Herman van Papendorp, Head of Investment Research & Asset Allocation and Sanisha Packirisamy, Economist at Momentum Investments

Economies at a Glance by Momentum Investments’ macro research team consists of an easy-to-read chartbook of what is happening in the economy and a snapshot of the index returns for the month.

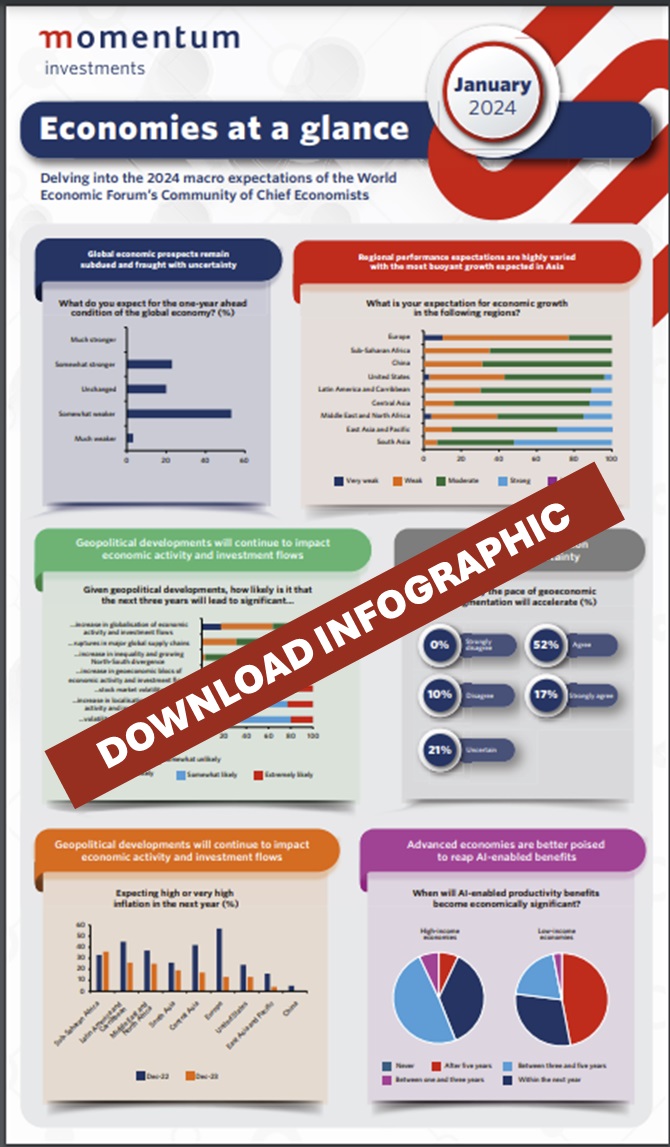

This month’s infographic features key expectations of the World Economic Forum’s Community of Chief Economists on growth, inflation and geopolitical developments for 2024.

Below is a short summary of what is happening in the world’s largest economies:

United States

In late December, markets were pricing in a more aggressive interest rate cutting cycle starting in March 2024 of nearly double the United States (US) Federal Reserve’s (Fed) indication, following the release of the committee’s decision to keep interest rates steady. At the meeting, the Fed indicated only three interest rate cuts of 25 basis points each for 2024 (implied by the ‘dot plot’ – the Fed’s collective expectations on interest rates over time). Financial markets have since pared back bets on interest rate cuts, with the Fed funds futures now pricing in six instead of seven cuts for the year, given stronger-than-expected payroll data and still firm gains in wage inflation. Higher costs arising from the Red Sea disruptions, triggered by Houthi militias, could add to inflationary pressures in the US, particularly given that 30% of cargo arriving on the East Coast of the US is typically routed through the Suez Canal.

In late December, markets were pricing in a more aggressive interest rate cutting cycle starting in March 2024 of nearly double the United States (US) Federal Reserve’s (Fed) indication, following the release of the committee’s decision to keep interest rates steady. At the meeting, the Fed indicated only three interest rate cuts of 25 basis points each for 2024 (implied by the ‘dot plot’ – the Fed’s collective expectations on interest rates over time). Financial markets have since pared back bets on interest rate cuts, with the Fed funds futures now pricing in six instead of seven cuts for the year, given stronger-than-expected payroll data and still firm gains in wage inflation. Higher costs arising from the Red Sea disruptions, triggered by Houthi militias, could add to inflationary pressures in the US, particularly given that 30% of cargo arriving on the East Coast of the US is typically routed through the Suez Canal.

Eurozone

The European Central Bank (ECB) kept interest rates steady for the third consecutive meeting in January 2024 citing stagflationary concerns. The latest projections from the ECB suggest that headline inflation will average 2.7% this year, before decelerating to 2.1% next year and 1.9% in 2026. Meanwhile, low export growth and tight financing conditions are expected to constrain economic growth to 0.8% this year and 1.5% in both next year and 2026. While the overnight indexed swaps are still pricing in six interest rate cuts for the year, ECB President Christine Lagarde warned about the upcoming wage negotiation season in April and May. Moreover, the Red Sea conflict could add to shipping costs and threaten a lift in oil prices, which could reduce the scope to ease monetary policy. This is in spite of continued downside risks to growth posed by the wars in Ukraine and the Middle East and the dampening effect of previous monetary policy tightening on domestic demand.

