Richard Damming, Senior Investment Director at Schroders

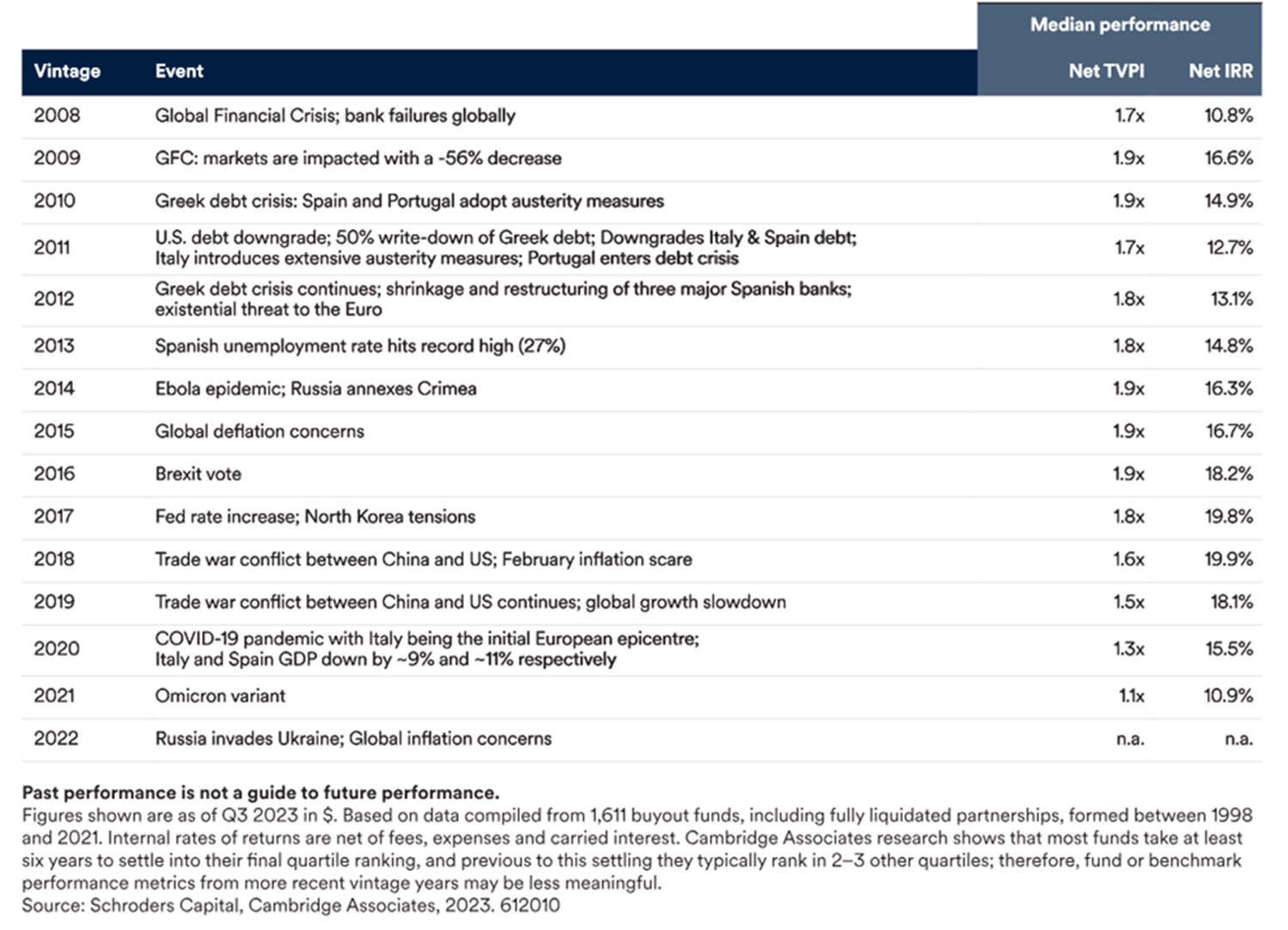

While inflation is moving steadily lower, we believe the secular shifts of deglobalisation, decarbonisation, and demographic change – the “3D Reset” – will keep inflation and interest rates higher for longer. With the added challenge of geopolitical conflicts, many investors are reassessing their private equity allocation. But almost every year since 2008 has involved a crisis for investors in private equity.

