Shaun le Roux and Mikhail Motala Fund Managers at PSG Asset Management

Equity markets have continued to power ahead in 2025 despite macro uncertainty and the reshaping of the global world order. This development has caught many investors by surprise, especially given that US equities in general and mega tech shares in particular are trading at extremely elevated valuations, driven by exuberance around artificial intelligence (AI). But how long will the run in equities continue, and are there still opportunities to be found in very concentrated and expensive markets?

Not all equities are equal

While equities will be indispensable in client portfolios going forward, not all equities are equally well positioned to continue rewarding investors in the future. Owning the right equities will be key. Investors must look outside the popular areas of the market, with local equities specifically poised to offer some attractive opportunities.

Equities will have a key role to play in portfolios in a changing world

One of the key features of the new economic world order is that it will be marked by higher levels of global inflation. The monetisation of debt and ongoing fiscal deficits, especially when coupled with dovish monetary policy in the US, set the stage for a more inflationary environment.

Furthermore, rising protectionism will also add to existing inflation pressure, augmented by a weaker US dollar and tight labour markets. In such an environment, G7 (developed market) bonds are likely to be a poor store of value and equities will be essential to protecting investors’ wealth in the long run.

While equities are going to be needed to generate the appropriate real returns, certain sectors are unlikely to deliver the required returns. Real assets and precious metals typically fare well in more inflationary environments, while emerging markets benefit from weaker dollar cycles. However, we believe these equities are especially well positioned to reward investors into the future, as they are currently deeply out of favour and trading at far less rich valuations than their popular counterparts. A similar case can be made for global value stocks, which have been chronically trailing growth stocks for far longer than is typically the case in investment cycles.

In this article, we specifically look at the opportunity set we see in the local market.

Many investors are not positioned correctly to benefit from local equities going forward

Generally, shares perform well in inflationary environments, and from this perspective, the equity bull run for the year to date is understandable.

What is concerning, however, is that many investors’ portfolios have a disproportionate weighting to the US. This is partly a reflection of the exceptional returns US shares have delivered over the past few years. SA investors not only bought into this ‘US exceptionalism’ narrative, but have also tended towards being conservative in their allocation to local assets, seeing SA equities as ‘risky’ because of pessimism towards the local economic and political landscape.

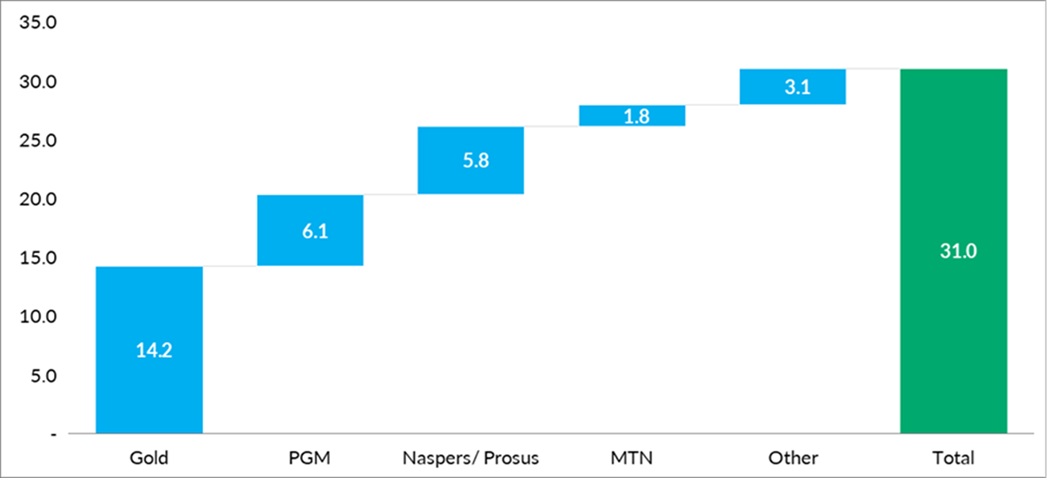

Many investors have been surprised by the exceptional performance delivered by local equities so far this year. What investors have tended to lose sight of, is that the JSE is not representative of the SA economy. Some 54% of JSE Capped SWIX constituents are not SA Inc. companies. In fact, SA Inc. shares have lagged so far this year, while precious metals and commodities have done very well, buoying index returns. Deconstructing the 31% shows that gold miners contributed 14%, Naspers and Prosus 6%, platinum miners 6% and MTN 2%, meaning everything else in the index contributed 3%. SA Inc. shares outside of the banks, experienced particular pain.

Sources: PSG Asset Management and Bloomberg

The SA index’s appeal rises in a commodity bull market

Commodities are very influential in the South African economy and commodity stocks currently comprise 25% of the ALSI. Most investors have been bearish on commodities in recent years given the underperformance over much of the past decade – another reason why demand for SA equity funds has been lacklustre. PSG has a positive outlook on several commodities (including gold, PGMs, copper and coal), all of which are well represented in our market. In previous bull markets, resource stocks comprised in excess of 50% of the ALSI (in the 1970s and early 2000s). In the event of a new commodity bull market (which we think is quite likely over the next five years given the low level of additions to commodity capacity over the past decade) it is reasonable to expect strong relative performance from the JSE.

