George Brown, Economist at Schroders

You’re hot then you’re cold

You’re yes then you’re no

You’re in then you’re out

You’re up then you’re down

Pop star Katy Perry might have been singing about an indecisive lover in her 2008 hit single, but Hot n Cold could just as easily be about this year’s conflicting US labour market data. While several indicators have pointed to a deterioration, an equal number have suggested the exact opposite. Further adding to the confusion has been sharp revisions to some series, which have occasionally flipped the narrative.

This presents a major headache for the Federal Reserve (Fed). Its dual mandate of maximum employment and stable prices means the labour market is perhaps the single most important consideration. And so this year’s mixed data raises the risk of a policy error by the Fed, either by neglecting to raise rates enough or alternatively by overtightening.

Take May’s jobs report. While some 339,000 workers were hired over the month, the unemployment rate climbed 0.3 percentage points to 3.7%, even as the participation rate remained at 62.6%. Divergences between the two do occur from time to time, but very rarely to this extent. So why was there such a dichotomy between them?

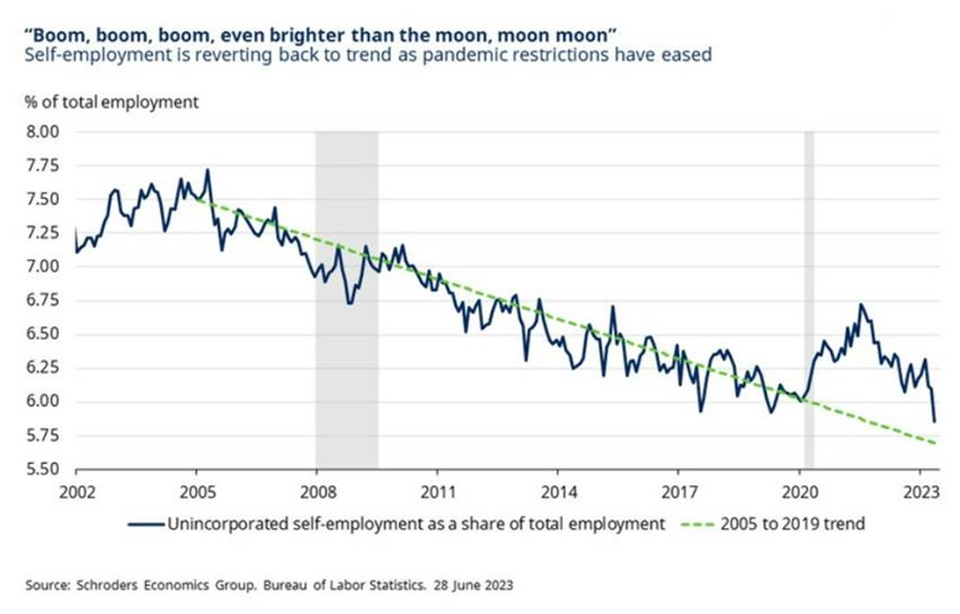

For one, two separate surveys are used to calculate the jobs and unemployment figures. The latter is derived from the survey sent to households, which is more representative than the payrolls survey filled out by non-agricultural employers. For instance, the household survey captures those who are self-employed. Of this cohort, the number of those that are unincorporated (i.e. working for themselves in a non-corporate entity) fell by a sharp 412,000 in May.

While this may appear alarming, context is important. An outsized number of Americans started their own businesses over the pandemic. Many of these were women, which may be linked to the increased burden of at-home childcare during lockdown. And so, now that restrictions have eased, it is unsurprising to see a correction back to pre-pandemic levels and trends.

