Izak Odendaal, Investment Strategist, Old Mutual Wealth

South Africa has always been a country with high levels of political uncertainty, but not political instability. For the last three decades, it has been governed by a single party with a comfortable majority. No more. We are now in unchartered political territory, and things can go in very different directions from this point forward.

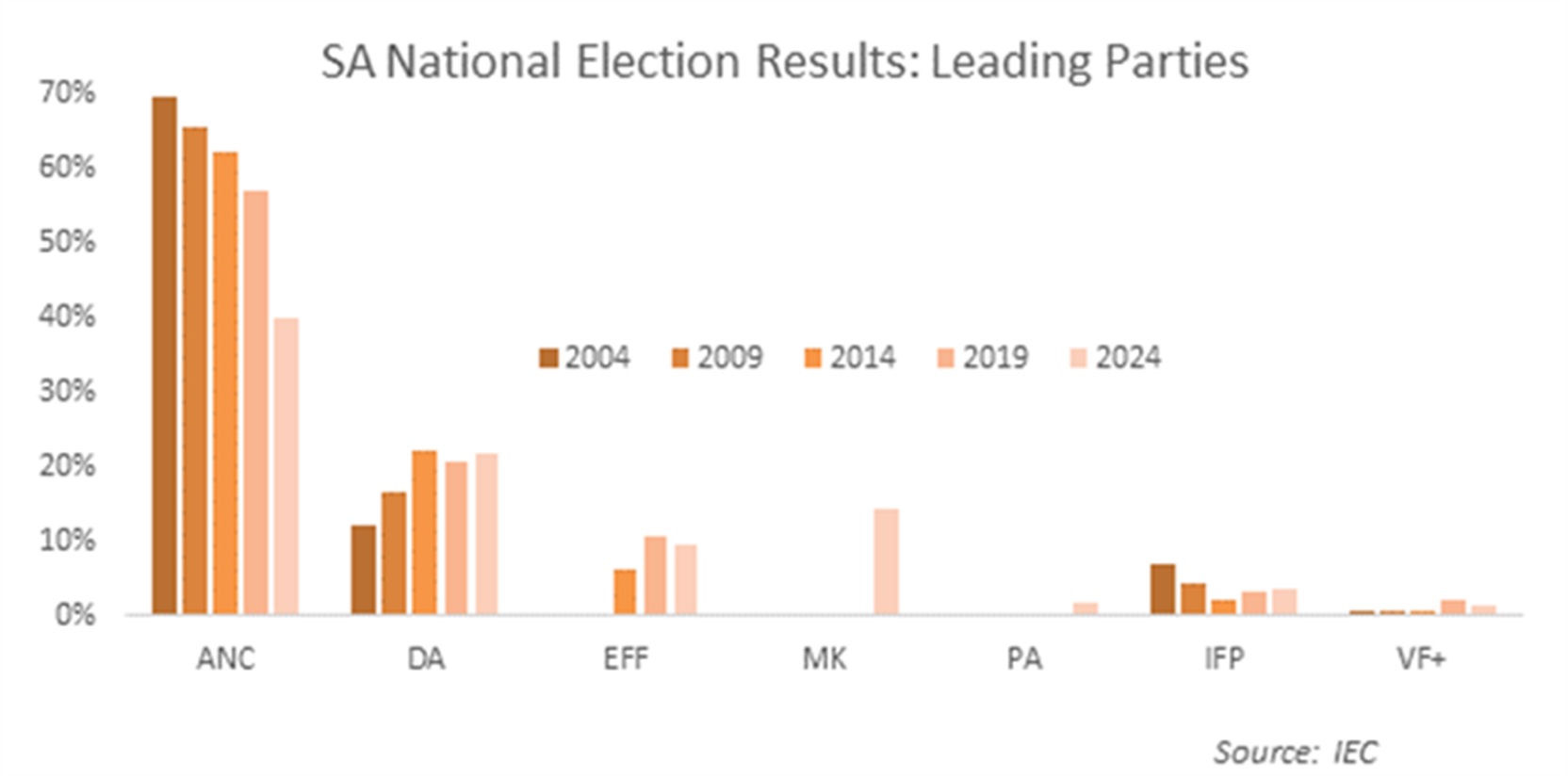

While the ANC’s share of the national vote was expected to drop below 50%, the end result was even more startling as it only secured 40%. It is a massive drop from the 57% share it won in 2019. It also lost its majority in KwaZulu-Natal, Gauteng and the Northern Cape. The big winner, of course, was the MKP, securing 14.6% in its first election and ending second behind the DA, which grew its support slightly to 21.7%.

