Izak Odendaal, Investment Strategist, Old Mutual Wealth

South Africa, Mexico and India announced election results a few days apart. In the one, the continuity candidate won a solid majority. In the other, the ruling party suffered a heavy defeat, and must now cobble together a coalition. In the third, the popular prime minister will return for a third term, but without a parliamentary majority. In each case, markets were negatively surprised, but for very different reasons. Elections are hard to forecast, and the consensus is often wrong. The longer-term implications of such a political surprise are also difficult to determine, while investors often shoot first and ask questions later.

Comparing these three very different emerging markets is an interesting exercise in thinking about how politics, economics and markets intersect. While each of these countries is complex and there isn’t space here for nuance, there are still lessons for South African investors as they sail into unchartered political waters.

What’s GNU?

Starting at home, the past week has seen intense discussions within and between parties on various cooperation and coalition possibilities. This is new terrain for a country that has been governed by one party for the past thirty years.

There is strong disagreement within parties about who they should and shouldn’t partner with. Holding your nose and working with people you don’t like is part and parcel of coalition politics, but again, this is new terrain.

The ANC has invited all other parties to join a government of national unity (GNU), which is simply another form of a coalition. So far, a few parties have ruled out participation. Most notably, this includes the EFF and MKP.

Therefore, it still seems that the outcome investors fear most – a leftist-populist coalition – will not materialise. Nothing is guaranteed, however, and it will ultimately depend on whether the ANC and DA can reach an agreement, since they are the two largest parties with 62% of the votes between them.

The DA could join the GNU, or support it as a minority government, voting for key legislation such as the Budget (known as the “supply and confidence” model). Either arrangement would be welcomed by the business and investor communities.

If the DA and ANC cannot come to an agreement, the EFF could still join the GNU, which would hurt investor sentiment, given the party’s stance on property rights and fiscal policy. However, with a weaker election performance, the EFF will not be entering such a coalition on the front foot and will not be able to impose its policies on its coalition partners. Among other things, this means the ANC will still appoint the finance minister.

The main question, as discussed before, is whether South Africa gets an acceleration of growth-enhancing economic reforms, fiscal discipline, increased emphasis on the fight against crime and corruption and improved delivery of basic services. Populists and ideologues always reach for silver bullets, but there are none. Fixing South Africa requires the hard and tedious work of getting the basics right every day.

Whatever governing arrangement emerges in the next few days, political uncertainty will not go away. Coalitions can unravel at any point, including at some of the big upcoming events on the political calendar: the ANC’s policy conference (National General Council) next year, municipal elections in 2026, and the ANC’s elective conference in 2027.

South African assets can enjoy a relief rally if a market-friendly coalition comes to power, but the real value will probably only unlock when there is evidence of faster growth, better governance and debt sustainability. And, of course, a conducive global climate. In other words, whatever happens in the next week, good or bad, will not be the end of the story. Investors will still need to remain calm and be patient.

