Kim Silberman, Macro Economist and Fixed Income Strategist at Matrix Fund Managers

US policy decisions are a primary driver of EM asset performance. The Trump administration’s shift away from the predictability of a uni-polar, US-led, rules-based world order to one that is multi-polar, necessitates that investors adopt a new frame of reference to benchmark US policy decisions. Although Trump administration policies may appear reactionary and disparate, in this note we show ways in which they are coordinated and deliberate and less unpredictable.

In May 2025, Moody’s downgraded the US to Aa1, citing concerns around Fed independence, fiscal deficits and policy uncertainty. Heightened uncertainty has increased the risk premium associated with US assets, and investors have repriced dollar-denominated assets accordingly. Emerging market bonds and equities look relatively less risky, which has prompted a structural shift into these assets.

US policy aims to immunise against economic and geopolitical chokepoints

The Trump administration’s economic policy has been well articulated by the US Treasury Secretary’s National Security Strategy (November 2025). Policy choices are intended to reduce the US’s vulnerability to geographical and economic chokepoints, while simultaneously relinquishing its role as keeper of world order and consumer of last resort. Key tenants are 1. rebalancing the trade deficit 2. returning to fiscal sustainability and 3. ensuring energy independence. More specific goals include US technological dominance, reduced reliance on foreign supply chains and securing critical materials. These are the policy objectives that will guide asset prices and global financial flows.

In his first term, Trump brokered the Abraham Accord, an alliance between the US and Arab nations aimed at cementing regional stability and countering Iran’s role as “the region’s chief destabilising force”. An excerpt from The National Security Strategy provides useful insight:

“America will always have core interests in ensuring that Gulf energy supplies do not fall into the hands of an outright enemy, that the Strait of Hormuz remain open, that the Red Sea remain navigable, that the region not be an incubator or exporter of terror against American interests or the American homeland, and that Israel remain secure. We can and must address this threat ideologically and militarily without decades of fruitless “nation-building” wars.”

The Iran war should be viewed in this policy context. The US’s primary goal is reducing supply chain risks through control of the Strait of Hormuz – the world’s most critical chokepoint with respect to crude oil and its multitudinous derivatives.

The US has been given too much rope

The current account deficit can only be financed by “ever-larger portfolio and direct foreign investments in the United States, an outcome that cannot continue without limit.”

Alan Greenspan, March 2000

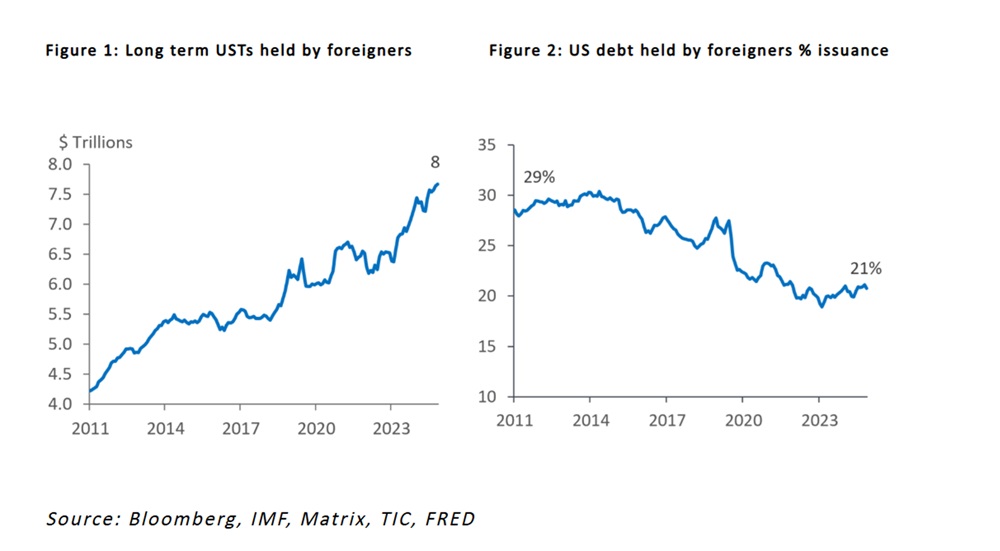

The US is in a vulnerable position. China has hollowed out US domestic manufacturing capacity, leaving the country dependent on imports, and foreigners finance its fiscal deficit. Even though foreign purchasing of long-term US debt has accelerated (Figure 1), it has fallen as a % of issuance (Figure 2).

US vulnerability is being tested by the current administration’s decision to weaken ties with old allies. Unwinding the country’s trade and fiscal deficits is aimed at reducing this vulnerability, but it will also be painful.

