Izak Odendaal – Old Mutual Wealth Investment Strategist

Amid the hustle and bustle of daily life, it is easy to forget how small we are. It would take 1.3 million Earths to fill up the sun. The past week saw massive solar storms, explosions on the surface of the sun that emit electromagnetic radiation. When these electrically charged solar particles hit the Earth’s magnetic field, they are funnelled north and south towards the poles. In the upper atmosphere, they crash into oxygen and nitrogen atoms, resulting in the spectacular aurora light phenomenon. This is usually more visible in the Northern Hemisphere, but last ‘s week solar storm was so big even South Africans could catch a glimpse in places. There is potential peril amid the beauty. These geomagnetic storms can also knock out communication equipment, but fortunately not this time.

Solar activity varies over an 11-year cycle, and the last few days saw the peak of this round. The sun’s magnetic poles also flip at the end of every cycle, unlike on Earth where it happens rarely. Yes, even the mighty sun is subject to cycles.

For investors, understanding the difference between cycles and structural trends is vital. So much of what we deal with in markets has mean-reverting tendencies. What goes up, eventually comes down. However, there are also structural trends that persist for long periods. Demographics is one. A low birth rate one year does not give way to a high birth rate the next year. Instead, a low birth rate compounds over time as there are fewer girls who can grow up to be mothers.

