Eugene Botha, Head: Research Hive at Momentum Investments

Passive investing is a popular option for global investors, but this is not evident in South Africa. Historically, the popularity of passive investment funds has varied by region. Globally over the last couple of years, we have seen an enormous shift in the market away from active funds to passive investment vehicles. This shift has been largely due to the infamously low success rate of active managers outperforming the market index, but other factors also drive the growth in passive investing.

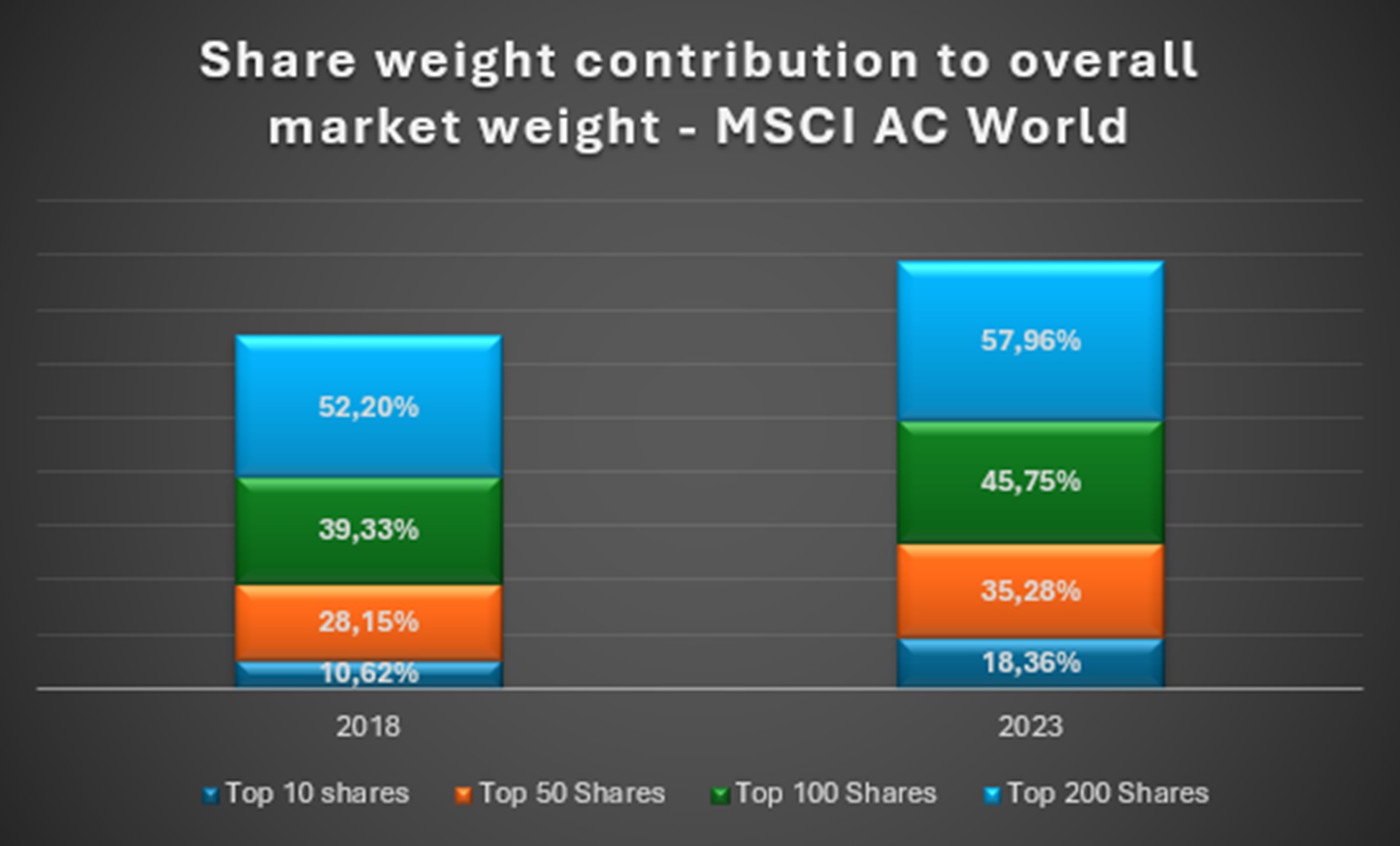

The share concentration in the global equity market has increased quite significantly, mainly due to the abnormally large difference in growth in a select few stocks versus the rest of the market.