The European Central Bank (ECB) kept interest rates steady for the third consecutive meeting in January 2024 citing stagflationary concerns. The latest projections from the ECB suggest that headline inflation will average 2.7% this year, before decelerating to 2.1% next year and 1.9% in 2026. Meanwhile, low export growth and tight financing conditions are expected to constrain economic growth to 0.8% this year and 1.5% in both next year and 2026. While the overnight indexed swaps are still pricing in six interest rate cuts for the year, ECB President Christine Lagarde warned about the upcoming wage negotiation season in April and May. Moreover, the Red Sea conflict could add to shipping costs and threaten a lift in oil prices, which could reduce the scope to ease monetary policy. This is in spite of continued downside risks to growth posed by the wars in Ukraine and the Middle East and the dampening effect of previous monetary policy tightening on domestic demand.

United Kingdom

In December 2023, the Bank of England’s (BoE) Monetary Policy Committee (MPC) voted six to three in favour of holding interest rates steady for a third consecutive meeting. Despite the MPC’s tough stance against any discussions of interest rate cuts, overnight indexed swaps indicate that markets are pricing in a more aggressive easing stance, which includes four cuts this year. Slower inflation and wage growth have prompted investors to bet on a softer stance in monetary policy. Despite lagging its peer countries, significant progress has been made in reducing the rate of inflation in the UK. Although headline inflation inched higher to 4% in December 2023, it is significantly lower than the peak of 11.1% reached in October 2022. The BoE’s Monetary Policy Report for November 2023 projected that inflation would reach 3.1% by the fourth quarter of this year and come back within target to 1.9% by the fourth quarter of next year.

In December 2023, the Bank of England’s (BoE) Monetary Policy Committee (MPC) voted six to three in favour of holding interest rates steady for a third consecutive meeting. Despite the MPC’s tough stance against any discussions of interest rate cuts, overnight indexed swaps indicate that markets are pricing in a more aggressive easing stance, which includes four cuts this year. Slower inflation and wage growth have prompted investors to bet on a softer stance in monetary policy. Despite lagging its peer countries, significant progress has been made in reducing the rate of inflation in the UK. Although headline inflation inched higher to 4% in December 2023, it is significantly lower than the peak of 11.1% reached in October 2022. The BoE’s Monetary Policy Report for November 2023 projected that inflation would reach 3.1% by the fourth quarter of this year and come back within target to 1.9% by the fourth quarter of next year.

Japan

At the December 2023 meeting, the Bank of Japan (BoJ) appeared to be laying the groundwork for an interest rate hike. The minutes of the meeting divulged a debate among policymakers on the necessary conditions for phasing out stimulus, particularly as the BoJ’s conviction in its inflation projections has strengthened. The minutes further indicated an intention to discuss the appropriate pace of future interest rate hikes. In its October 2023 report, the BoJ forecasted core or underlying inflation at 2.8% for fiscal year (FY) 2024 (starting in April) and 1.7% for FY2025. Markets, via the overnight indexed swaps, are pricing in two interest rate hikes before the end of 2024. The minutes further noted that several members were in favour of sustaining yield curve control to support wage growth, while introducing more flexibility to reduce market speculation.

At the December 2023 meeting, the Bank of Japan (BoJ) appeared to be laying the groundwork for an interest rate hike. The minutes of the meeting divulged a debate among policymakers on the necessary conditions for phasing out stimulus, particularly as the BoJ’s conviction in its inflation projections has strengthened. The minutes further indicated an intention to discuss the appropriate pace of future interest rate hikes. In its October 2023 report, the BoJ forecasted core or underlying inflation at 2.8% for fiscal year (FY) 2024 (starting in April) and 1.7% for FY2025. Markets, via the overnight indexed swaps, are pricing in two interest rate hikes before the end of 2024. The minutes further noted that several members were in favour of sustaining yield curve control to support wage growth, while introducing more flexibility to reduce market speculation.

China

In support of a plunging equity market and fragile economic growth, the People’s Bank of China (PBoC) announced a 50-basis point cut in the reserve requirement ratio (the amount of cash banks must hold as reserves) in January 2024, following two cuts in the ratio in 2023. This move will add c.US$140 billion in cash into the banking system, increasing the capacity for lenders to extend loans against a weaker economic backdrop. The PBoC additionally noted new policies aimed at supporting loans for high-quality real estate developers. The policies will enable real estate firms to use bank loans pledged against commercial properties (e.g. offices or shopping centres) to repay other loans and to cover operating expenses. Many developers have defaulted on their debts after the government’s crackdown on excessive borrowing, with the largest, Evergrande, recently being ordered to liquidate.

