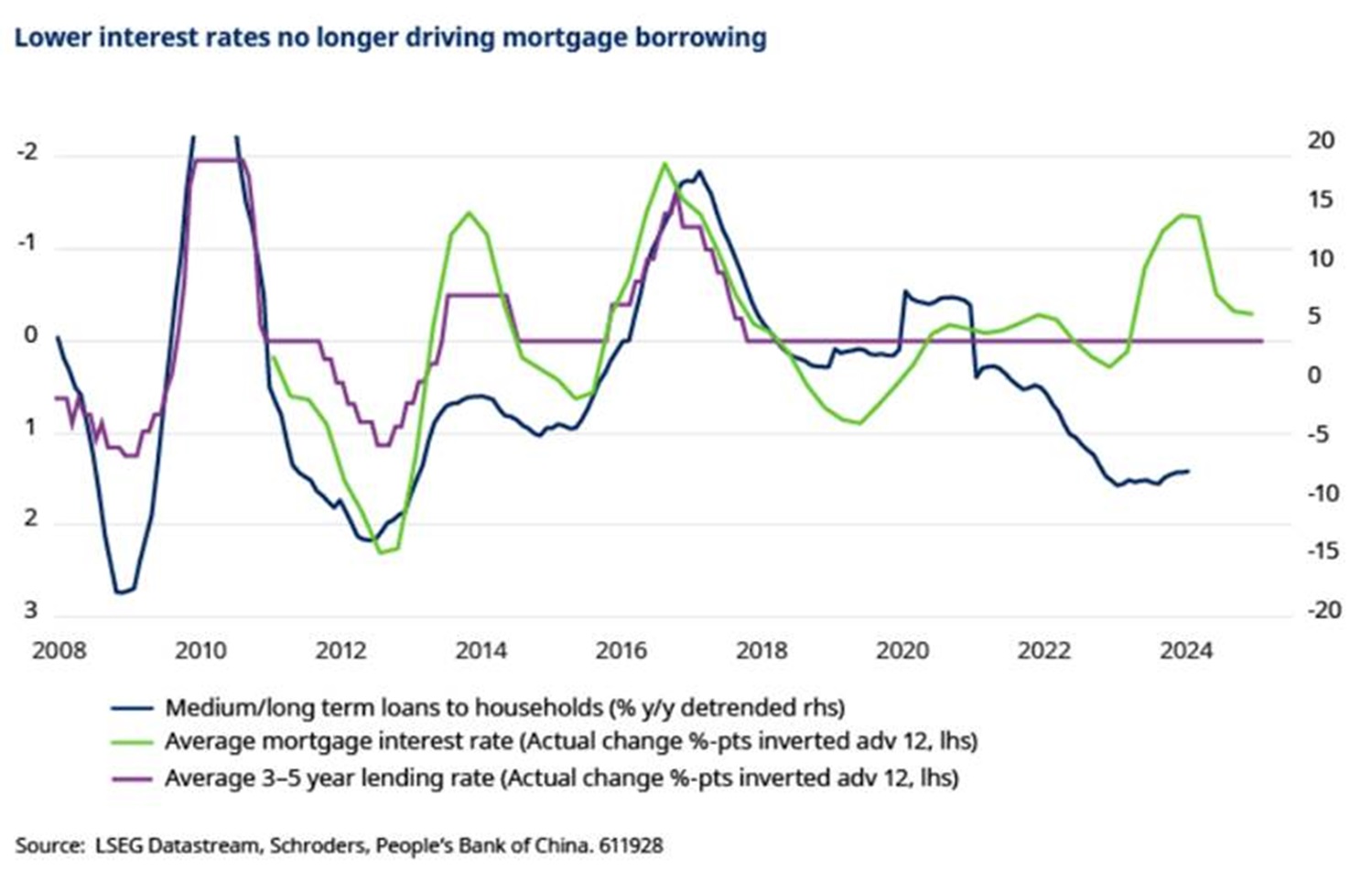

Weak private sector demand for credit can be traced back to the ongoing bust in the housing market. With homebuyers concerned by falling prices, still uncertain about the delivery of outstanding projects and deterred from buying property for investment, demand for credit has weakened substantially. Corporate bond issuance has fallen as real estate developers have run into trouble. Meanwhile, bank lending grew by 10.4% y/y in January, the slowest in almost two decades and within that, medium-long term loans to households, a proxy for mortgage lending, increased by just 1.9%.