In the weeks running up to the election, the broad consensus among local and international investors was that the ANC would get between 45% and 50%, allowing it to remain in power with the help of one or two smaller parties. However, its losses were too big and it will need to partner with one of the large parties – the MKP, EFF or DA – in a formal or informal coalition arrangement.

Chart 1: National election results (biggest parties)

Source: IEC

The immediate market reaction was negative, since markets are always moved by surprises. But this doesn’t mean that the outcome was negative. Democracy is alive and well in South Africa. Voters are still engaged and turned out in numbers to express their hopes and frustrations. Despite being an extraordinarily violent country, we’ve managed yet again to host a free and fair election, without major disruptions. The ANC accepted the outcome, unlike in many other countries where losers instinctively cry foul or where the military gets involved to influence political outcomes. While our democracy isn’t perfect, South Africa is not experiencing a disastrous slide to authoritarianism.

But where are we headed? Coalition talks are tentatively getting underway, but given the scale of the election surprise, the biggest discussions are probably happening inside each of the major parties. They need to agree on what they want internally before negotiating externally. It could take weeks for talks to be finalised, so we will have to wait. The most pressing step is that the National Assembly must elect a president within 14 days, otherwise fresh elections must be held. This can take place without formal coalition agreements in place, but a majority of MPs must support the candidate, who at this stage is still likely to be Cyril Ramaphosa.

A number of different things could still happen, but the market will treat the outcomes as binary: either a ‘Grand Coalition’ between the ANC and the DA and others emerges, which would be seen as positive; or there will be a leftist/populist coalition of the ANC and either the EFF or MKP, or both.

In the case of the former, South African assets and the rand would rally, while they would sell off in the case of the latter.

However, beyond the knee-jerk market reaction, there is still complexity and nuance. For instance, while there is much common ground between the ANC and DA in terms of the substance of their policies, there remains a wide gap in terms of the style of politics which could make it a volatile relationship. On the other hand, if the ANC partners with the EFF, the latter’s relatively weak showing in the election means it will not have the upper hand in setting coalition priorities.

It is also not the case that there has been a decisive shift to the left on the part of South African voters. The old joke has it that the problem with socialism is running out of other people’s money. The parlous state of government finances means there is no room to embark on fantasies like widespread nationalisation. The EFF’s growth has topped out, while the MK’s success is probably more due to ethnic mobilisation and a protest vote by disgruntled ANC voters than a leftist policy platform.”

