Harry Goodacre – Strategist, Strategic Research Unit at Schroders

Equity investors increasingly need the mindset of a corporate bond investor amid the regime shift in interest rates and inflation.

In the previous environment of cheap, easily-available debt, and low default risk, equity investors rewarded companies that delivered growth. And in an era where central bank actions were used to offset economic weakness, balance sheet resilience was less in focus.

But the regime shift in interest rates and inflation has changed things. Equity investors will increasingly have to think more like corporate bond investors. In this article we take the novel approach of looking at how much credit risk investors are taking on when they invest in different equity markets and sectors.

Q1: What is the credit risk in different equity indices?

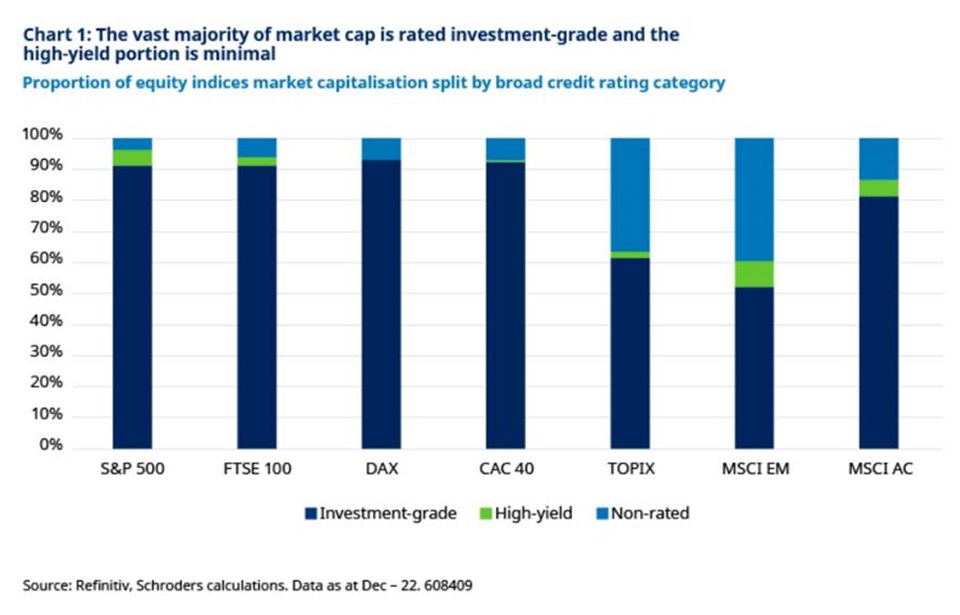

Reassuringly for equity investors, major equity markets are dominated by higher-rated, investment grade companies (those with a credit rating between AAA and BBB). More than 90% of the market capitalisations of the US S&P 500, UK FTSE 100, German DAX and French CAC 40 indices have an investment grade rating (Chart 1)[1]. The proportion with a riskier, high-yield/sub-investment grade rating is minimal, 5% or less.

Ratings coverage is lower in Japan but, even here, 97% of those for which we have ratings data are investment grade.

Companies without a rating fall into one of two camps. They either have no corporate bonds outstanding, or any bonds they do have are not rated by Moody’s, Fitch, S&P, or the Japanese Credit Rating Agency. This final one is a Japanese ratings agency which we included as coverage of Japanese bonds by international agencies is very low.

Ratings coverage is also lower in emerging markets. However, while less than 5% of developed stock markets have a sub-investment grade rating, 8% of emerging markets do (rising to 14% if you exclude those without a rating).