Lack of demand for borrowing

The 25 basis points cut to the five-year loan prime rate in February, the largest single cut to the rate used to price mortgages, may offer some marginal stimulus to house purchases. But it is unlikely to solve the conundrum of weak demand for credit. After all, the link between lower long term interest rates and faster credit growth has completely broken down since the government’s crackdown on the housing market and speculative purchases of real estate. The cost of credit does not appear to be the limiting factor on loan growth at this juncture, but rather a lack of demand for borrowing.

With this in mind, the upgrades to our growth forecasts are not large and we suspect more easing would be needed to comfortably achieve the government’s target for growth of “around 5%” this year. We now project GDP growth of 4.8% this year and 4.5% in 2025, up from 4.5% and 4.3% respectively.

Deflation remains a concern

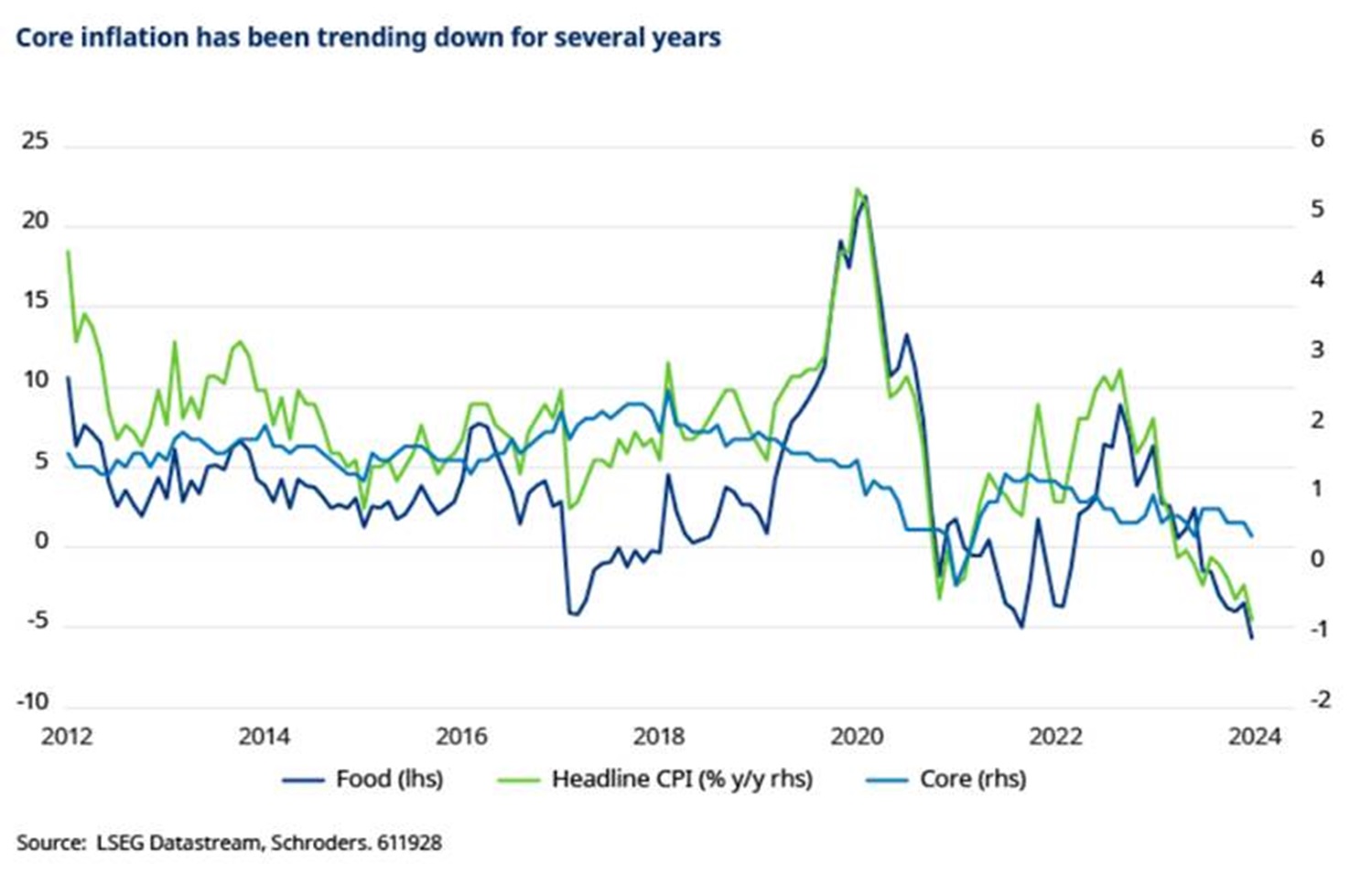

The soft domestic picture not only raises question marks about the durability of any pick-up in growth, but also China’s ability to continue to stave off deflation. Headline inflation has consistently fallen short of our expectations over the past couple of the years. Much of that has admittedly been due to food price effects, particularly of pork, that have been difficult to forecast with any accuracy. The January data saw inflation decline 0.8% y/y, which was the largest decline in well over a decade. This, however, needs to be taken with a pinch of salt given the shift in the timing of the new year holiday to February this year from January in 2023. But the bigger picture is that, beyond all of these distortions, core inflation has been trending down since 2017/18 and has averaged around 0.5% y/y over the past six months.