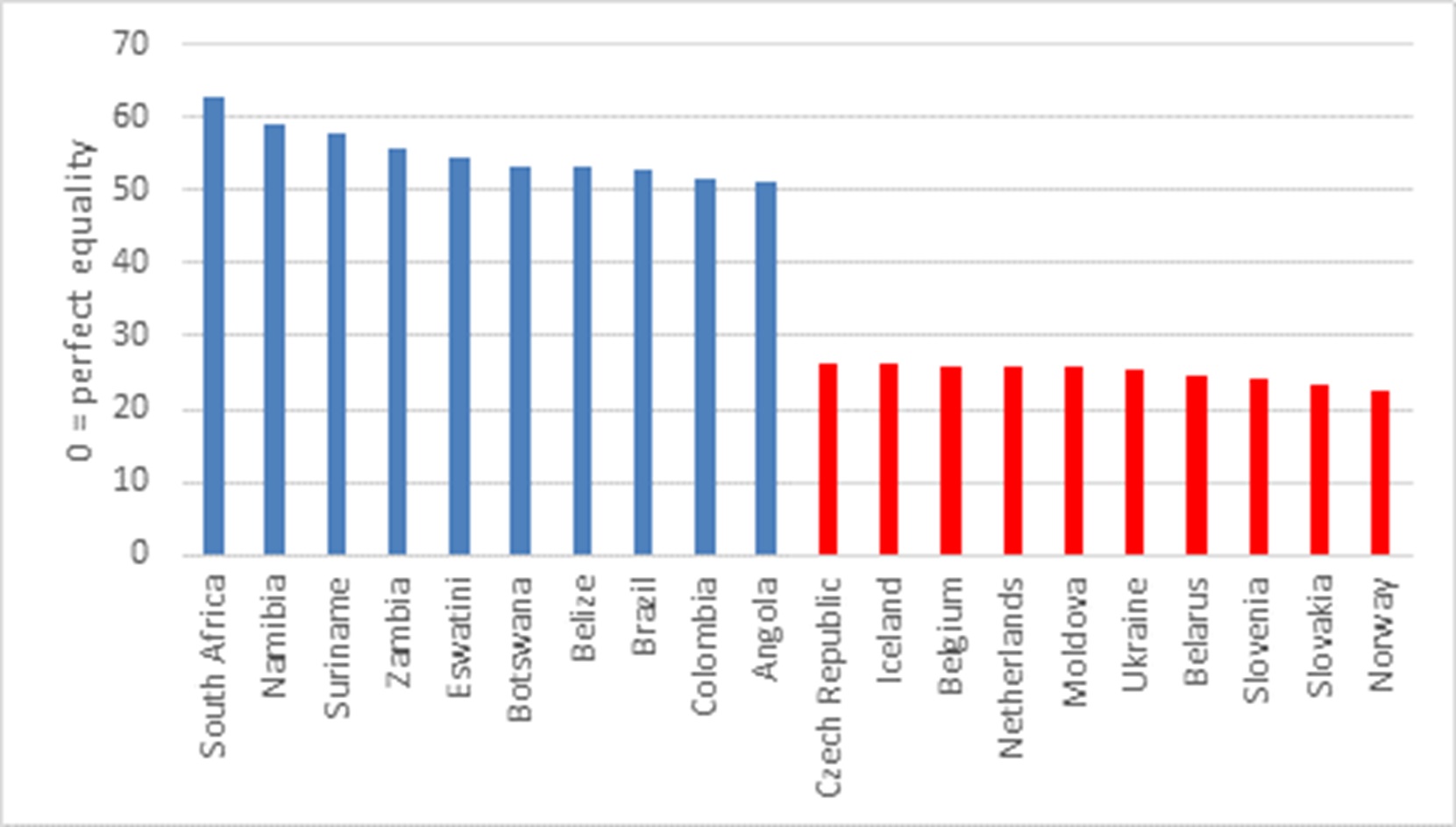

Given that South Africa is the most unequal society in the world, at least as measured by the Gini coefficient, one would expect a large and natural constituency for leftist policies. But South African voters, for whatever reason, continue to favour centrist and centre-left parties.

Chart 2: Top 10 and bottom 10 countries by the Gini coefficient

Source: World Bank

However, this extreme inequality means that the risk of a leftist/populist lurch will probably always be at the back of investors’ minds. For this reason, South African assets carry a long-term risk premium.

Cyclical and structural

Ultimately, the big question for investors is what economic policies the next government will implement.

In mature economies, investment analysts obsess over the trajectory of the business cycle and politics is usually an afterthought. The UK will go to the polls in July, for instance, but it’s hard to argue that a given election outcome there will impact the UK economy much or alter its attractiveness as an investment destination.