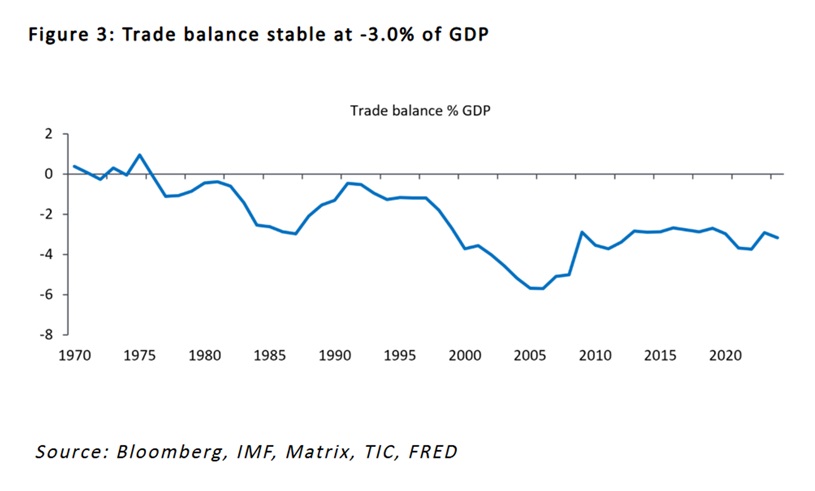

The two deficits fuel each other: the trade deficit ensures that the rest of the world has a net surplus of dollars, which return to the US via investment in US bonds and equities. Its reserve currency status of the USD has allowed the US to run ever-widening deficits without triggering currency depreciation, or a rise in bond term premia. Guaranteed funding has seen successive US administrations use fiscal and monetary policy to truncate recessions and reinflate growth. Without increased productivity, this has helped fuel a series of bubbles, including dollar overvaluation, house prices, consumer and government debt, and import reliance. We expect the policy response to the current twin deficit excesses, will be more of the same. The Trump administration will do everything possible to cushion the pain, and with limited room for fiscal stimulus, monetary policy will need to do most of the work. Investors should expect policy to favour a weaker dollar and accommodative monetary policy. This goes some way to explaining the attack on US central bank independence.

Figure 3: Trade balance stable at -3.0% of GDP

Reinflating bubbles, again

The structural decline in US real GDP growth since the 1970s is primarily due to weak productivity growth and demographics. Economists estimate that long-run growth will continue to slow to an estimated 0.9%.

Policy has failed to address these underlying causes and has compensated for them by allowing the economy to run hot, encouraging increased leverage in both the financial and real sectors.

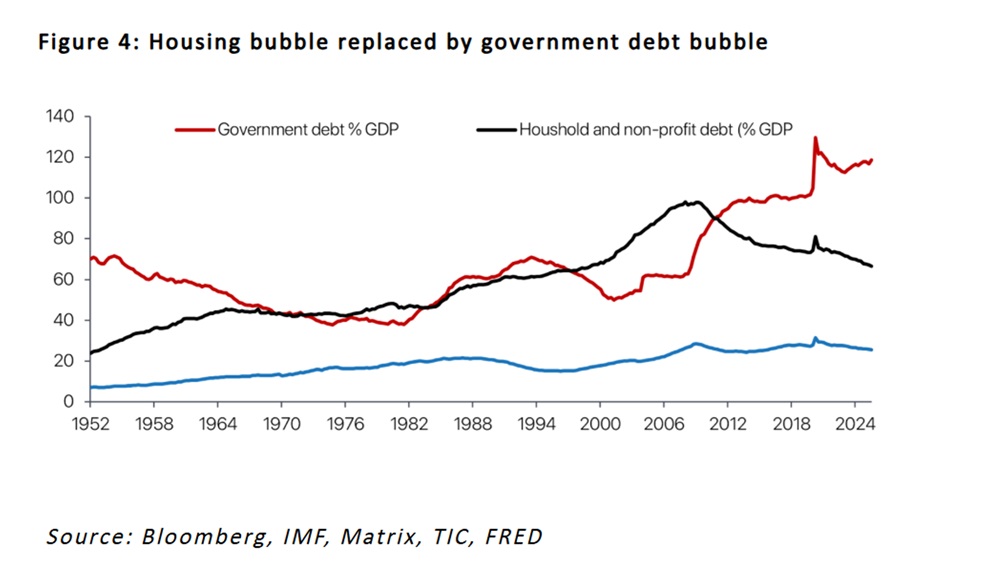

Growth in the years leading up to the 2008 global financial crisis (GFC) was fuelled by lax regulation and irresponsible US consumer credit policy, characterized by an unsustainable expansion of subprime mortgage lending to unqualified borrowers. The resultant housing price bubble triggered the GFC, and government’s response – bailouts, fiscal stimulus packages and quantitative easing, replaced the consumer debt bubble with a sovereign debt bubble (Figure 4). Government debt rose to 105% of GDP in 2015, where it stayed until COVID related spending saw it breach 120% of GDP.