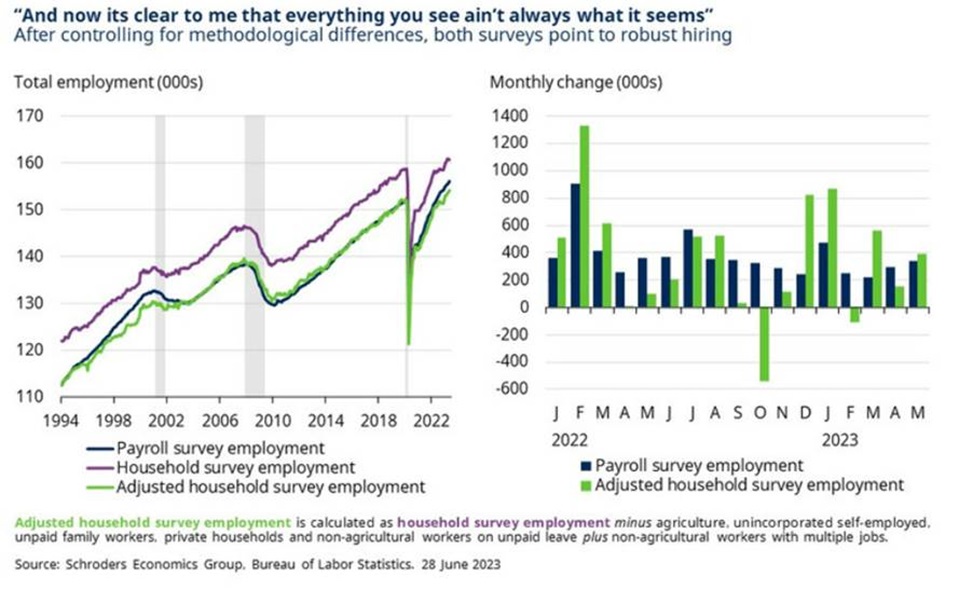

Also, the household survey has a much smaller sample size than its payrolls peer. To be considered statistically significant, employment has to rise or fall by 600,000 over the month, over four times the 130,000 threshold for the payrolls survey. And so the 310,000 fall reported by the household survey in May could well be completely wrong. In fact, employment may actually have risen.

Such a possibility is underscored when the household survey is adjusted for the payrolls methodology, which enables a near like-for-like comparison between the two. On this basis, both surveys point to a robust pace of hiring, with the adjusted household survey actually pointing to nearer 400,000 job gains over the month.

Even so, the rise in unemployment can’t be so easily discounted. The rise is in excess of the sampling error, meaning it should be at least partially genuine. Still, it may prove short-lived if the pace of hiring is maintained. Since the Fed started raising rates last year, it has jumped 0.2 percentage points on three previous occasions only to unwind over subsequent months.

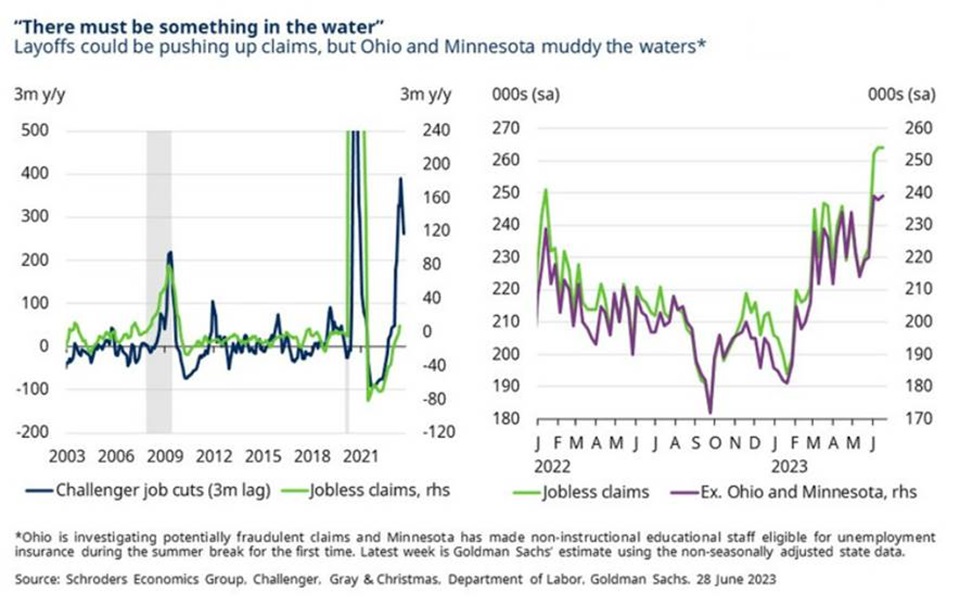

But perhaps this time is different, particularly as other indicators are similarly consistent with rising joblessness. Layoffs have risen sharply from a low base since November according to Challenger, Gray and Christmas. And this appears to be corroborated by initial jobless claims, which have risen in recent weeks to the highest since October 2021.

