Adriaan Pask, Chief Investment Officer at PSG Wealth

An early start is at the heart of achieving sufficient financial resources for the lifestyle you desire for yourself and your family. It gives your investments more time to compound and grow. Adriaan Pask, Chief Investment Officer, at PSG Wealth shares nine rules of thumb for younger investors who want to secure a strong financial future.

Rule 1: Plan to reach your 100th birthday

Many studies have found that advances in medicine, technology and overall quality of life have resulted in the average person’s lifespan increasing by about three years for every ten years that pass. By the time a person turns 85, they will therefore require additional savings to survive until the age of 105. However, the current pension system and retirement age in South Africa means that people tend to have less time to save enough for a longer retirement. The World Economic Forum expects a massive shortfall (US$80 trillion) in retirement funding among retirees globally by 2025 because many are underestimating how long they will live and how much money they will really need in retirement.

Table 1: Chance of living to 100

| Chance of survival | 65-year-old man | 65-year-old woman | 65-year-old couple* |

| 50% chance | 85 years | 89 years | 94 years |

| 30% chance | 91 years | 95 years | 99 years |

| 25% chance | 93 years | 97 years | 100 years |

| 20% chance | 95 years | 99 years | 102 years |

| 10 % chance | 100 years | 104 years | 106 years |

*At least one surviving spouse

Source: Sanlam

Rule 2: Consider inflation

Protecting your savings against inflation is crucial. Assuming South African long-term inflation averages about 6% per annum, you in essence start every year with minus 6% and need to ensure that you invest in such a way that you can recover that 6% and then grow the real value of your savings on top of that. For example, if a balanced portfolio offers a return of 11% per year, the real growth only equates to about 5% a year.

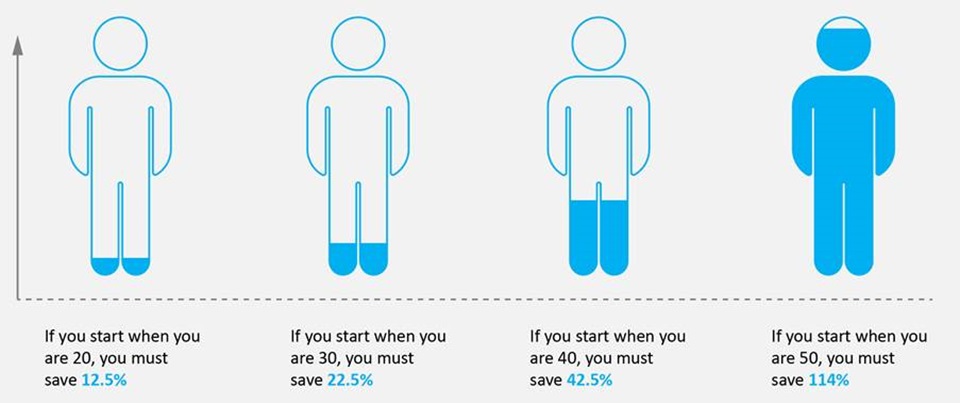

Rule 3: Start early

When you do not add to- or grow your savings, your required savings rate doubles every decade. A person who retires at age 60, has a life expectancy of 85 years, and has a required real return of 5% (as the previous point mentions) should save 12.50% from the age of 20, but that rate roughly doubles every ten years. The longer you delay, the steeper the climb. In the words of H. Jackson Brown Jr., “The best preparation for tomorrow is doing your best today”. Start early to lessen the load.

Graph 1: Your savings rate doubles every decade if you start later

Assumed retirement at 60, life expectancy of 85, ROE of 11%, inflation of 6%, 100% replacement income.

Source: PSG Wealth research team

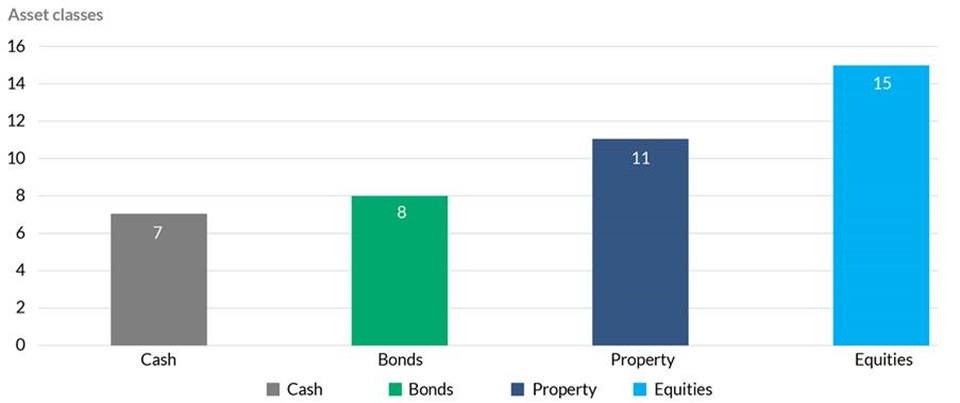

Rule 4: Know where to get ‘bang for your buck’

Investments need to have exposure to growth assets like equities to counter inflation. Equities have historically delivered better returns than other asset classes. This is because the impact of short-term market downturns weakens when staying invested for ten years or more. Data also shows that equities have offered the best real returns over longer periods.