Policy responses since 2008 have been criticised for exacerbating income and wealth inequality while not addressing the decline in real GDP growth. Quantitative easing benefits those who own equity and property, without transmitting such benefits to citizens who are not owners of those assets. In the absence of redistributive tax measures, inequality has motivated US citizens to vote for more populist candidates who promise change and the opportunity to “Make America Great Again”.

US fiscal consolidation requires low real interest rates

Fiscal consolidation is an economic imperative for the US.

We estimate that for US debt to stabalise as a % of GDP, it’s primary budget (i.e. the main budget balance excluding debt service costs) must be close to -0.4% of GDP, a far cry from its current -4.0% of GDP. In dollar terms, this requires spending cuts of USD1.13Trn, or 13% of total spending.

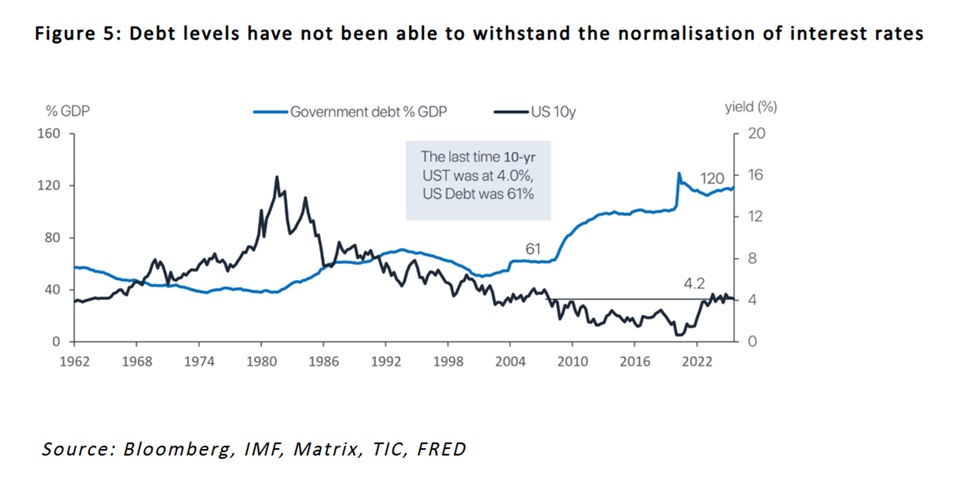

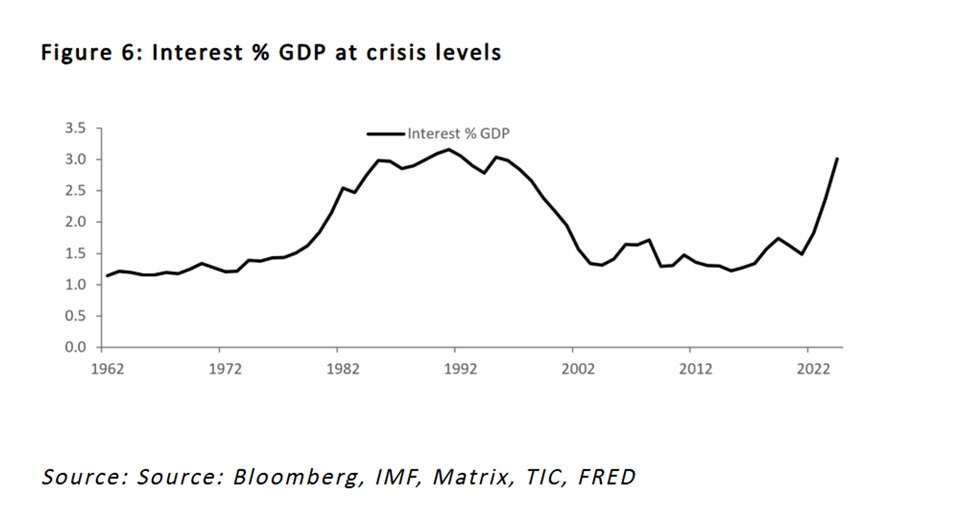

Quantitative easing between 2008 and 2015 saw government debt rise to levels which cannot withstand the subsequent normalisation of interest rates (Figures 5 & 6). Since COVID, spending on interest has grown by on average 36% per annum and are at crisis levels. To put fiscal risk in context, the last time interest was at 3% of GDP was during the Great Inflation of the 1970s (Figure 6). Then Federal Reserve Bank, Chair Paul Volcker raised the Federal Funds rate to a peak of 20%, causing unemployment to rise to 11%.