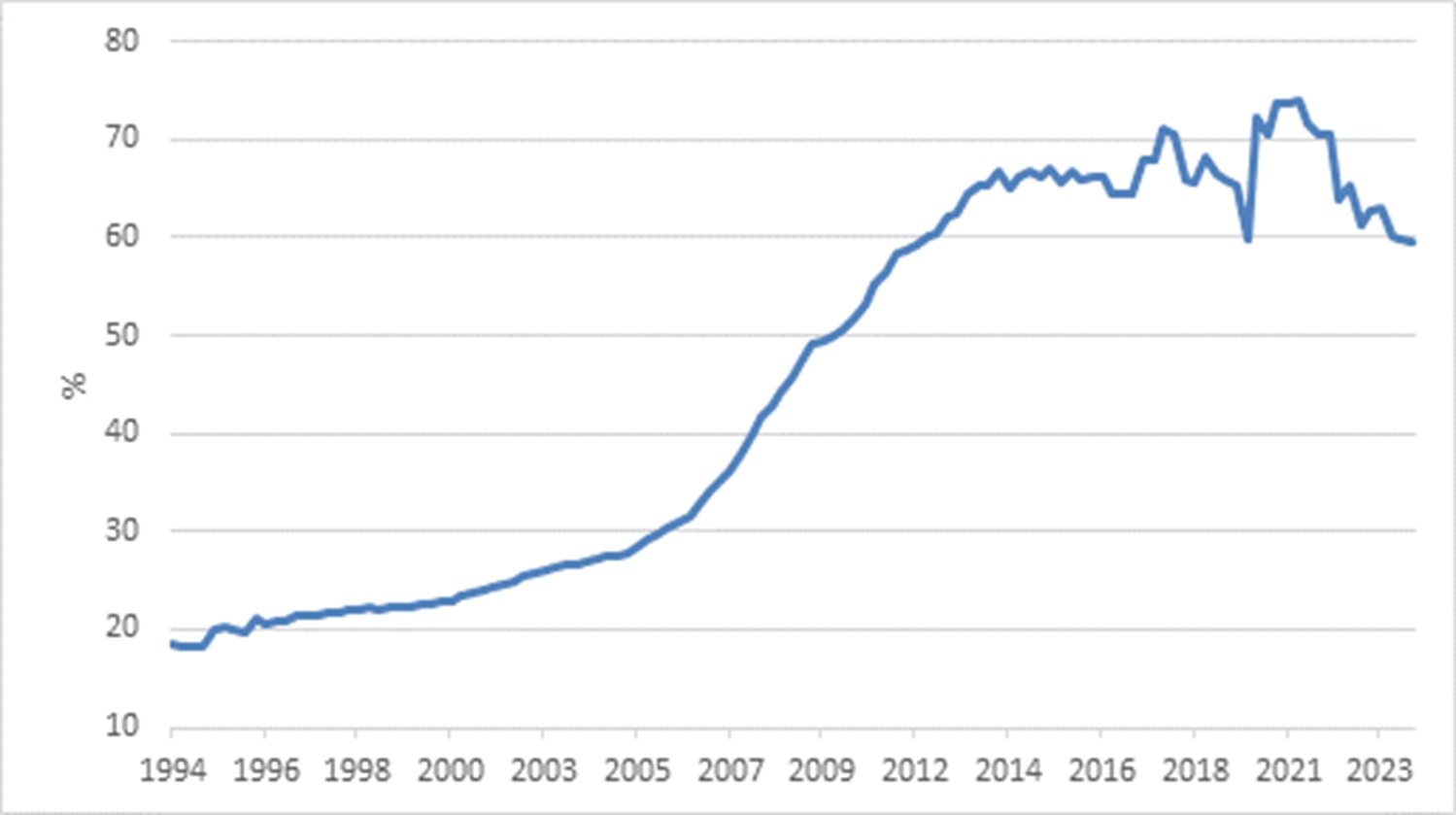

There was a time when the US economy was so dominant, it was effectively like the sun in our solar system. In 1960, with only 6% of the global population, the US share of annual global economic output (GDP) was 40%. Today its share has declined 25%, and China has emerged as a real competitor in the economic sphere. Adjusting for the different cost of living in the two countries which is much lower in China – on purchasing power parity basis, in other words – the Chinese economy has overtaken the US. However, it remains at number two when measured at market exchange rates. More importantly, its rapid catch-up with the US since the 1990s has stalled.

Chart 1: China GDP as a share of US GDP at market exchange rates

Source: LSEG

The two countries have very different economic models, and not just because one is notionally communist, while the other is the red-blooded home of free markets. More than two-thirds of US national income goes to households who spend most of it. Therefore, analysing US economic trends always starts with the shape of the consumer (more on this below). In China, household income is 60% of GDP but household consumption is less than 40% of GDP. The difference is saved. Chinese households save much more than almost anywhere else in the world, now or in the past.

As many commentators and Western policy advisers have pointed out, a more balanced Chinese economy, and one that could enjoy ongoing sustained growth, would be one where households spend more and save less. Getting there is not easy, however.

Chinese households save a lot due to big gaps in the social safety net and the low returns earned on these savings. The state-owned banking system offers depressed deposit rates, so that cheap credit can be extended to favoured businesses. Equities have been flat for more than a decade, and the option of earning a decent return in the property market has now evaporated. Demographics are also often mentioned as a driving factor, since the one child policy means that each person theoretically might one day support four grandparents.

This abundance of savings leads to domestic over-investment. No country invests such a high share of GDP (around 40%). This has given China amazing infrastructure, such as the most impressive high-speed rail network in the world, but most of it operates at a loss.

The amount of economic growth that each yuan of investment creates has therefore been falling over time, meaning that growth has been propped up over the past decade or so by a massive debt binge, much of it related to the property bubble. It is somewhat paradoxical that an economy with too much savings would also have too much debt, but that is what we’re dealing with.