And yet, double-digit returns have been earned by global private equity investors in every single year over this period (figure 1), whatever the global economy and markets have thrown at them, recessions included.

Performance in recent years is less meaningful as funds have yet to mature but investors in 2008-19 vintages have earned an average internal rate of return of 16% a year and got back an average of 1.8 times their money. This has far outpaced GDP growth.

One reason why performance has been so resilient is that private equity funds benefit from “time-diversification”. Capital is deployed over several years, rather than all in one go. This reduces sensitivity to market events and means that the concept of market timing doesn’t make sense when it comes to allocating to private equity. Likewise, private equity investors are long-term asset holders without pressure to divest if market conditions are not conducive to return maximization.

Rather than being a time for investors to worry about allocating to private equity, recession years have been a pretty good time to invest. Funds raised in bad times can pick up assets at depressed values as a recession plays out, and then exit later on in the recovery phase when valuations are rising.

There are many value-drivers that go well beyond economic or domestic industry-specific growth. For example, mergers and acquisitions/consolidation, technical innovation, professionalisation, and export-oriented business models. These can generate value even against a challenging macroeconomic backdrop.

But a tailwind from rising leverage and falling borrowing costs is ending.

One factor that has been supportive through this period is cheap, easily available debt. This has helped more leveraged transactions “juice” returns, especially when accompanied by rising valuation multiples.

With long-term inflationary pressures created by the 3D Reset, we believe the era of ultra-low interest rates is behind us. Debt will cost a lot more and leverage levels will be lower because higher interest costs will make it less appealing.