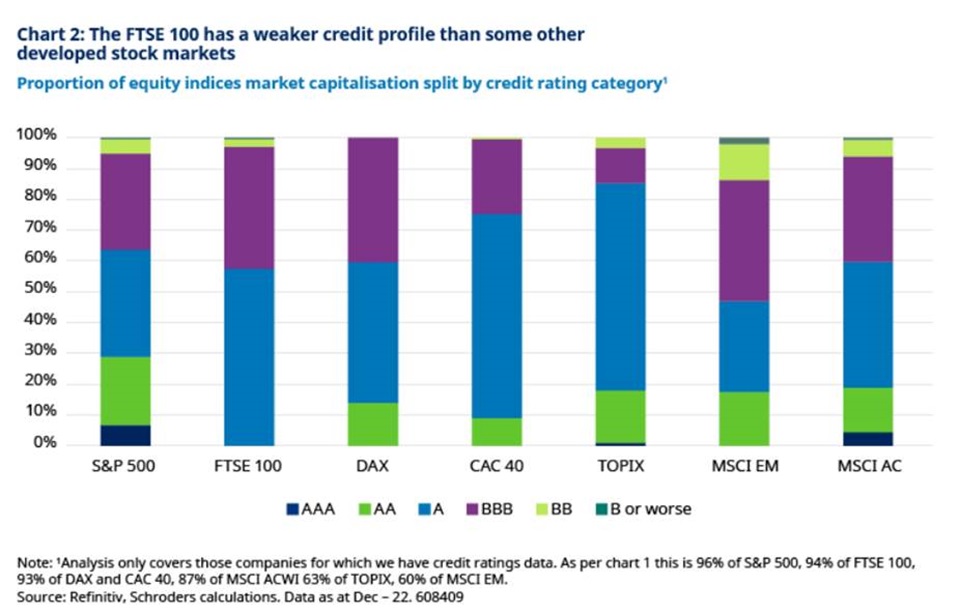

Digging a level deeper, differences start to emerge between developed markets (Chart 2). Almost 30% of the rated-S&P 500 has one of the top AAA or AA ratings. But none of the FTSE 100 does.[2] The UK stock market is riskier than other developed markets, from a credit ratings perspective.

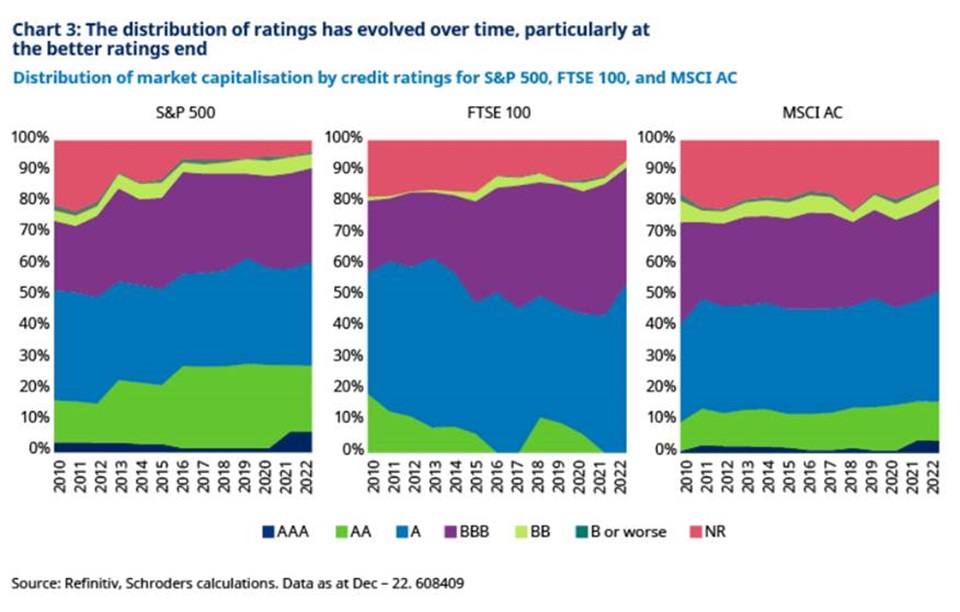

It’s not always been like this (Chart 3). The FTSE 100 has seen a decline in the AA and above rated portion due some large banks being downgraded. But the opposite is true for the S&P 500, and also MSCI ACWI. They have seen an increase in the portion rated AA and above, reflecting the presence of large highly rated technology companies.

Q2: Do some sectors have stronger credit ratings than others?