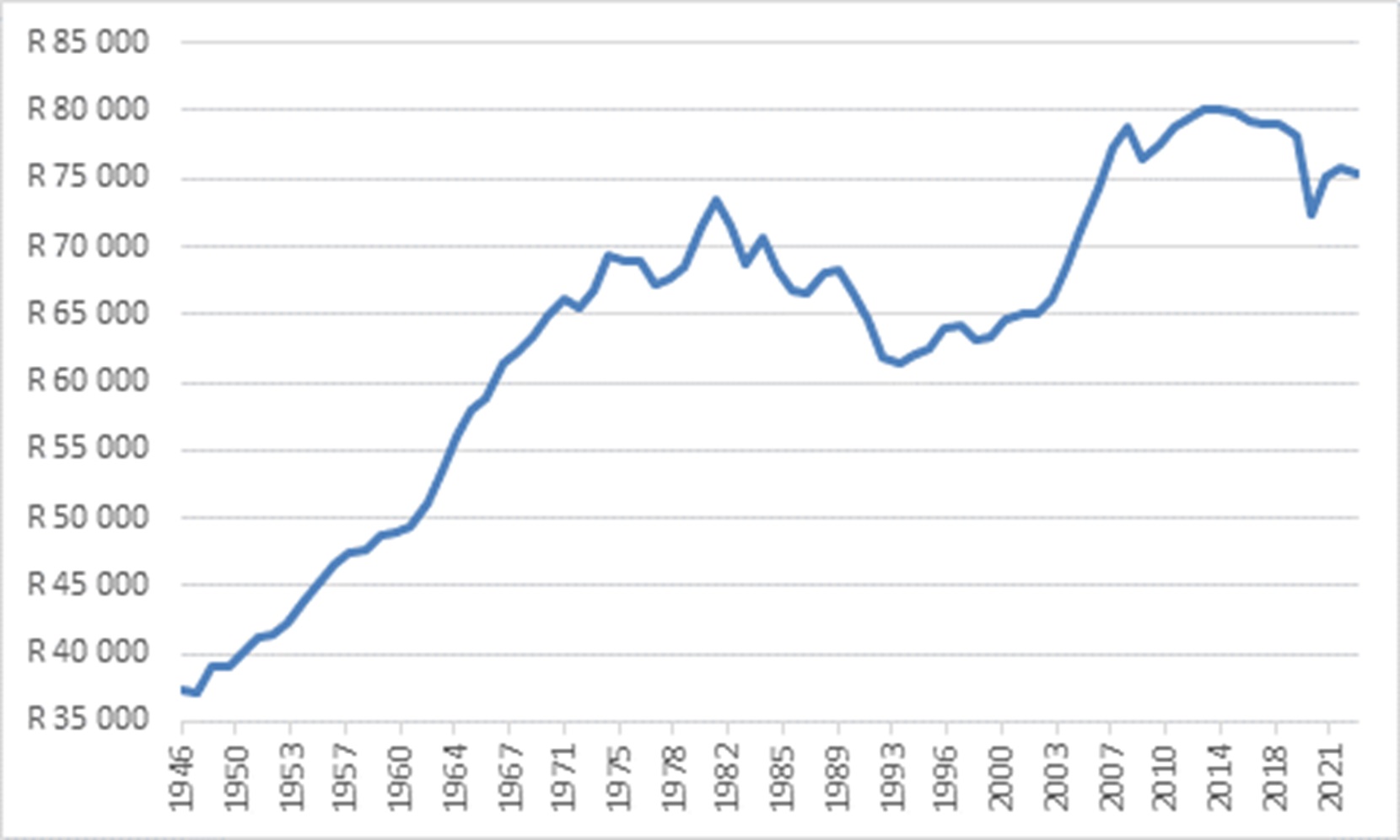

South Africa is different. It has been stuck in a low growth trap for the past decade. In real terms, growth averaged less than 1% per year in real terms. This is not an economic collapse by any means, but it has failed to keep up with annual population growth. The traditional analysis of business cycle indicators is therefore of less relevance in South Africa today, and the emphasis is instead on structural reforms to raise the economy’s growth potential.