Overall, the SA market remains attractively priced

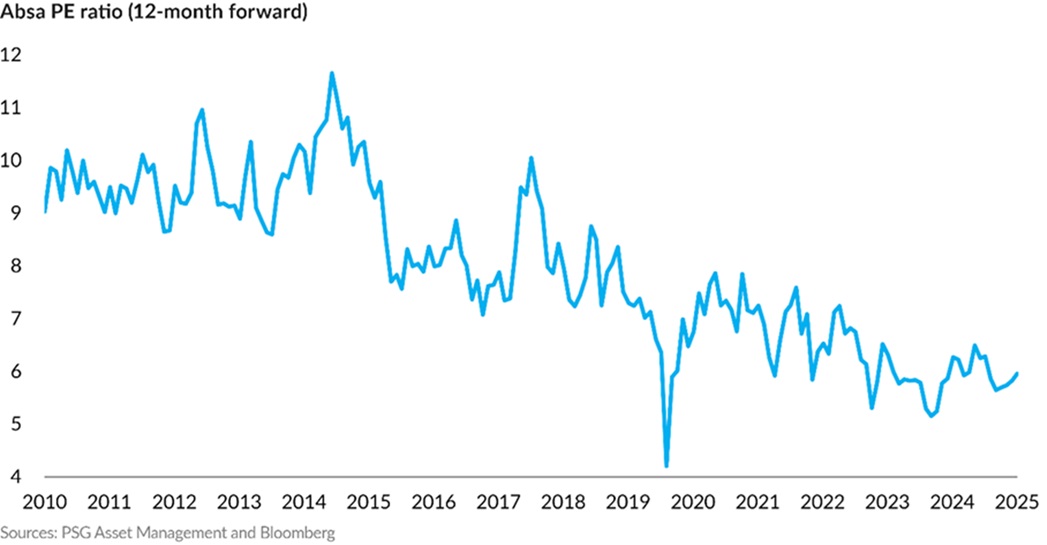

Despite the rally, many constituents of the South African market offer attractive value. The largest SA Inc. sectors are the banks, and across the banks, the cheapest one on traditional valuation metrics is Absa. Absa trades on a 6x PE and 8% dividend yield (not far removed from the yield currently received on the 10-year SA government bond, which has rallied sharply in recent months). The dividend per share has compounded by 7% p.a. over 15 years from 2010 to 2025, a period that has been tough for South Africa and where the term ’polycrisis’ was appropriate. If that dividend growth can be maintained, Absa offers a 15% total return absent any positive rerating in the PE ratio, which at a starting multiple of 6x carries a reasonable probability.

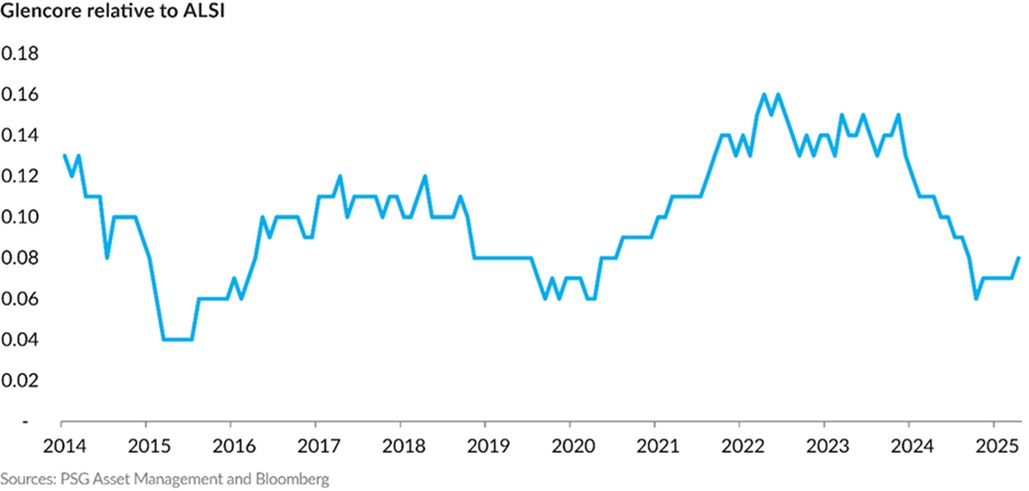

Undervaluation is not only evident in SA Inc. In the diversified mining sector, Glencore is also undervalued. The stock is trading at lows relative to the market, at similar levels to 2020, and has only been cheaper in 2015 when the balance sheet was much weaker than it is now.

The changing macro environment is likely to benefit emerging markets like SA

While no-one knows what the emerging global world order will ultimately look like, investors should be worried about continued positioning into some of the most expensive and crowded parts of the US markets, as it is highly unlikely that hype will be matched by economics in the long run. Importantly, valuations in SA equities are incredibly cheap compared to those in US markets, which are almost showing some bubble-like characteristics.

ENDS