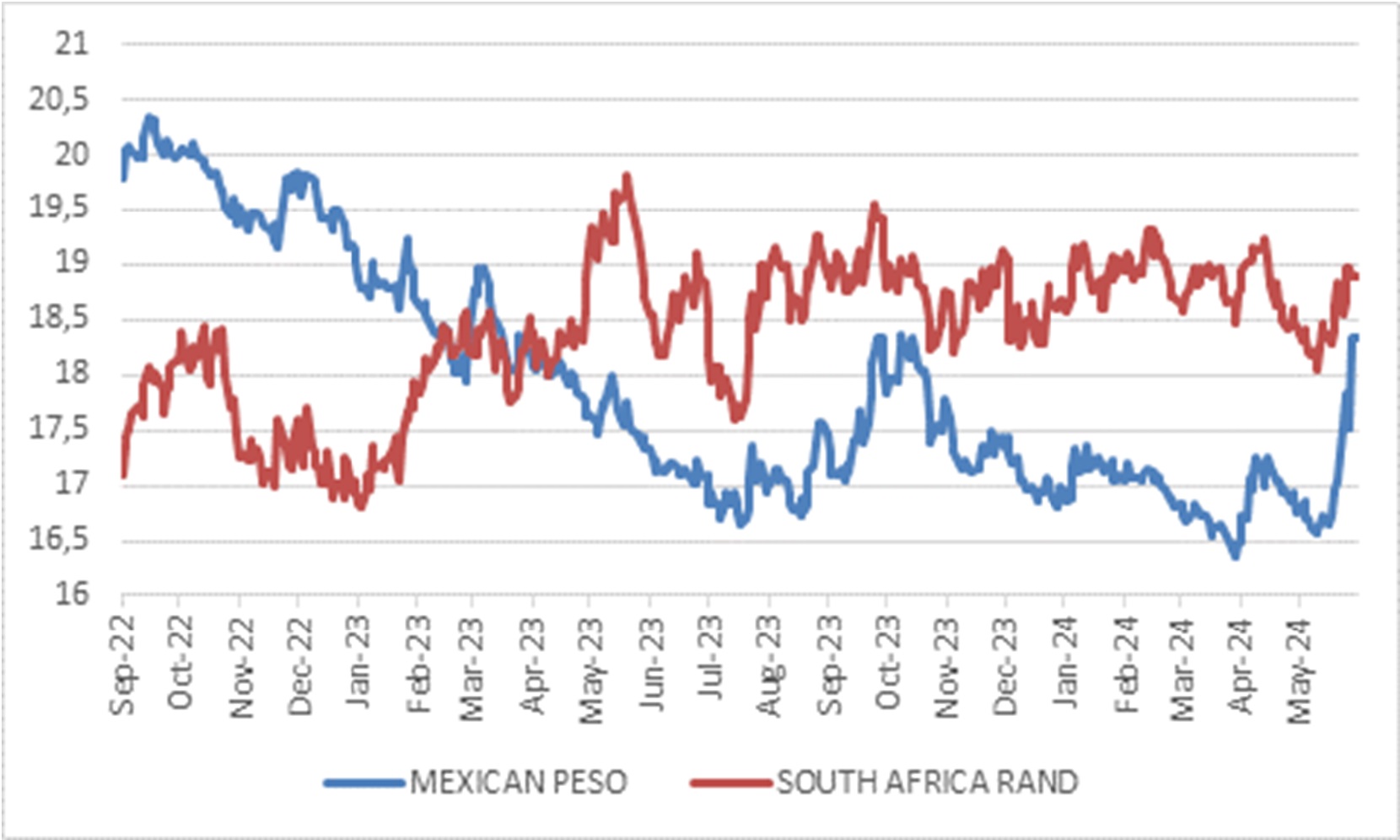

Chart 1: Cost of one US dollar

Source: LSEG Datastream

So far, so close

As for Mexico, its troubled past is summed up by the famous quote from a 19th century president, Porfirio Diaz: “Poor Mexico, so far from God and so close to the US.” This closeness to its giant northern neighbour has been destabilising in the past through wars and the present through the impact of powerful drug cartels. But it still offers much promise. Having the world’s largest consumer market on your doorstep at a time when it wants to trade less with China and more with friends is handy, and Mexico is indeed experiencing a manufacturing boom as exports to the US surge.

Importantly, Mexico has also managed a far greater degree of macro-stability in recent years, having been the victim of major financial crises in the 1980s and 1990s. As with most emerging markets crises, the root cause was excess borrowing in dollars, compounded by rising US interest rates and a strengthening greenback. The fact that Mexico survived the most recent US Federal Reserve hiking cycle relatively unscathed is telling. In fact, by maintaining high short-term interest rates, the Mexican central bank made the peso (technically the “new” peso; it was introduced in 1993) a favourite for carry trade players.

That is, until it plunged 7% in the wake of the election outcome, one of the biggest weekly moves since the “Tequila Crisis” of 1994.

Claudia Sheinbaum, the handpicked successor of the popular outgoing president Andres Manual Lopez Obrador (known widely as AMLO) won a landslide victory, making her the first woman elected to Mexico’s highest office. With a close to two-thirds majority in Congress, investors are worried about a weakening of constitutional checks and balances and an unsustainable increase in government spending. While AMLO was fiscally conservative, which is unusual for a leftist-populist, that might change now under Sheinbaum’s proposals to expand public pensions. AMLO tried to weaken the judiciary and independent regulators who he accused of blocking his legislative agenda, and the worrying plan to have top judges directly elected is still on the table.

Institutions matter. The old dictum is that power corrupts, and that absolute power corrupts absolutely. Even good leaders can be dangerous if given too much control. Bad leaders without guardrails are downright destructive, however.