Chart 3: South Africa real income per capita

Source: LSEG Datastream

Think of a car. Business cycle analysis asks how fast it is going. What are the brakes and what are the accelerators? Is it overheating or is it underperforming its potential? In contrast, the structural analysis asks: can we take out the engine and put in a new, larger and powerful one? Or has something happened that means the engine is now permanently smaller and weaker?

In the case of South Africa, some progress has been made in rebuilding the engine, with far-reaching reforms made to the electricity sector. Reforms in the logistics arena (ports and rail) are less far down the track, excuse the pun, but underway. Ditto for bulk water provision and other forms of infrastructure provision, and the fight against organised crime. The big success to date and reason for continued optimism has been increased room for the private sector to get involved on these fronts. There is no reason to believe that this will change dramatically. Also important is ongoing fiscal discipline, which might be harder to maintain in a coalition set-up. But again, there is likely to be a great degree of policy continuity. The ANC will not give up the Finance Minister position, and the leadership team at Treasury should remain in place.

As for monetary policy, it remains shielded from political interference, and continues to set policy in the long-term best interests of the country.

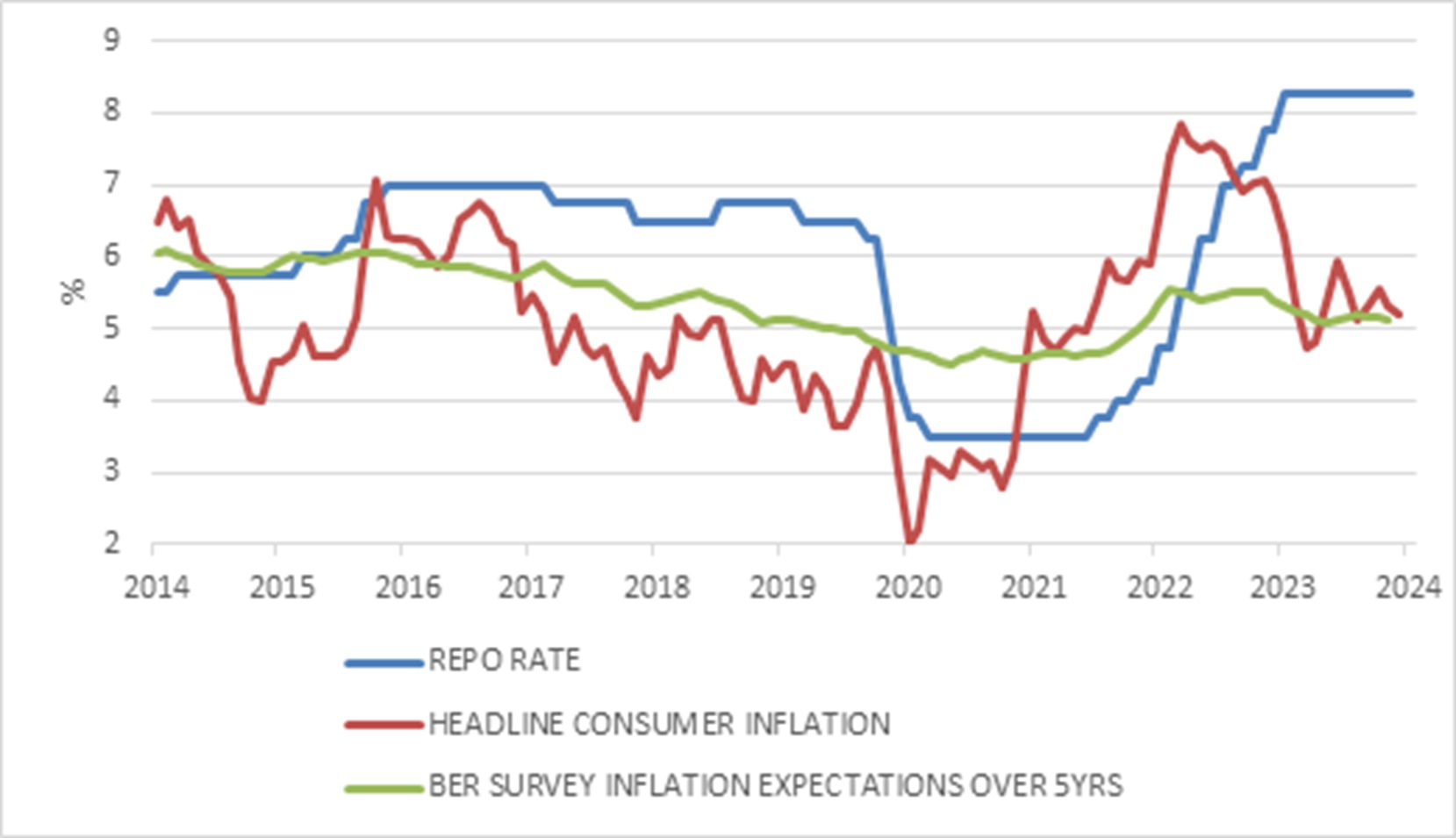

Amidst all the election drama, few people paid attention to the Monetary Policy Committee meeting. As expected, the outcome was a unanimous decision to leave the repo rate unchanged. However, the tone of the meeting statement was more upbeat. Oil price and exchange rate risks have abated somewhat, and the Reserve Bank now forecasts that inflation will reach its 4.5% objective in the second quarter of next year, earlier than previously thought.

Chart 4: South African interest rates and inflation

Source: LSEG Datastream

The Bank remains concerned about elevated surveyed inflation expectations, but these tend to lag actual inflation. In other words, as inflation falls, it will probably pull expectations lower. Inflation risks are now viewed as being “balanced” rather than “biased upwards”.

Despite a weaker-than-expected first quarter, the Bank still expects 1.2% growth this year, rising to 1.4% next year and 1.6% in 2026. This forecast still assumes a fairly high level of loadshedding over the next year. If the improvement of the past two months persists, there is room for an upward surprise (as an aside: the power didn’t go off immediately after the election, as many memes suggested it would).