Cyclical uptick

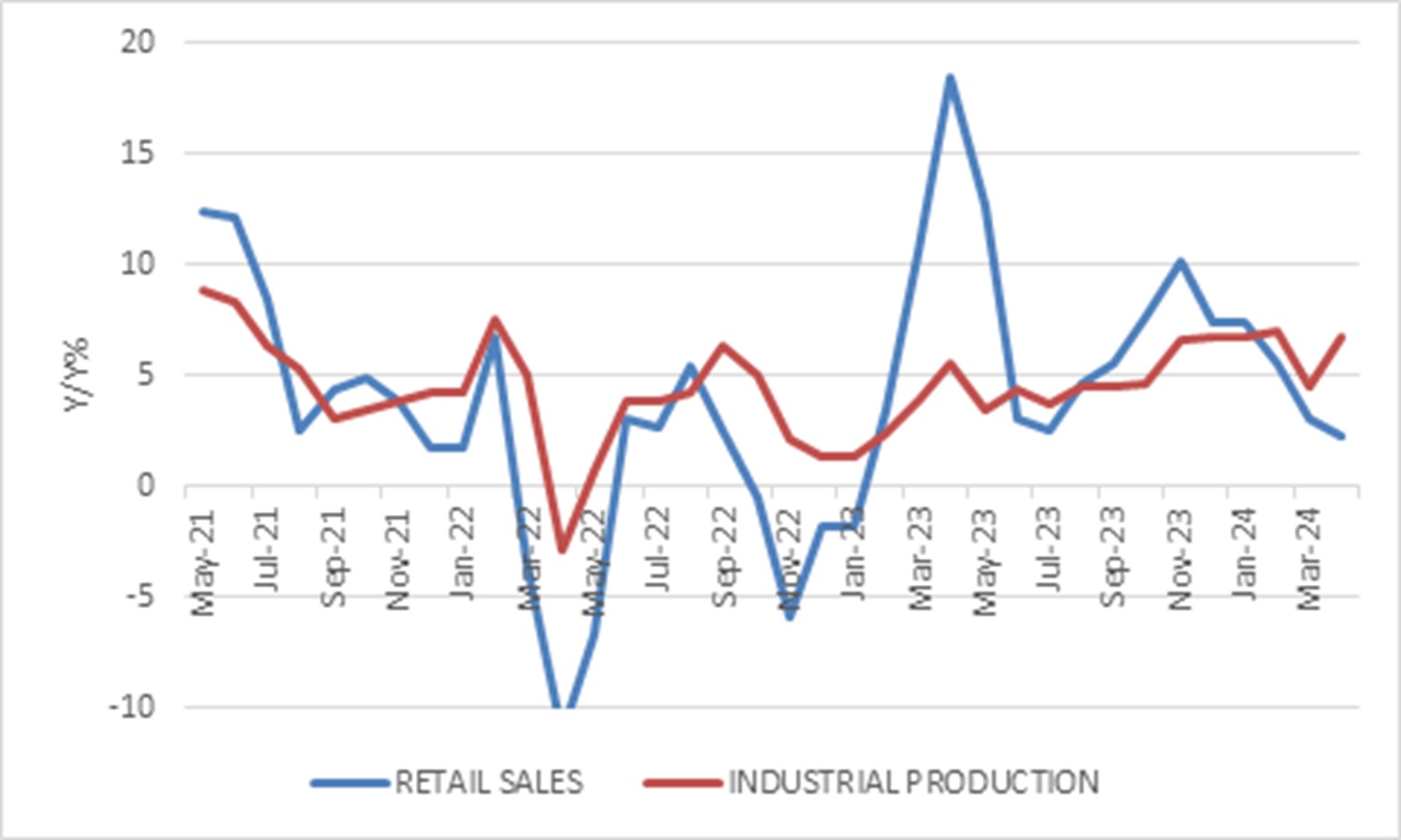

These are the structural challenges. The cyclical picture is an economy that came out of Covid lockdowns in weak shape. This is confirmed by persistently low inflation, a sign of weak overall demand. Rather than supporting households, as in the US, the government largely supported businesses. In particular, electric vehicles (EVs), batteries, solar panels and computer chips have emerged as favoured sectors. But since production exceeds what can be consumed locally, much of this must be exported. Last year, China became the world’s biggest vehicle exporter, having long been a net importer of cars.

Chart 2: China retail sales and industrial production

Source: LSEG Datastream

A raft of other policy support measures, including interest rate cuts introduced in recent months, seems to be gaining some traction. While the structural headwinds remain, the Chinese economy seems to be enjoying a cyclical bounce, led by its factory sector. This is good news for the global economy, but only up to a point.

The rest of the world is now reaching a limit in terms of the Chinese exports it is prepared to absorb. This is particularly true in the US where there is increasing talk of a “second China shock”. The first was the massive loss of manufacturing jobs in the early 2000s, often concentrated in specific regional manufacturing hubs. The fear goes beyond job losses. There is also a growing recognition that a decimated manufacturing sector leaves the US vulnerable in cases of emergency, as it discovered during the Covid pandemic when most medical supplies had to be sourced from China. Worse, in a case of war, manufacturing capacity is necessary. While the US can still outspend China in military matters, China can outproduce it.

