Justin Floor – Head of Equities and John Gilchrist – Co-CIO

Investing, by its very nature, requires that managers to take on some form of risk. However, risk is a complex concept, and how it is defined can impact the decisions fund managers make. At PSG Asset Management, we believe the most crucial risk for most clients is not meeting their return objectives over the long term. This can occur because clients are invested in a fund that underperforms the objective (or experiences a permanent capital loss), or because a client exits a fund at the wrong time (potentially due to short-under performance), crystallising losses.

Asset managers must therefore strive to find a balance between maximising long-term performance and ensuring that short-term performance does not disappoint investors to such an extent that they divest. However, these objectives can frequently be in conflict.

The history behind the focus on volatility

While Harry Markowitz introduced ‘volatility’ as a proxy for risk in 1952, market participants only started thinking of volatility as risk after the 1987 Black Monday market crash. JP Morgan developed a report estimating the ‘maximum’ the bank could lose on any given day. This report used historical volatility as an input, and led to the development of Value at Risk (VaR). In 1993, JP Morgan made its methodology freely available, ultimately leading to historic volatility becoming the de facto measurement of risk in the investment industry.

Shortfalls and risks of using volatility as the sole measure of risk

Actual portfolio risk is incredibly difficult to assess, so it is no wonder that the finance industry has embraced one easy-to-calculate measure, despite its numerous shortfalls and flaws. However, relying too heavily on volatility as a risk measure has significant drawbacks.

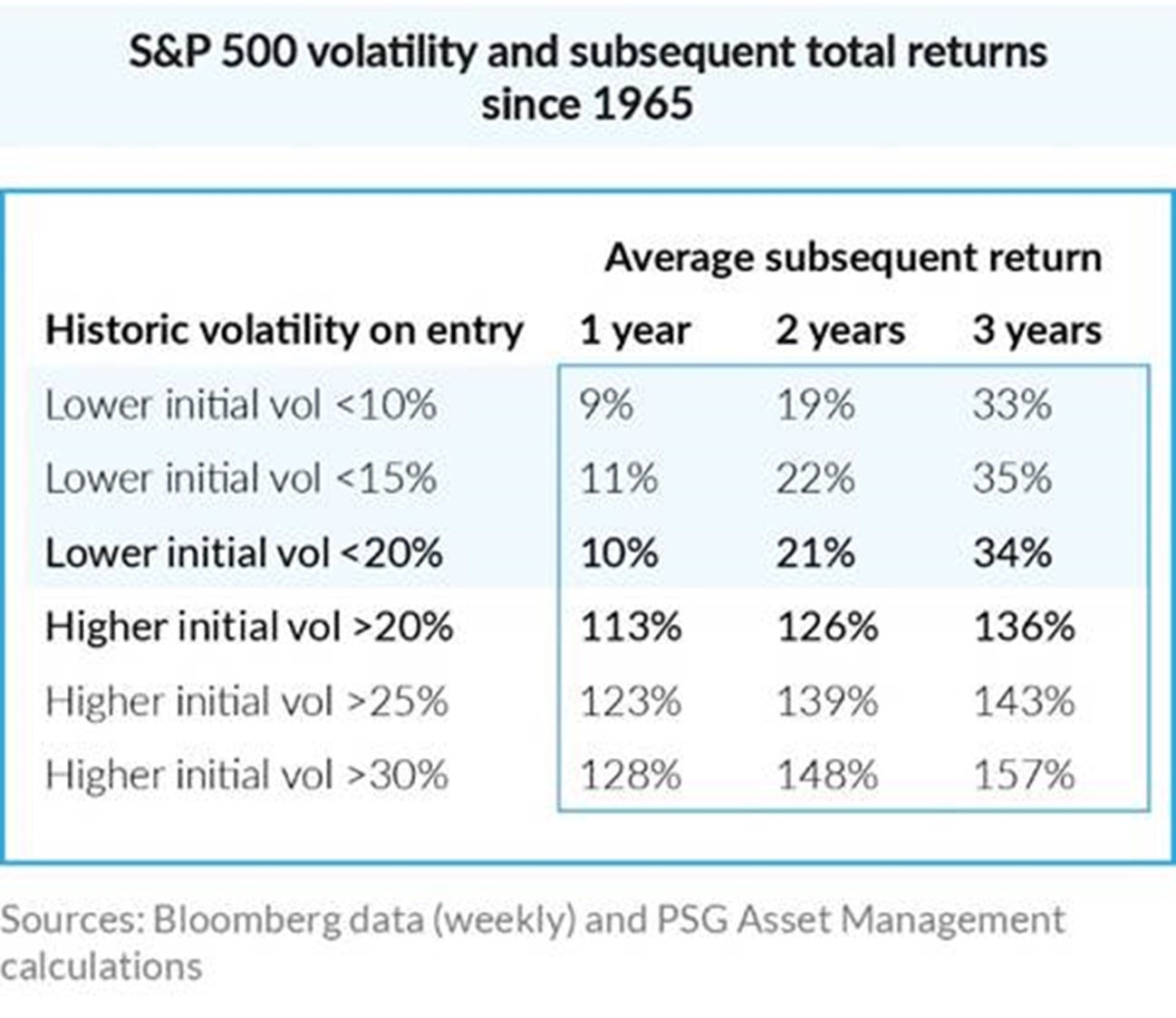

Volatility is backward looking

Historical volatility has a correlation with market moves – when markets fall volatility rises, while in bull markets volatility tends to flatline or decline. Using volatility as a risk measure implies assessing risk as higher after a fall in the market (and rise in volatility). Conversely it would imply risk is lower after a market rally. This is counterintuitive – we believe the price you pay for an asset is a critical driver of both potential performance and the risk of permanent capital loss. Historical data supports our view:

The underlying assumptions are flawed.