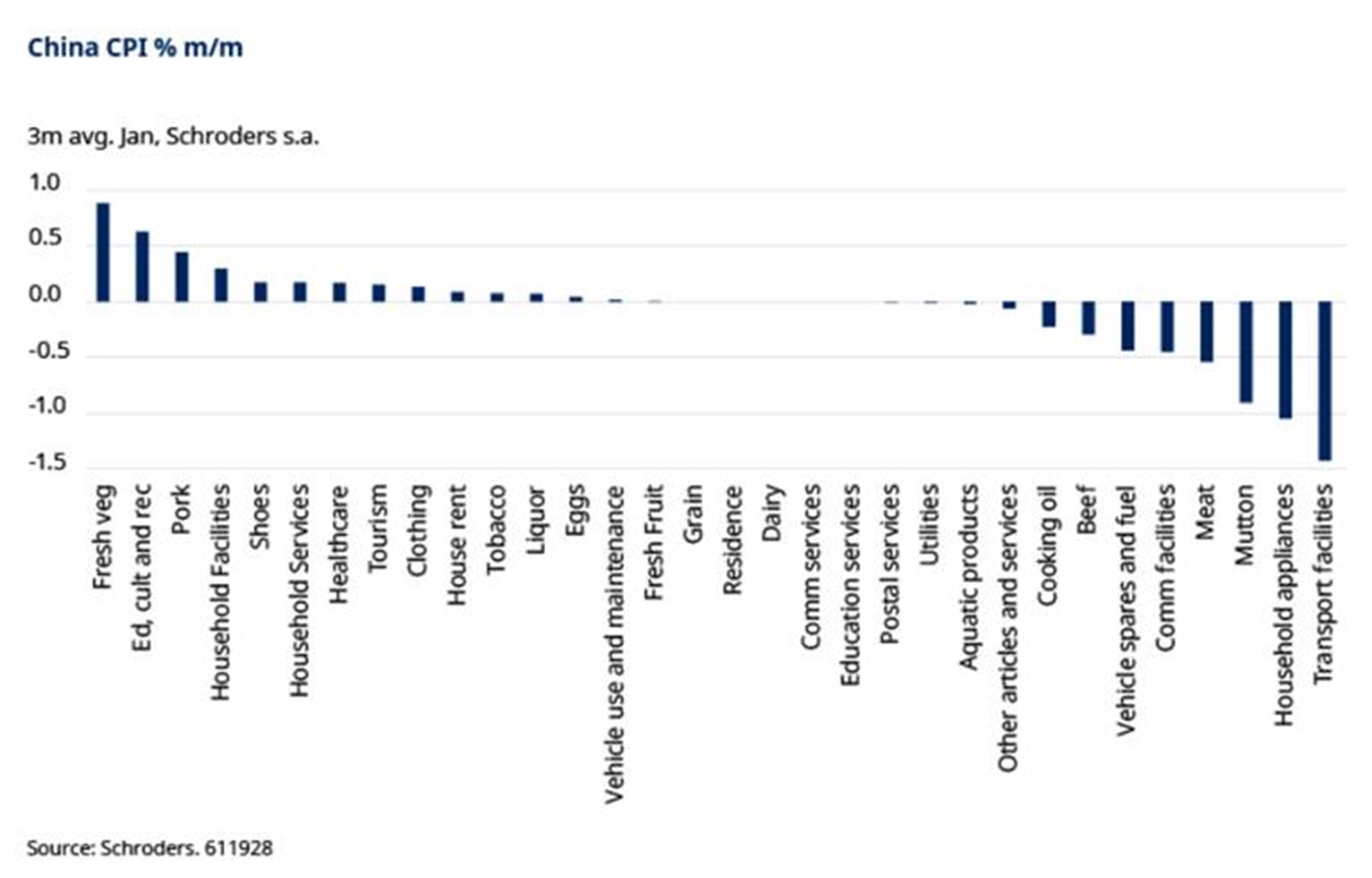

It makes sense to look at the month-on-month (m/m) changes in consumer prices for evidence of outright deflation. Unfortunately, these figures are not seasonally-adjusted, making them vulnerable to large swings, particularly around major events such as the new year holiday. In order to cut through this noise we have seasonally-adjusted the data ourselves and, acknowledging that this is unlikely to be perfect, analysed the three-month average of m/m changes through to January.

The data show that commodity price effects are still exerting deflationary forces on the economy, with several food components showing m/m declines along with some energy-related sectors such as vehicle fuel and utilities. Declines in the prices of household appliances also make sense given weak activity in the real estate sector, while some service sectors such as communication and transport facilities have seen prices fall.

The concern is that, in an environment of weak domestic demand and anecdotal evidence of weak labour market conditions and nominal wage cuts, inflation is being held up by a handful of service sectors. This becomes clear when we strip out increases in volatile food components. Policies such as “common prosperity” mean that healthcare and education – the latter which has seen a major clampdown on private activity – are unlikely to be a sustained source of inflation in the future. The ongoing bust and oversupply in the real estate market suggests that the household facilities, services and rent components aren’t likely to be inflationary either.