Graph 2: Nominal returns (before inflation, fees and taxes)

Source: PSG Wealth research team

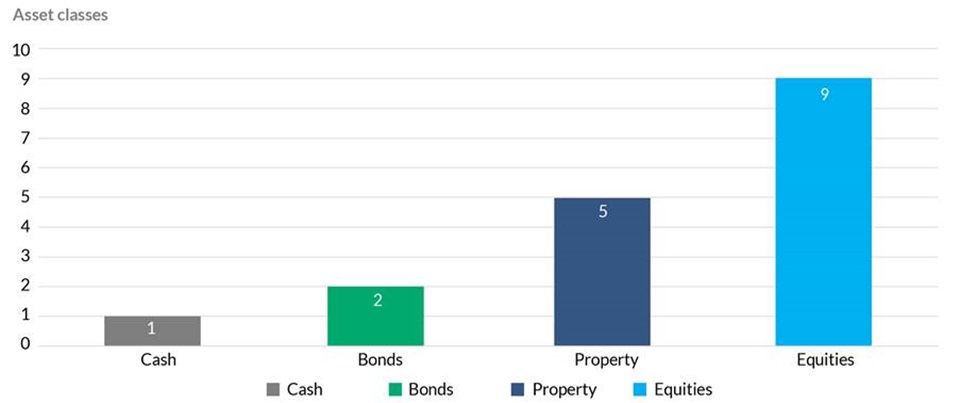

Rule 5: Being overly conservative can be a risky strategy

Not all asset classes are engineered to protect savings against inflation. For example, cash is a great way to cater for short-term income needs but is the weakest guard against inflation. A portfolio that consists solely of cash is all but guaranteed to underperform inflation after fees and taxes. As a stable asset class, it may provide short-term comfort; but over the long term, the opportunity cost is significant.

Graph 3: Real returns (after deducting 6% inflation, and before fees and taxes)

Source: PSG Wealth research team

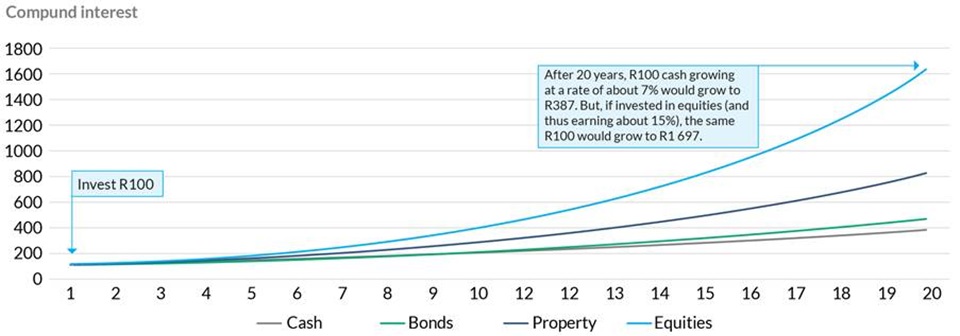

Rule 6: Compound interest is your greatest ally

Over the short term it may not seem like the difference between 7, 8, 11 or 15 percent is all that much, but these differences grow and compound over time. By way of example, a R100 cash investment that grows at 7% would grow to R387 over a 20-year period, whereas an equity investment growing at 15% would be worth R1 637.

Graph 4: How compounding works over time

Source: PSG Wealth research team

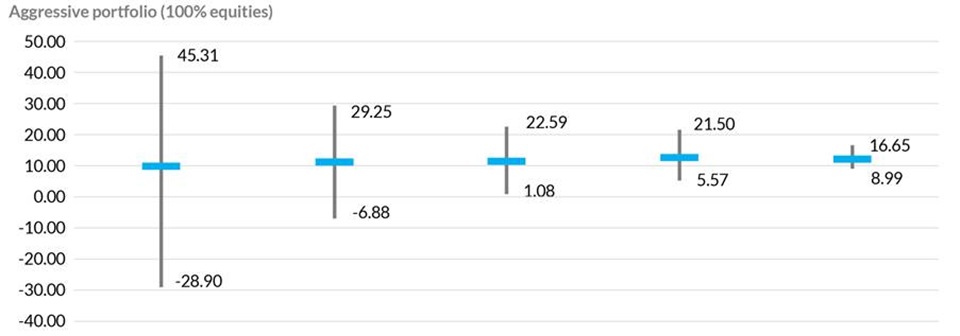

Rule 7: Risks reduce over time

Although equities can be volatile over the short term, they move closer and closer to their long-term returns as time passes. Thus, the returns can vary greatly over a short-term period, but the range of possible outcomes reduces as time passes. Use time as your protection against uncertain outcomes.

Graph 5: How risks reduce over time

Source: PSG Wealth research team

Rule 8: The plan is the map, and the map is sacred

Planning and preparation are integral parts of wealth creation. When markets turn volatile (as they often do), it’s important to recognise that these events have already been factored into the plans a financial advisor has prepared for you. We view these events as a natural part of the journey, a proverbial hump in the road. As long as you stick to the map, you won’t get lost. Have you ever tried to outsmart Google Maps? It rarely ends well!

Rule 9: Take advice

Investors who heed the advice of professional financial planners have a better chance of reaching their investment goals. Research from Morningstar, titled ‘Alpha, Beta and now Gamma’, argues that investors can generate better returns by having a sound investment plan and sticking to it. The research concludes that the retirement income for a hypothetical investor would be nearly 23% higher if they made use of a financial adviser.

ENDS