Even so, Ohio has accounted for a large share of the recent rise and officials have reported that they are investigating widespread fraudulent filings. If you are getting a feeling of déjà vu, it is because Massachusetts suffered a similar issue earlier this year, which was then revised away as these were weeded out. Further muddying the waters is that Minnesota has expanded its eligibility for claims.

Stripping out these two states, claims in the remaining 48 have trended upwards but not nearly to the extent as currently suggested by the national picture. And even this may have been distorted by seasonality issues, such as the recent Memorial Day holiday. These issues are set to continue until mid-July given the variability in annual automotive retooling and Independence Day.

Alongside this, wage growth has been gradually moderating. Average hourly earnings are running at 3.8% on an annualised trend basis, although higher than it was before the pandemic, it is nevertheless a substantial easing from its peak of 6.2% early last year. Particularly as hours worked have been trending down as of late, despite the robust hiring.

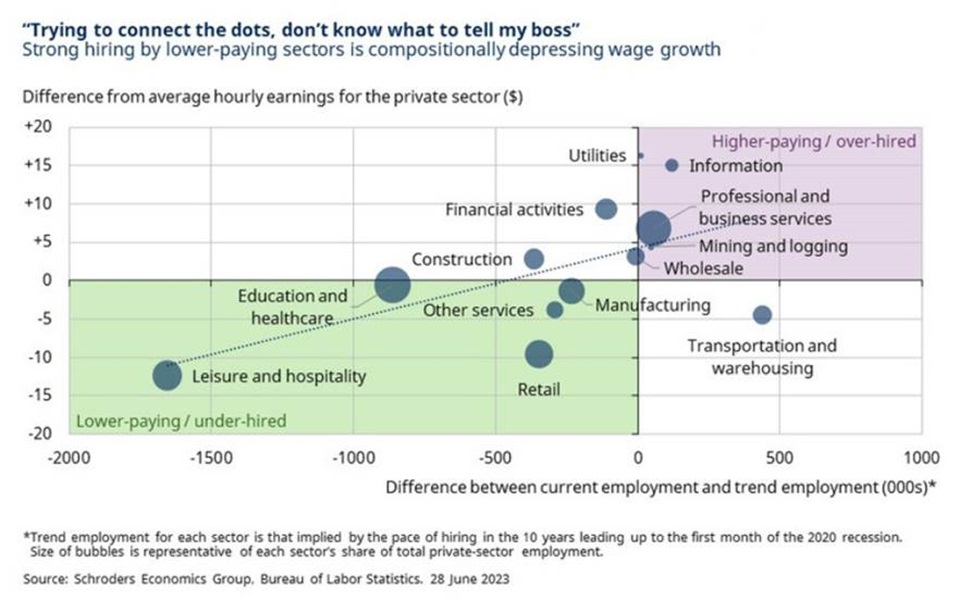

But it is worth bearing in mind that recent hiring has been concentrated among lower paid workers in the leisure and hospitality industries. Conversely, higher paying sectors have generally over-hired in previous years. And so weaker wage growth may be a symptom of these compositional effects, rather than necessarily a less competitive jobs market.

These effects can be looked through by using the Atlanta Fed measure. It tracks median wages for individuals over time, stripping out those at the extreme ends of the earnings spectrum. On this cleaner measure of pay growth, it has eased much more moderately, with its current rate of 6% well in excess of previous periods of labour market tightness.

As demonstrated, the conflicting data makes it difficult to reach a firm conclusion about the current state of the US labour market, much less its future direction. This is largely because pandemic effects continue to linger, which is one of the four reasons why the Fed has been struggling to tame inflation. And it is unclear to what extent these will fade or whether they will prove permanent.

But on the whole, our assessment is that we are seeing a softening from the very elevated levels we saw last year. And although this will provide some encouragement for the Fed, committee members are likely to remain concerned about the risk of a resurgence of inflationary pressures not unlike what the UK appears to be experiencing.

In Jerome Powell’s recent semi-annual testimony to Congress, he admitted to being a Deadhead: a fan of the Grateful Dead. It therefore seems doubtful that his musical taste would extend to Katy Perry. But if it did, perhaps the lyrics to Never Really Over would have been stuck in his head at this month’s policy meeting when officials indicated that they now plan to raise rates even further:

Two years and just like that

My head still takes me back

Thought it was done, but I

Guess it’s never really over

ENDS