Sanlam Corporate and Simeka Consultants and Actuaries weigh in on the Budget Speech

Contributors:

Carien Veenstra – Senior Legal Advisor, Sanlam Corporate

PG Marais – Legal Advisor, Sanlam Corporate

Anita Roodman – Senior Manager: Legal and technical, Simeka Consultants and Actuaries

William Donachie – Legal and Technical Specialist

David Gluckman – Chairman, Sanlam Umbrella Fund

Danie van Zyl – Head of Smoothed Bonus Centre of Excellence, Sanlam Corporate: Investments

Dirk Oosthuizen – Head: Research and Development, Simeka Consultants and Actuaries

1. Introduction

Tax revenue collections for 2022/23 are expected to total R1.69 trillion. This exceeds the 2022 Budget estimate by R93.7 billion, and the 2022 Medium-term Budget Policy Statement (‘MTBPS’) estimate by R10.3 billion. Over the medium-term, revenue projections are R6 billion higher than the estimates of the 2022 MTBPS. As a result, there are no major tax proposals in this budget.

The 2023 Budget provides tax relief totalling R13 billion to support the clean energy transition, increase electricity supply and limit the impact of consistently high fuel prices. In addition, the budget provides inflation-related adjustments to the personal income tax tables, the retirement tax tables, transfer duties and excise duties for alcohol and tobacco. R4 billion in relief is provided for households that install solar panels, R5 billion is provided to companies through an expansion of the renewable energy incentive and there is no increase in the fuel levies, resulting in R4 billion in tax foregone.

2. Proposals affecting the retirement fund industry

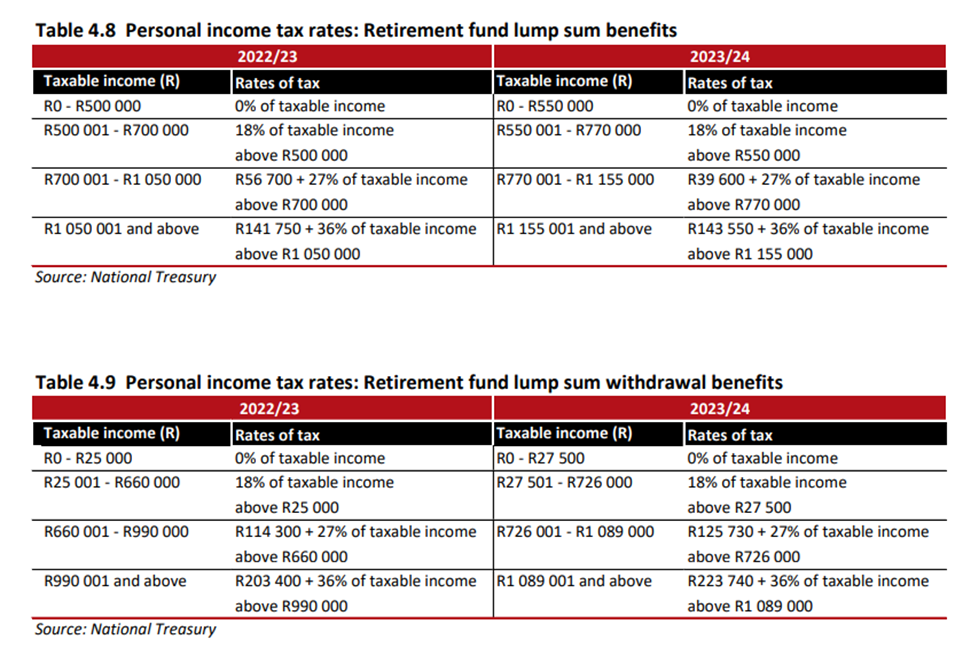

2.1. Adjustment of retirement tax tables

As part of the periodic reviews of monetary values in tax tables, the brackets for retirement fund lump sum benefits and retirement fund lump sum withdrawal benefits will be adjusted upwards by 10% to compensate for inflation. This means that the tax-free amount that can be withdrawn at retirement increases from R500 000 to R550 000.

The rates shown in tables 4.8 and 4.9 below are effective from 1 March 2023:

3. Other matters of interest

3.1. Conduct of Financial Institutions Bill

National Treasury has revised the Conduct of Financial Institutions Bill based on feedback from stakeholders. The Bill is expected to be tabled in Parliament in early 2023. It will introduce a new legal framework for the regulation and supervision of the conduct of financial institutions, which will shift away from the institutional form to an activity-based licensing approach.

Comment: The Conduct of Financial Institutions Bill will introduce several amendments to the Pension Funds Act and will have far-reaching implications for retirement funds and retirement fund administrators.