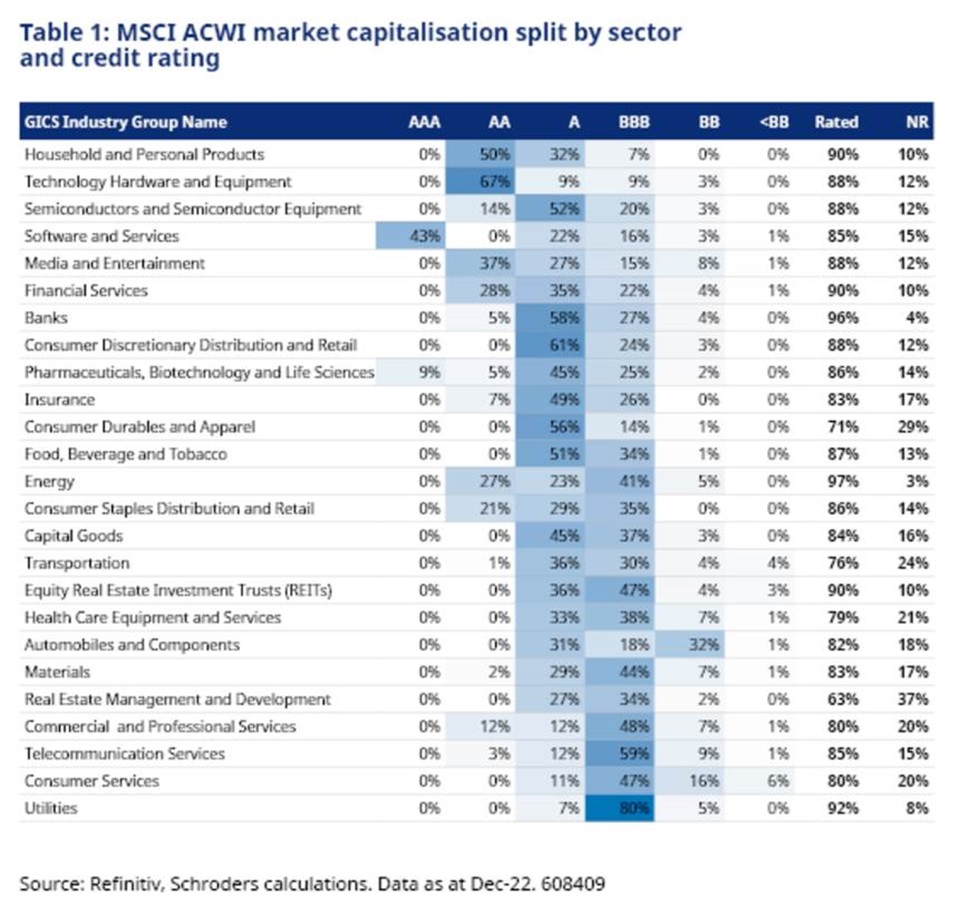

There are even bigger differences between sectors than between stock markets (Table 1). The household & personal products and technology hardware & equipment sectors of MSCI ACWI each have over three quarters of their market capitalisation rated A or higher. Whereas sectors such as utilities, telecommunication services, and consumer services each have much less at these stronger ratings. And automobiles & components stands out as the sector with the highest proportion of market capitalisation that is high-yield, with 32%, followed by consumer services.[3]

The level of credit ratings coverage also varies a lot. Within MSCI ACWI, the banks sector has the highest with 96% of market capitalisation with a rating, while real estate management & development has the lowest at only 63%.

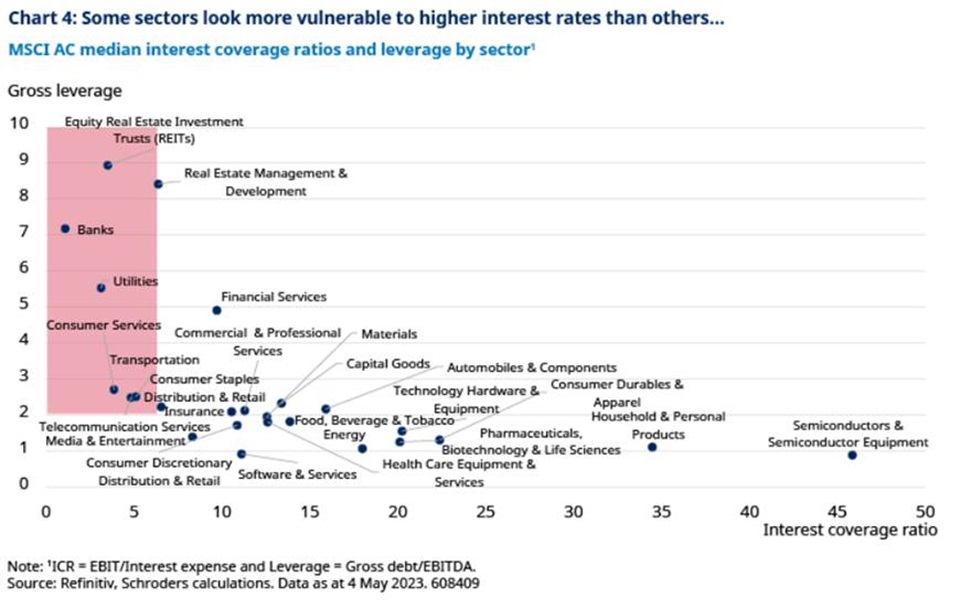

Q3: Are some sectors more vulnerable to the higher interest rate regime than others?