Authorities concerned about Japan-like debt-deflation spiral

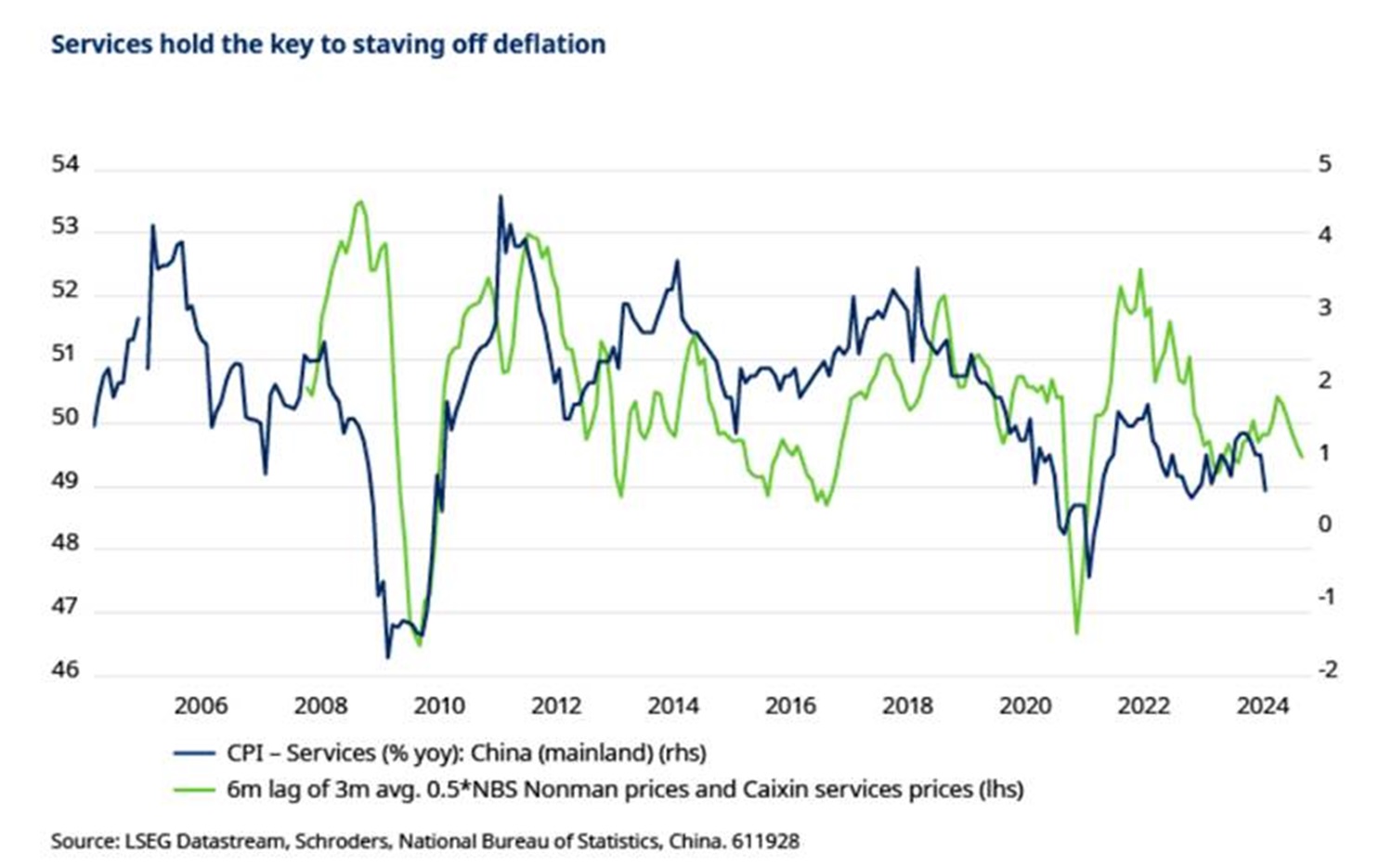

This appears to leave China in the precarious position of relying on culture, recreation and tourism to keep prices up and there is clearly a risk that pricing power in these sectors also starts to fade. For example, over the recent lunar new year holiday, while traveller numbers and aggregate activity were up on 2019 levels, spending per capita was down indicating that individuals are still retrenching.

Reliable leading indicators of services inflation in China are hard to come by. A weighted average of the output prices of the NBS non-manufacturing and Caixin services PMIs has historically given an indication of future turning points in services inflation but not the absolute rate of change. To this extent, the recent decline in the output prices components is concerning and we will be watching for any further declines in future PMI reports.

By all accounts, the authorities in China are concerned about the risks of sliding into a Japan-like debt-deflation spiral. The government’s 3% inflation forecast for this year seems wildly optimistic. Indeed, we have cut our projection for headline inflation this year to just 0.2%. And our low forecast suggests that monitoring the probability of outright deflation is likely to be one of the most important themes this year.

After all, in a rational environment, evidence of deflation at a time when the government expect a significant increase in inflation ought to induce a significant shift in policymaking to raise price pressures. This is something that we modelled in our latest forecast round in the “China stimulus” scenario, where we assume that broadening deflation pressures force the government into more aggressive fiscal and monetary action.

With investors crying out for a catalyst to trigger a turnaround in Chinese markets, there is a rising chance that bad news for the economy may start to become good news for markets. A return to structural reform would be the multi-year bull case. But a more substantial fiscal stimulus geared towards boosting demand would probably do the trick in the near term.

ENDS