In support of a plunging equity market and fragile economic growth, the People’s Bank of China (PBoC) announced a 50-basis point cut in the reserve requirement ratio (the amount of cash banks must hold as reserves) in January 2024, following two cuts in the ratio in 2023. This move will add c.US$140 billion in cash into the banking system, increasing the capacity for lenders to extend loans against a weaker economic backdrop. The PBoC additionally noted new policies aimed at supporting loans for high-quality real estate developers. The policies will enable real estate firms to use bank loans pledged against commercial properties (e.g. offices or shopping centres) to repay other loans and to cover operating expenses. Many developers have defaulted on their debts after the government’s crackdown on excessive borrowing, with the largest, Evergrande, recently being ordered to liquidate.

Emerging markets

Although growth in emerging markets (EMs) should continue outperforming that in developed markets by a notable margin, aggregate EM growth is likely to soften in the next quarters on the back of past monetary policy tightening, pressure on export markets and headwinds to Chinese growth posed by an ailing property sector. This could be partly offset by the localisation of supply chains as geopolitical tensions rise. EM central banks have played a leading role in shaping the global monetary cycle. They were the first to raise interest rates in response to emerging inflation concerns early in 2021. Similarly, EM central banks have also been the first to start cutting interest rates, starting around the middle of 2023. Countries such as Hungary, Brazil, Poland and Chile, were among the first to cut given their earlier aggressive hiking cycles. In contrast, there are a number of Asian economies that are likely to delay lowering rates or have a shallower cutting cycle given that they raised rates by less in response to a smaller inflation shock.

Although growth in emerging markets (EMs) should continue outperforming that in developed markets by a notable margin, aggregate EM growth is likely to soften in the next quarters on the back of past monetary policy tightening, pressure on export markets and headwinds to Chinese growth posed by an ailing property sector. This could be partly offset by the localisation of supply chains as geopolitical tensions rise. EM central banks have played a leading role in shaping the global monetary cycle. They were the first to raise interest rates in response to emerging inflation concerns early in 2021. Similarly, EM central banks have also been the first to start cutting interest rates, starting around the middle of 2023. Countries such as Hungary, Brazil, Poland and Chile, were among the first to cut given their earlier aggressive hiking cycles. In contrast, there are a number of Asian economies that are likely to delay lowering rates or have a shallower cutting cycle given that they raised rates by less in response to a smaller inflation shock.

South Africa

After hiking interest rates by 475 basis points since November 2021, the South African Reserve Bank’s (SARB) MPC decided to keep rates on hold at 8.25% for a fourth consecutive interest rate-setting meeting in January 2024. In the question-and-answer session, the governor stated that a sustained deceleration in the inflation trajectory to the midpoint of the 3% to 6% target was not yet obvious. As such, any easing in policy was not strongly considered, with the five-member committee unanimously agreeing to an unchanged stance. Even though the SARB expects global and local inflation to gradually moderate further, it retained a cautious tone, flagging serious upside risks to the inflation outlook and noting that a high level of uncertainty continued to cloud the economic outlook. The main risks to the inflation outlook remain local energy and logistic bottlenecks (which add to the cost of business operations), volatility in global food and oil prices (due to geopolitical strife) and the potential feed-through effect into higher wage growth in SA, particularly given the extent to which inflation expectations are backward-looking and could continue to reflect the effects of higher food and fuel prices with a delay. In our view, the SARB is likely to maintain its hawkish rhetoric to keep inflation expectations at bay. In line with the median expectation in the Reuters January Econometer, we expect the first interest rate cut of 25 basis points in the second quarter and are pencilling in two more cuts of the same magnitude for the remainder of the year.

After hiking interest rates by 475 basis points since November 2021, the South African Reserve Bank’s (SARB) MPC decided to keep rates on hold at 8.25% for a fourth consecutive interest rate-setting meeting in January 2024. In the question-and-answer session, the governor stated that a sustained deceleration in the inflation trajectory to the midpoint of the 3% to 6% target was not yet obvious. As such, any easing in policy was not strongly considered, with the five-member committee unanimously agreeing to an unchanged stance. Even though the SARB expects global and local inflation to gradually moderate further, it retained a cautious tone, flagging serious upside risks to the inflation outlook and noting that a high level of uncertainty continued to cloud the economic outlook. The main risks to the inflation outlook remain local energy and logistic bottlenecks (which add to the cost of business operations), volatility in global food and oil prices (due to geopolitical strife) and the potential feed-through effect into higher wage growth in SA, particularly given the extent to which inflation expectations are backward-looking and could continue to reflect the effects of higher food and fuel prices with a delay. In our view, the SARB is likely to maintain its hawkish rhetoric to keep inflation expectations at bay. In line with the median expectation in the Reuters January Econometer, we expect the first interest rate cut of 25 basis points in the second quarter and are pencilling in two more cuts of the same magnitude for the remainder of the year.

ENDs