Barring a serious market dislocation, the MPC is likely to start a modest cutting cycle in the coming months, perhaps as early as the next meeting in July. As always, it will keep a close eye on international interest rate developments. It helps that Friday’s US inflation reading was a touch softer than expected.

A lower repo rate will lift the cyclical performance of the economy, but not its structural growth trend. Over the last few years, every MPC statement has urged the government to implement structural reforms that will improve growth and lower inflation. The closing paragraph of the May MPC statement reiterates this call for “a prudent public debt level, improving the functioning of network industries, lowering administered price inflation, and keeping real wage growth in line with productivity gains.” Again, this is where the new governing coalition will have to stay the course.

In the post-meeting press conference, Governor Kganyago noted that the Reserve Bank remained committed to achieving macroeconomic stability, and that if fiscal policy changed in an unwelcome direction, monetary policy would do “the heavy lifting to deal with inflation, because that is the mandate of the central bank.” This was the case during the Zuma years, when monetary policy had to overcompensate for the lack of policy credibility elsewhere in government. The independent central bank, together with the independent judiciary, a free and vocal media, and other institutions, will continue to keep disaster at bay in South Africa.

Finally, as much as our attention is going to be glued to local political developments for the next few weeks, the global cycle remains crucial for South African markets. As we saw in 2021, a surge in global commodity prices gave the economy and its markets a lift despite serious domestic infrastructure constraints. On the other hand, a global downturn will have the opposite effect.

These factors are largely out of our control, and on top of it all, we might need to wait for an extended period until there is more certainty, but we can choose how to respond to them. On election day, many voters had to wait for hours for the chance to cast their votes, but their patience was ultimately rewarded. There is a lesson there for investors too. Moreover, it is precisely for uncertain situations like these that diversification is so important. Global and rand-hedge exposure will do well (all else equal) should a market-unfriendly coalition emerge, while South African assets can rerate under a ‘Grand Coalition’ scenario. And it is precisely for such situations that a long-term investment plan is necessary to avoid a knee-jerk reaction, especially since there is bound to be much rumour and speculation in the uncertain days ahead.

ENDS