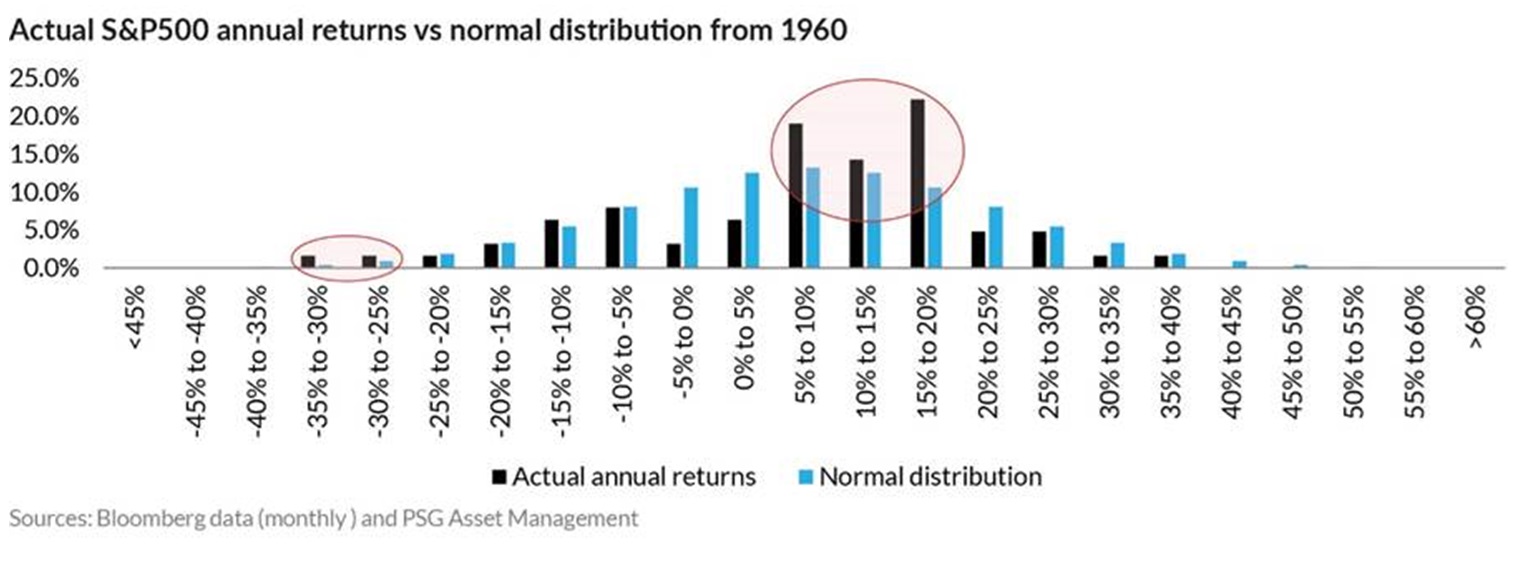

Using volatility as a risk measure implicitly assumes that market returns are normally distributed. However, when comparing actual annual S&P 500 returns to a normal distribution with the same mean, it is evident that there are more actual observations around the mean and in the left tail than a normal distribution assumes. This, in turn, means that many assumptions about risk based on volatility are flawed.

These assumptions can be even more flawed when volatility is used to assess the risk of multi-asset funds that, by design, do not display normal pay-off profiles.

It does not distinguish between upside and downside volatility

Focusing only on volatility ignores the distinction between desirable upside volatility, and volatility associated with losses. On occasion, funds seen as high risk due to elevated historical volatility are being unfairly penalised for lumpy upside performance. Downside deviation addresses this by measuring only the volatility associated with negative returns.

It is short-term focused

Ideally, investors should focus on risk measures consistent with their relevant time period. While monthly volatility may be relevant for selected investors, most investors in multi-asset or equity-centric funds have a longer-term time horizon. Measuring risk based on monthly moves creates a short-term focus with potentially negative implications for investors’ ultimate returns.

It is not necessarily a reliable predictor of the potential to lose money

There have been numerous examples of instruments and funds that have displayed extremely low volatility, were seen as low risk, but whose value precipitously dropped, sometimes to zero. Two high-profile examples:

- Credit Suisse’s Additional Tier 1 (AT1) bonds which were written off by the Swiss Financial Market Supervisory Authority as part of the forced rescue merger with UBS in March 2023.

- Bernie Madoff’s ponzi scheme: Of the US$65 billion of purported client assets, less than US$15 billion in cash deposits were returned to investors (a 77% loss).

Fund volatility can be reduced artificially

Some funds and instruments apply opaque mark-to-market processes, which can result in artificially low volatility of returns. We believe an excessive focus on volatility is currently contributing to demand for credit investments at unattractive spreads in the local market, and is also driving greater investment in illiquid bespoke products. Volatility as a measure of risk is a potentially misleading indicator for funds that make extensive use of these instruments.

What is the antidote?

While historical volatility as a proxy for risk is clearly flawed, it is relatively simple and objective and is likely to remain a key part of any investor’s due diligence processes. However, we believe that it is crucial that risk be considered holistically, with both a quantitative and a qualitative assessment.

Leading multi-managers, institutional investors, discretionary fund managers and sophisticated advisers all conduct extensive due diligence processes on investment managers, gaining insights into how they construct portfolios. We believe this is crucial to ensure that risk is assessed properly. In addition, while an individual fund may appear risky on a stand-alone basis, each fund needs to be assessed in conjunction with other funds it may be combined with in a solution. This is particularly relevant for funds managed on a similar basis to those of PSG Asset Management, as we do not construct our funds using benchmarks or strategic asset allocations, and hence can add significant diversification benefits.

ENDS