3.2. Transformation and financial inclusion

The FSCA published its draft transformation strategy for the financial sector in 2022. In the first phase of implementation, the FSCA will engage with industry and other stakeholders on the current legal landscape governing transformation. In the second phase, it will set and supervise specific licensing and regulatory requirements for financial institutions in line with the relevant legislation. The FSCA has committed to

following a proportionate approach that will not unduly burden small businesses. The final strategy will be published by March 2023.

3.3. Financial education policy

In 2023, National Treasury will publish a consumer financial education policy document for public comment. This policy document addresses consumer protection in the financial sector in the context of financial inclusion and transformation.

3.4. Tax administration

Aligning tax registration requirements for non-resident employers

It has been noted that non-resident employers may not have representative employers in South Africa for purposes of employees’ tax. They are, as a result, not liable to deduct or withhold tax from the remuneration that is paid to their employees who render services in South Africa. Nevertheless, given that they pay remuneration, they are required to register with SARS as employers. They are liable for skills development levies and unemployment insurance contributions, which many pay. It is proposed that the various provisions be aligned to ensure consistency.

3.5. Combating financial crimes and illicit activities

Since 2003 South Africa has been a member of the Financial Action Task Force (FATF), which sets global standards to combat money laundering and the financing of terrorism across national borders.

The FATF’s most recent mutual evaluation of South Africa identified a number of deficiencies in its legislative framework and implementation. Government is working to rectify these shortcomings. At its February 2023 plenary, the FATF will pronounce on South Africa’s progress and the extent to which it will face enhanced monitoring, including possible grey listing.

Comment: The efforts to prevent grey listing are bound to lead to a considerable additional administrative and compliance burden being placed on the financial services industry and payroll administrators.

4. Personal income tax

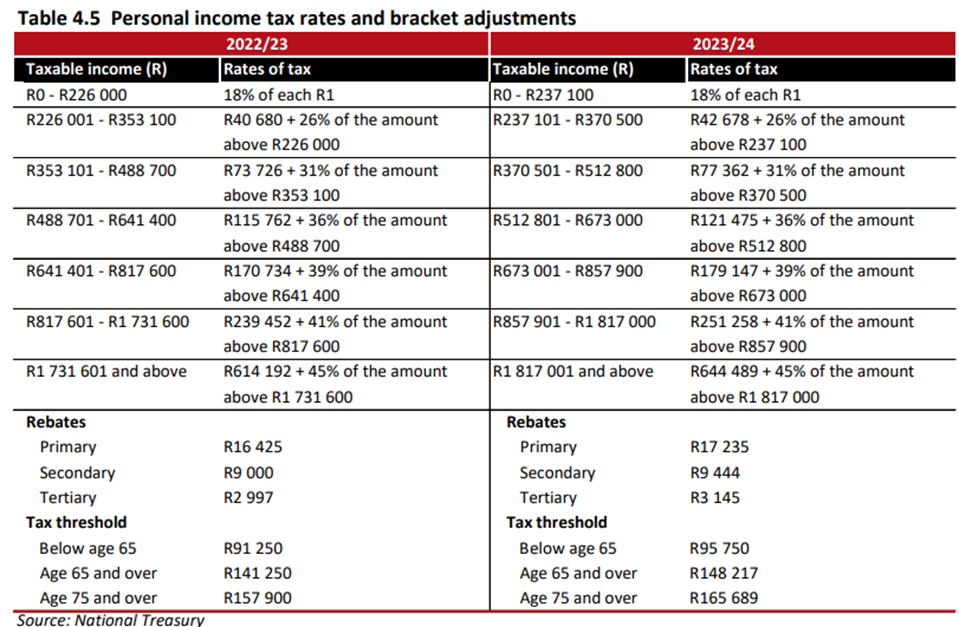

4.1. Income tax brackets

The personal income tax tables are reviewed annually to ensure that inflation does not automatically push personal income taxpayers into higher tax brackets. The 2023/24 tax brackets will be adjusted in line with the expected inflation rate of 4.9%.

As a result, the annual tax-free threshold for a person under the age of 65 will increase from R91 250 to R95 750. Relief mainly benefits middle-income households.

The brackets have been adjusted as follows:

4.2. Medical tax credits

Medical tax credits will increase from R347 to R364 per month for the first two members, and from R234 to R246 per month for additional members.

4.3. Social grants

The old age and disability grants increase by R90 on 1 April 2023 and a further R10 on 1 October 2023. The result is a total increase to R2090.

The COVID-19 social relief of distress grant of R350 per month will be extended for a year until 31 March 2024. Government is still considering alternative options to provide appropriate social protection for the working-age population that can replace or complement the current grant.

Social grants will increase in line with inflation, as per the table below:

ENDS