Matiisetso Madito, Chief of Credit Bureau Services at Experian South Africa

As South Africa marks Youth Month, new data from Experian’s Consumer Default Index (CDIx) reveals a stark reality: despite making up nearly a quarter (24%) of the adult population, the nation’s youth are largely excluded from the formal credit economy. They hold just 10% of active credit accounts and a mere 4% of the country’s R2.39 trillion in outstanding debt, pointing to barriers that are creating a generation of ‘credit invisibles’.

When young people access credit, they tend to show a strong affinity for Vehicle Asset Finance and Retail Loans, while their exposure to high-value assets like Home Loans remains incredibly low at just 1% of the total youth credit exposure. As a result, their overall contribution to the nation’s outstanding debt value remains minimal.

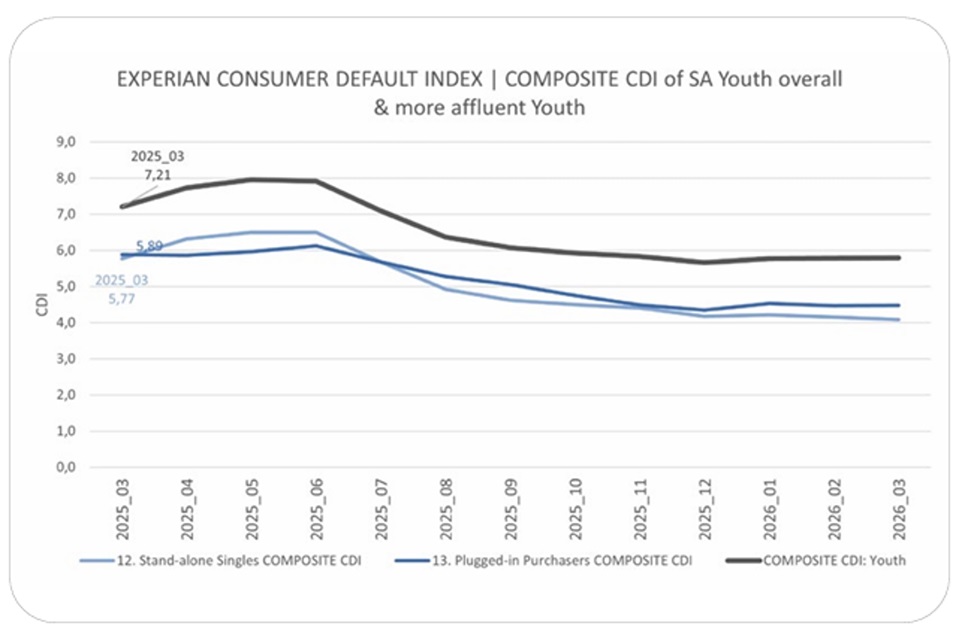

The Experian CDI, which measures the rate at which South African consumers default on their loans for the first time across home, vehicle, credit card, personal, and retail accounts, shows that the default index for youth (aged 20-29) fell from 7.21% in March 2025 to 5.79% in March 2026.

Typically, lower default rates signal a healthier consumer base, but in South Africa’s current macroeconomic climate, the reality is far more nuanced.

“With youth unemployment remaining high, lenders have naturally adapted their risk frameworks, resulting in fewer young people qualifying for new credit products,” says Matiisetso Madito, Chief of Credit Bureau Services at Experian South Africa. “While lower default rates among our youth may seem like good news, it’s a hollow victory if they are being omitted from the financial system altogether. With youth unemployment at a staggering 40.6%, we are witnessing the creation of a ‘credit invisible’ generation. This isn’t just a challenge for young people; it poses a growing risk to the broader national economy. Sustainable entry into the financial system is essential to helping the next generation build a stable economic foundation. Our focus must be on finding ways to responsibly and sustainably include them, not exclude them.”

A national credit market of contrasts

Beyond the youth demographic, the CDI for Q1 2026 indicates a highly fragmented national credit market characterised by a clear divide in consumer behaviour, where consumers are carefully choosing which commitments to prioritise.

The Home Loan sector recorded the most significant improvement, with its CDI dropping by 16% year-on-year (from 2.21% to 1.86%). This suggests that mid-to-high-affluence consumers, who hold the vast majority of mortgage debt, are actively protecting their primary properties.

Conversely, unsecured credit products are showing signs of persistent stress. Retail Loans, often utilised as entry-level credit products, deteriorated by 11% year-on-year (rising to 17.18%). Personal Loans also experienced a 4% year-on-year deterioration. This contrast confirms that while established assets are being safeguarded, everyday household budgets remain under severe pressure.

High demand met with tight controls

The CDI for Q1 2026 indicates that consumer appetite for credit remains exceptionally high, driven by the persistent gap between household incomes and rising living costs. Following the usual post-festive season slump in January, the volume of credit applications rebounded strongly in the first quarter of the year.

However, actual approvals have continued to decline. This indicates that financial institutions are maintaining highly cautious risk management strategies to shield both their portfolios and consumers from the risks of over-indebtedness in a volatile macroeconomic environment.

“This is a climate where credit health education is more critical than ever. Both consumers and lenders are navigating incredibly tight margins. For young South Africans especially, understanding how to manage credit conservatively from the very start of their financial journeys is key to long-term economic resilience,” concludes Madito.

South Africans can take control of their financial future today by visiting the Up web-based app at www.up.experian.co.za.

ENDS