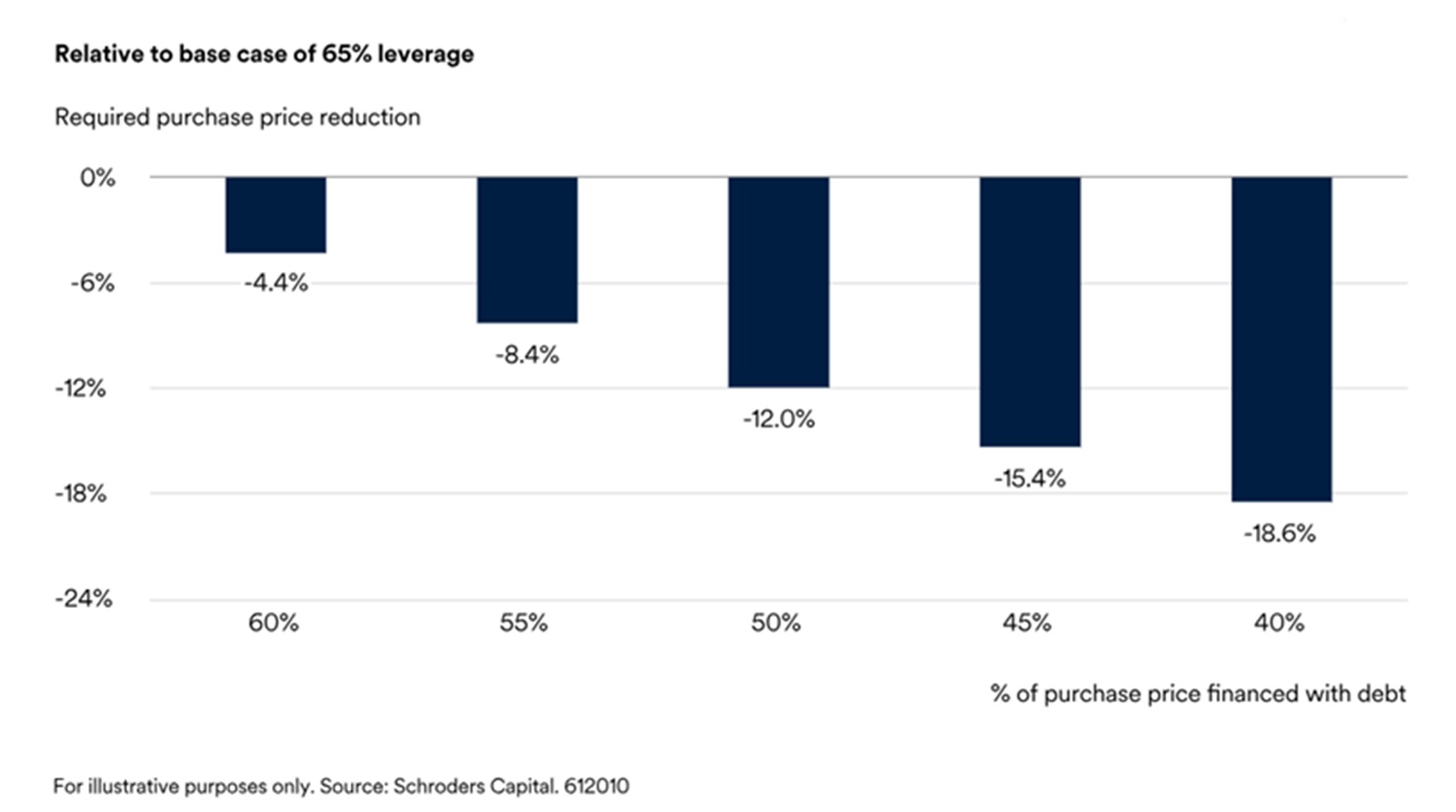

But, offsetting this, falling valuations mean that it costs less to acquire a company today than it would have done 12 months ago. And the price reduction required to offset a lower level of leverage and leave returns unchanged is less than you might think. A 12.5% reduction could be enough to offset a reduction in leverage from 65% to 50% without impacting returns, all else being equal (see worked example).

One change is that the types of strategies that look set to be more successful could look quite different to those that succeeded in the past decade. With leverage and rising multiples unlikely to propel returns, there could be a sweet spot for strategies focussed on revenue growth and profit margin improvement.

For example, expansion of product lines or geographic footprint, and professionalising management to improve profit margins. This is all easier to do among small- and medium-sized, often family-owned, companies. At larger companies, which have often been through several rounds of private equity or institutional ownership, it is much harder to add the same value.

Buy and build strategies are also well positioned to do well, with opportunities to buy smaller companies, expand, improve profitability, and then sell at the valuation premium that larger companies go for compared with smaller ones.

Worked example:

Crudely, let’s assume a company’s enterprise value grows by 8% a year. So, if it’s worth €100 million on day one, it’s worth €146.9 million after five years (for the purpose of this analysis it is irrelevant whether this comes from revenues, margins, or multiple expansion). At that point it is assumed that you exit.

If the purchase is 65% financed by debt, then that covers €65 million, with the equity investor putting up the other €35 million. After five years, the equity investor’s stake is worth the sale price net of outstanding debt which, for simplicity, I’ve assumed is still €65 million. That gives them €81.93 million, which works out as an annualised return of 18.5% on their initial €35 million investment.

But what if, in today’s new world, you can now only get 60% debt financing. Or 55%. Or less? Figure 2 shows how much cheaper the purchase price would need to be for your return to be the same as in the original case. This assumes you can still sell it for the same projected value of €146.9 million in five years’ time. For example, if only 50% debt financing was available, entry prices would have to fall by 12% for investors to still earn an 18.5% return. This is perhaps less than many people might expect.

How much of an entry price reduction is needed to offset lower leverage and leave returns unchanged?

What about inflation higher for longer?

The combination of ageing populations, slowing globalisation, and the transition to more expensive energy sources are set to keep inflation structurally higher. This is a global problem which is affecting all asset classes, across equities and bonds, public markets, and private ones. Private equity is not immune. As well as impacting leverage, as described above, the profitability of many companies will come under pressure as their cost base increases.

However, not all will suffer. Those which are able to pass on higher costs into higher prices will prove more resilient. Those with weaker market positioning or whose products and services are more easily substitutable will struggle. This will increasingly differentiate between successful companies and successful private equity investors in the years ahead.

Conclusion

Investors in private equity need not fear the implications of structurally higher inflation and rising geopolitical conflict. Although the global economy continually faces challenges, returns have been strong through thick and thin. The tailwind from cheap interest rates may be fading but the ability to buy companies for less will go a long way to offsetting that. Funds focussed on smaller and medium-sized companies look to be particularly well positioned to navigate the times ahead.

ENDS