The Top 10 shares now contribute to a larger cumulative weight in the index (10.62% in 2018 to 18.36% in 2023). This increase in concentration is mainly because of seven technology shares that have grown immensely over the past couple of years relative to the rest of the market, making it extremely difficult for active managers to outperform if they do not favour those companies from an investment perspective. Given the breadth beyond the top 10 shares, it remains difficult to pick winning stocks in an active portfolio that will consistently outperform the market.

According to SPIVA research*, only 12.58% of all large cap funds in the US have managed to outperform the S&P 500 over the past 10 years and only 21.32% over the past 5 years. This explains, in part, why passive investing makes good sense and therefore the resultant growth of passive investing on the back of this phenomena.

Whilst passive investing has also grown in South Africa, the trend has been less pronounced. Passive investing has been prevalent globally for decades and is mature, with a broad range of products and substantial assets under management (AUM) in passive funds. In South Africa, the market is still in a relatively early stage compared to its global counterparts. The range of available products is expanding, but it is not yet as comprehensive. There are a couple of possible interrelated reasons for this trend:

1. Market structure and size

The South African stock market is small and concentrated compared to major global markets. A significant portion of the market capitalisation is dominated by a few large companies (like Naspers, BHP Billiton, and Anglo American), making it challenging for passive funds to offer the same level of diversification available in developed markets.

With 10 shares contributing to 41% of the overall market capitalization, this hyper-concentration in the equity market index suggests that investors may not be willing to put all their proverbial eggs in a very small basket. An active management approach is therefore preferred to deliver better risk-adjusted return outcomes.

South Africa’s market is also characterised by less liquidity compared to more developed markets. Concentration and illiquidity often lead to the market being more volatile and less efficient, providing opportunities for active managers to exploit mispricing and generate alpha.

2. Investment culture, preferences and performance

Active management has been the dominant investment strategy for decades in South Africa. South African investors have traditionally favoured active management due to the belief that fund managers can better navigate the market’s unique characteristics and achieve higher returns. Many investors and institutions have long-standing relationships with active managers and a deep-seated trust in their expertise.

Some active managers in South Africa have established strong track records of outperforming the market, reinforcing confidence in their abilities. According to SPIVA Research**, 29.41% of South African equity funds have managed to outperform the Capped SWIX over the past 10 years, compared to 12.6% in the US over the same period. Over a 5-year window, this number increases to 51% (vs. 21.3% in the US), reinforcing the belief that active management can yield better returns and make passive investing seem less attractive.

3. Costs and fees

Although passive funds generally have lower fees, the cost structures in South Africa for setting up and managing these funds can be higher than in other regions, making passive investing relatively less attractive to both providers and investors.

At the same time there is a very strong view that passive investors will lag the benchmark performance on a net of fee basis. Active management with higher fees might still make sense as better rated and skilled active managers have shown evidence that they can outperform the market on a net of fee basis.

4. Institutional influence

Large institutional investors, including pension funds, have traditionally allocated significant portions of their portfolios to active management. Their influence and investment practices have a substantial impact on the market. Some institutional mandates and investment policies may still favor active management due to historical performance or specific investment objectives.

In conclusion, while passive investing continues to slowly grow in popularity in South Africa, traditional active management strategies continue to hold significant influence in this country due to historical precedence, our local market’s characteristics, investor preferences, relatively higher fees for passives in SA, and strong marketing and distribution networks of active managers. However, as the market evolves and investor education improves, we believe that the balance between active and passive investing should change in the way that it has globally.

*https://www.spglobal.com/spdji/en/research-insights/spiva/#us

**https://www.spglobal.com/spdji/en/research-insights/spiva/#south-africa

ENDS

Ed’s note: Passive investing was the Special Feature in the Q3 issue of Pensions World SA which you can read here.