Those sectors where interest coverage ratios are lower and leverage is higher could be considered more vulnerable to the shift to a higher interest rate regime. Albeit the speed at which each sector is impacted by higher rates will depend on the balance of fixed and floating rate debt, and the horizon over which fixed rate debt is needing to be refinanced

Consistent with their investment grade status, most sectors of MSCI ACWI have relatively high levels of interest cover, suggesting default is low. However, there are differences in relative risk between sectors.

Leaving aside sectors which have more complex funding structures (such as banks, financial services, and REITs), the corporate sectors which stand out as having the combination of high leverage and low interest coverage ratios are transportation, telecommunications services, and consumer services (Chart 4). These are the same sectors which have relatively weaker credit ratings.

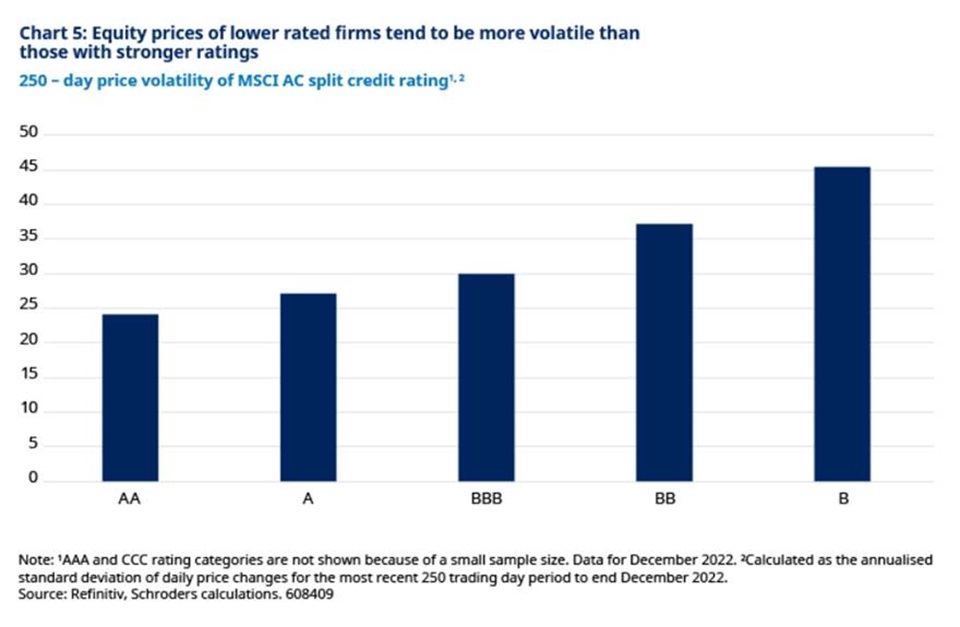

Q4: Are companies with poorer credit ratings riskier for equity investors?

Yes, when it comes to volatility. B-rated companies have been more volatile than BB-rated companies, which have been more volatile than BBB-rated companies, and so on (Chart 5). Equities with lower credit ratings have tended to be more volatile than those with better ratings, which has persistently been the case over time.

What this all means for equity investors

Valuations and their sensitivity to discount rates will always matter. But with central banks now contending with an era of inflationary pressures, monetary policy can no longer be assumed to mitigate weak growth. So corporate fundamentals will be more in focus. Companies with weaker credit ratings, higher leverage and/or lower interest cover could start to come under pressure as they face up to the more expensive cost of debt in today’s world. Even if ultimate default risk may be relatively low, the market differentiates between the relative risk of companies from this perspective. More credit risk equals more volatility.

The UK and emerging markets have relatively weaker credit ratings, while the US is starting from a position of relative strength. At a sectoral level, transportation, telecommunications services, and consumer services are ones to keep an eye on. Those equity investors who are able to think more like corporate bond investors will be in a stronger position to navigate the new economic regime we have entered.

ENDS

[1] We consider ratings from Moody’s (long-term issuer rating, senior unsecured rating, corporate family rating), S&P (long-term issuer rating), and Fitch (long-term Issuer default rating). For Japanese indices we take into account ratings from Japanese Credit Rating Agency. Where there is a split rating we take the lowest rating but the conclusions would be broadly similar if we used the highest rating.

[2] If we were to use the highest credit rating there would be some AA market capitalisation in the FTSE 100 but the conclusion of weaker ratings than the S&P 500 would be similar.

[3] Note that not all ratings providers agree on companies’ ratings. In situations of conflict we have taken the lower rating. If we were to use the highest rating then the proportion of the Automobiles & Components sector classed as high-yield falls significantly to only 5%, reflecting the presence of a company with a large market cap that has a split rating.