“Our elites badly miscalculated America’s willingness to shoulder forever global burdens to which the American people saw no connection to the national interest. They overestimated America’s ability to fund, simultaneously, a massive welfare regulatory-administrative state alongside a massive military, diplomatic, intelligence, and foreign aid complex.” (National Security Strategy of the United States of America, November 2025).

The Trump administration’s policy response is broadly twofold: import substitution to generate real GDP growth and financial repression. Import substitution requires currency manipulation (a weaker dollar) and tariffs. “Financial repression” refers to inflating away debt by maintaining government borrowing costs below nominal GDP growth for an extended period. Governments engineer this by running loose monetary policy to generate moderately above-target inflation, boosting fiscal revenue. Increasing issuance at the front of the curve lowers debt service costs – 83% of US debt stock has a maturity less than 10-yrs.

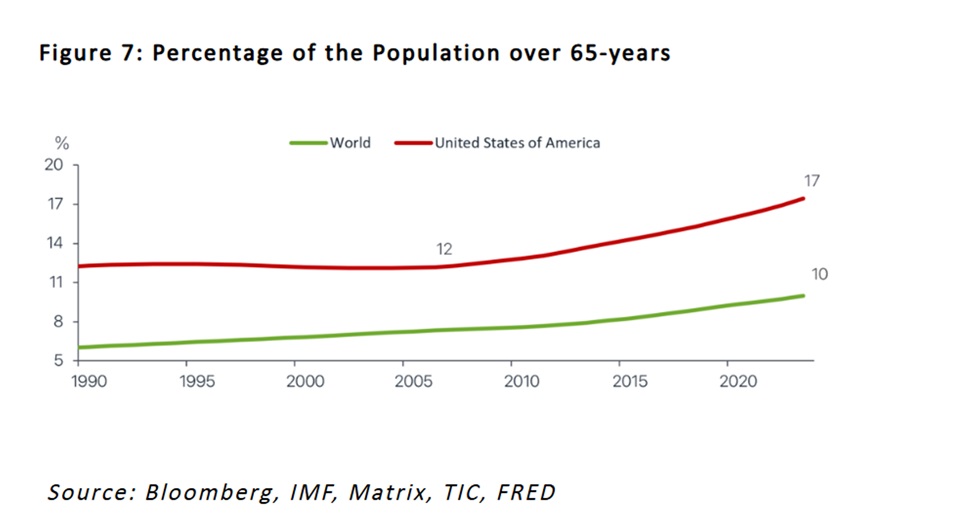

There is limited space to consolidate by reducing spending due to the fiscal burden of the US’s aging population. The percentage of the population aged over 65-years has grown from 12% in 2008 to 18% currently, versus a global average of 10% (Figure 7). Aging boomers will require significant increases in benefit expenditures (Social Security, Medicare and Medicaid), which already account for 54% of spending, up from 41% of spending in 2020. Including interest costs, mandatory spending is 70% of GDP. Attempts to reduce non-mandatory spending through DOGE (the Department of Government Efficiency) were unsuccessful amid backlash and legal challenges.

The Trump administration is well aware of the negative implications of higher inflation in combination with relative fiscal austerity, especially for those who don’t benefit from rising asset prices. To buffer inflation and keep long-term expectations anchored enough not to send long-end bond yields soaring and real wages falling, supply-side reforms include. 1. reducing the supply of labour through immigration policies, to protect wages; 2. controlling the oil price and 3. draining liquidity from the economy by running down the Fed balance sheet. The Fed chair-in-waiting, Kevin Warsh, has made it clear that he will comply.

Conclusion

The shift from a predictable, US-led global order to a more fragmented, multi-polar system fundamentally alters the investment landscape. The US enters this transition from a position of structural fragility. Supply chain dependencies, elevated debt levels, dependence on foreign capital, and declining productivity constrain policy choices.

For investors, the implication is clear: the traditional safe-haven status of US assets can no longer be taken for granted, and macro volatility will remain elevated. US policy is now explicitly geared toward reducing structural vulnerabilities even at the cost of a weaker currency, higher inflation, less credible institutions, and risk of renewed asset bubbles. The Iran conflict should be viewed through this lens: control of strategic chokepoints like the Strait of Hormuz is not incidental, but central to US economic and security objectives. While emerging markets may benefit from capital rotation away from the US, event risk has increased.

ENDS

___________________

[1] Trade deficits are negative if they are dominated by consumption goods as opposed capital and machinery to increase manufacturing productivity