This culminated in President Joe Biden last week announcing steep tariffs on Chinese electric vehicle imports amounting to 100% of the value of each car. Other items also saw big tariff increases. There are currently very few Chinese EVs in America, so this is very much a proactive step to prevent a flood of cheaper imports. It is also a political move ahead of the election. Donald Trump said he would raise tariffs to 200% if he gets into office, meaning that the presidential candidates of both large parties are competing on who is tougher on China. Such consensus is rare in US politics these days.

China’s excess productive capacity will have to go somewhere, so don’t be surprised to see even more Chinese cars on South African roads, including electric vehicles. Unlike the Americans, we don’t mind cheap solar panels and now have a 50-day streak of no loadshedding thanks in large part to them. This implies some downward pressure on global goods prices, but potentially also tariff increases from other countries to protect domestic production.

This is a messy moment in global economic history. The US and Chinese economies are deeply intertwined, with $750 billion in goods and services flowing between the two countries last year, with much more going from China to the US than the other way round. US companies also make around $400 billion in revenue from sales in China each year. Disentangling these relationships poses risks to the global economy, but also opportunities for others to step in.

At the centre

In financial markets, as opposed to ground level economic activity on the ground, the US very much remains at the centre of the galaxy. The US dollar maintains its central role in global finance, with more than half of all bonds and equities priced in dollars, as are more than 80% of commodities. Dollar assets bake up 60% of central bank foreign exchange reserves. Indeed, China’s own substantial reserves, the cumulative result of years of trade surpluses, are heavily invested in in US assets, about $2 trillion in total. There is just no other market large and liquid enough to absorb so much capital.