South Africa has many strong institutions – independent judiciary, a credible central bank, free press, regular fair elections – but Parliament has always been an underperformer, being largely subservient to the executive branch. This looks set to change, and Parliament could be a much more active and important branch of government, providing better oversight.

South Africa’s constitution is also a guardrail, and broadly respected by most political parties, as signified by the ANC’s quick acceptance of its election loss. It is the parties that don’t respect the constitution that concerns investors, though without a two-thirds majority, they have no hope of changing it.

Financial markets are another constraint on power. As Mexican markets tumbled, its finance minister called a hasty press conference to reassure investors there would be continuity with fiscal discipline. Markets have a way of disciplining politicians, sometimes even before they are elected. It might seem unfair that capital can overrule the electorate, and perhaps that is overstating it somewhat. But money does talk. And politicians that have a habit of borrowing large amounts of money must listen. Even UK prime minister Lizz Truss discovered this in 2022 when she tried to ram through a reckless budget. The bond market blew up, sinking her short-lived premiership.

The question is whether the incoming South African and Mexican administrations will heed this message or relearn the lesson the hard way. In South Africa, at least, we are likely to see reassuring continuity in terms of the political and bureaucratic leadership at National Treasury.

No majority

In India, prime minister Narendra Modi’s Bhartiya Janata party unexpectedly failed to win an outright majority of parliamentary seats after the marathon six-week election. It appears that Modi’s emphasis on Hindu nationalism failed to stir an electorate more focused on bread-and-butter issues. Similarly, his closeness to big business and fondness for the global stage might have put off millions of voters who still live precarious lives in slums and villages.

Modi will serve a third term with the help of coalition partners, however. In fact, coalition politics is standard in India, and the main opposition parties also operate as a coalition. If India, a continent-sized and mind-bogglingly diverse country can manage coalitions, so can South Africa. However, unlike South Africa where coalition negotiations could still take several days if not weeks, the BJP came into the election with a partnership arrangement and the government can hit the ground running.

The negative market response to the election outcome was mainly an equity story, unlike Mexico and South Africa where bonds and currencies were also in the firing line. Indian equity indices reached an all-time high on the eve of the results announcement, as exit polls pointed to a solid BJP victory. Modi’s strong emphasis on infrastructure spending, closeness to the big conglomerates, and reputation as a decisive ruler who can cut through the notorious tangle of Indian red tape, made him very popular among equity investors.

Chart 2: Forward price: earnings ratios

Source: LSEG Datastream

However, the stock market was priced for perfection with a forward price: earnings ratio of almost 23x, and there was much room for disappointment. In contrast, South Africa’s markets are already priced for disappointment.

Compared with the pedestrian Mexican and South African economies, India’s growth story remains remarkable. And to the extent that this election outcome strengthens India’s democratic institutions, the long-term outlook has, if anything, improved.

With high savings rates and still-low levels of GDP per capita and infrastructure, it can sustain rapid rates of economic growth for years to come. It wasn’t always this way. In the decades since independence in 1947, India underperformed its obvious potential due to restrictive socialist policies. Only when market-oriented reforms started in 1991 and accelerated over the past decade, has it become the darling of investors. As recently as 2013, India was still part of the Fragile Five, the unfortunate club of emerging markets that included South Africa. Today it stands alone as the fastest-growing large economy, with a booming market and rising self-confidence.

Chart 3: Real GDP growth, local currency

Source: LSEG Datastream

In contrast, South Africa’s growth performance has only worsened since 2014 (though its current account deficit is no longer as alarming). Reversing this decline should be priority number one for the new government as the only hope of sustainably addressing the challenges of poverty and unemployment.

Two final thoughts

Firstly, markets often overreact to political events. India’s stock market has already recovered most of its losses, for instance. South African markets can still experience volatility in the days ahead, especially if the GNU that emerges includes parties with destabilising economic policies. But the bigger driver of long-term market returns are not headline-grabbing events, but the more mundane business of cash flows, such as the profits that companies generate. Economic policy does play a role in the business climate, and therefore it is policy that matters, and what investors should pay attention to, not politics. Put differently, focus on what politicians do in the months and years to come, not what they say.

Secondly, the initial market response to each of these unexpected election results also demonstrates again how difficult it is to make investment decisions based on predicting a specific outcome, such as an election result. This is particularly true as the most important and probably most uncertain election this year still looms, namely the US presidential vote in November. It is better to be diversified than to forecast.

ENDS