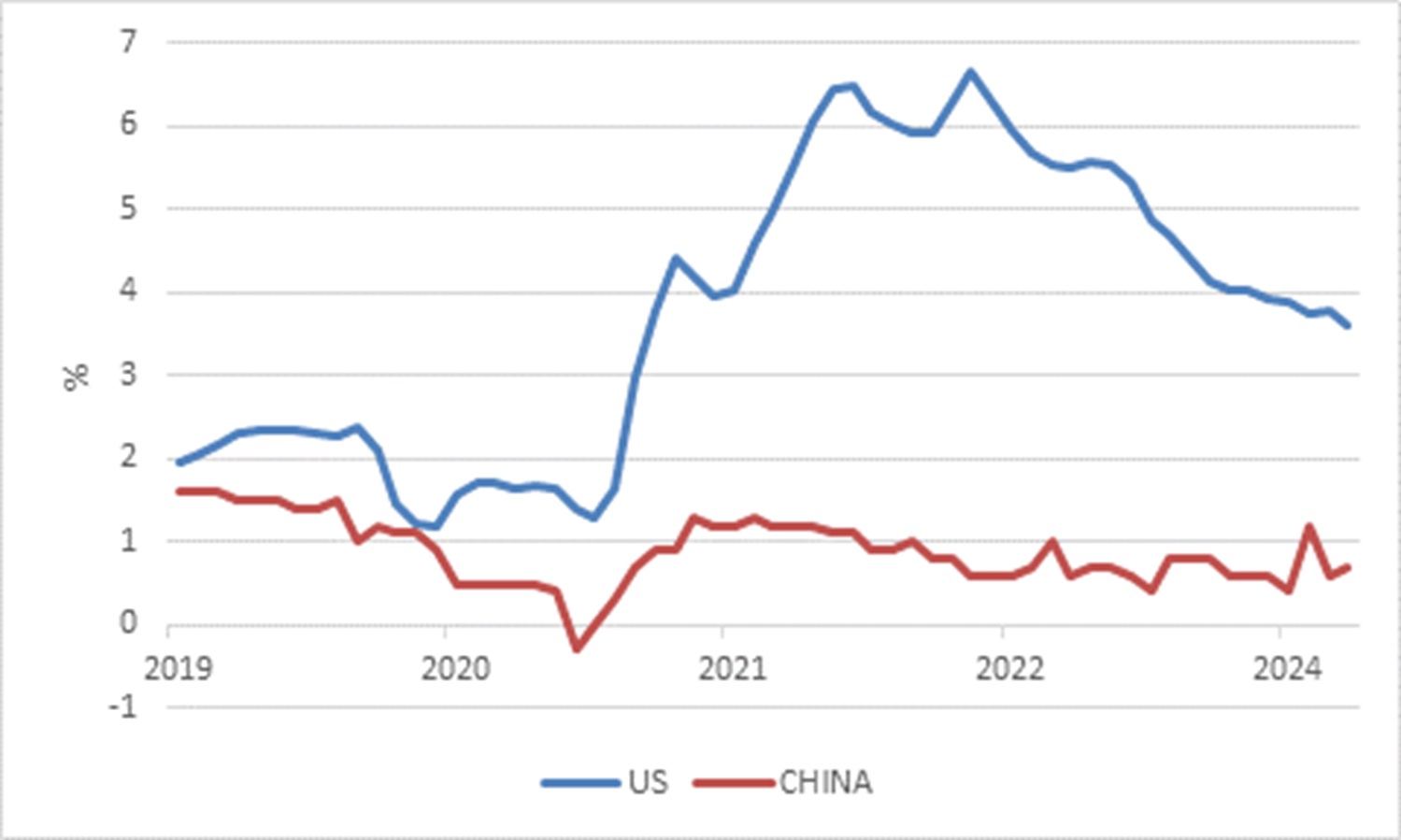

So, the world continues to watch anxiously what the US Federal Reserve will do. Inflation declined rapidly last year, but the first three months of 2024 have seen inflation surprising to the upside, resulting in a complete rethink of interest rate expectations on the part of market participants and policymakers. There was even talk of further rate increases.

Fortunately, April US consumer inflation declined to 3.4% year-on-year, in line with expectations. Core inflation, excluding volatile food and fuel prices, was also lower at 3.6%.

Chart 3: US and China core consumer inflation

Source: LSEG Datastream

This is still too high from the Fed’s point of view, and service inflation remains particularly elevated. But the fact that overall inflation is drifting lower and not accelerating rules out rate hikes and keeps the door open for the Federal Reserve to cut rates a few times in the second half of the year. Growth is still too strong for the Fed to cut soon and deep, but this might not be the case later this year.

Weak links

While there is overall strength in the US economy, beneath the surface there are weak links. Notably, there is a stark divide between those firms and households with fixed interest rate exposure and those without.

Large companies that borrow in the bond market could fix the cost of most of their debt at lower rates. Many also have healthy cash balances now earning a good yield. In contrast, smaller businesses that borrow from banks are exposed to higher rates.

Similarly, households who bought their homes before 2021 could lock in low mortgage rates below 3%. New buyers must pay more than 7%. Since house prices remain elevated, housing affordability is near an all-time low. For those unable or unwilling to buy, rents have gone up significantly. In other words, times are tough for many people.

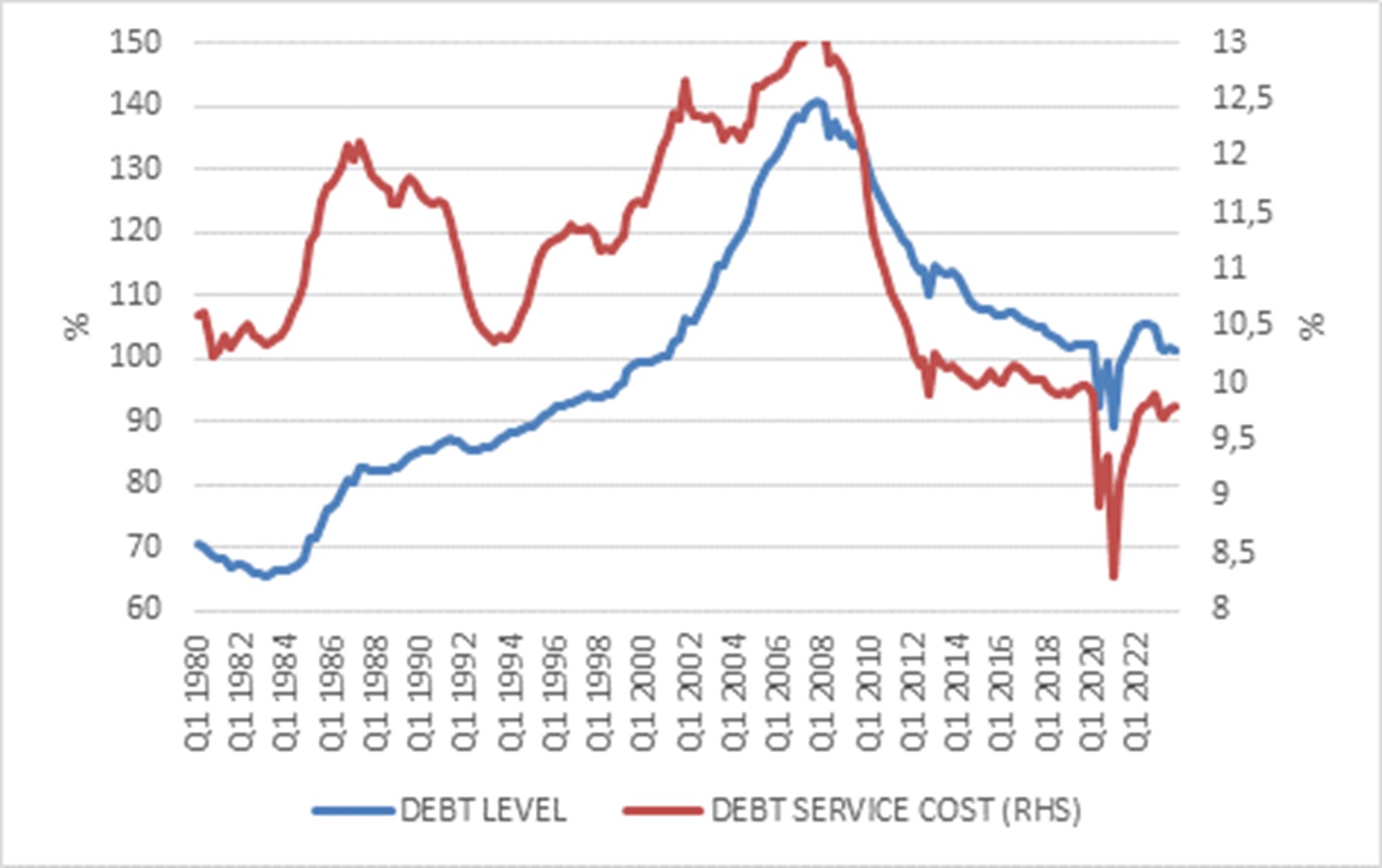

While aggregate household debt levels are at record levels, income has grown faster than debt, as has wealth, mainly equities and housing. Debt service costs (interest payments) as a share of income also remains historically low. In other words, overall household balance sheets are strong, but this masks a discrepancy between haves and have-nots.

Chart 4: US Household debt and interest payments as % of disposable income

Source: LSEG Datastream

For the latter, delinquencies are on the rise, with the 11% of people who are more than 90 days late on their credit card payments being the highest percentage since 2011.

Mortgages make up 70% of total household debt, and credit cards only 6%, so we’re not in alarming territory, but at the margin, high interest rates are squeezing people. This suggests spending will cool from current levels, but not crash.

Supportive

Of course, we can’t discuss the trade tensions between the US and China, rapidly turning into a second Cold War, without mentioning the risk of an all-out war over Taiwan, which China considers as part of its sovereign territory, but which the US has promised to protect. One can only hope that the financial and economic chaos that would result is enough of a deterrent for this not to happen. After all, as noted, these two giant economies remain deeply intertwined.

That remains a big risk for one day, but for the meantime, the cyclical story seems to be evolving in a desirable direction. The US is not overheating, which would cause the Fed to raise interest rates further, nor is a recession likely in the near term. On the other side of the world, Chinese activity is picking up. If we look through the political noise, this is a supportive backdrop for markets, explaining the recent rally in equities and the rand. But just as the Earth’s magnetosphere protects us from solar radiation – without it, the planet would be fried – sensible diversification is the investor’s best defence.

ENDS