Thando Noganta, Data Scientist at Matrix Fund Managers

In this article I explain how the shift from defined-benefit to defined-contribution pension funds is accelerating demand for higher-return assets and why the “AI trade” driven by the S&P 500’s breakaway group, the Magnificent 7, would be better represented in a dedicated sleeve, not in the core.

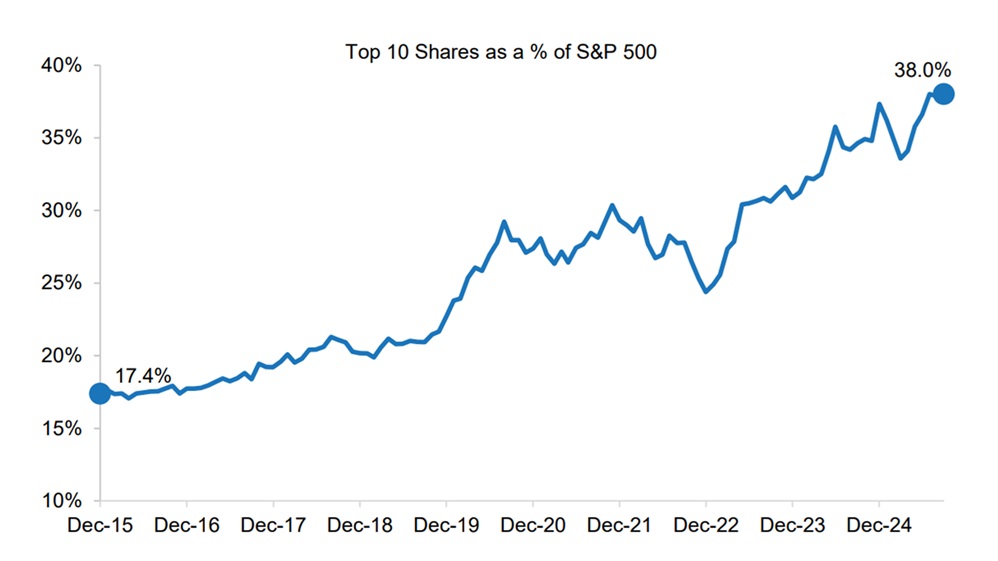

Unpacking the Mag7 There is value in understanding the performance of the S&P 500 going into this conversation. Below I show the 10-year performance of the index together with the performance of the Magnificent 7; Alphabet, Amazon, Apple, Meta, Microsoft, NVIDIA and Tesla.

Figure 1: Market Concentration of the S&P 500 in terms of Market Cap

Source: Bloomberg, S&P

With the MAG7 holding positions 1 through 5, as well as positions 7-9 (Alphabet has two classes), it is clear to see that the S&P 500 is a highly AI-concentrated index.

This concentration results in the index’s performance relying heavily on these seven shares with the MAG7 having a 10-year Compound Annual Growth Rate (CAGR) of 40% which contributes approximately 3% to the 15% CAGR of the S&P 500.

Needless to say, the performance over this period has not only led to an increase in the benchmark weights of these shares, but it has also garnered increased media coverage amid concerns about a “Tech bubble” or “AI Bust”.

AI boom or bust

At this year’s RMB Morgan Stanley Big Five Investor Conference, Minack Advisors introduced delegates to an “AI-8” basket; the Magnificent 7, but with Tesla and Apple swapped out for Oracle and Palantir and adding Broadcom. The theme: investors want a slice of generative AI’s high growth narrative which we have shown above.

The issue then becomes one of herd mentality because of this concentration with benchmarks disproportionately holding these stocks almost forcing both passive and active asset managers to replicate the same or “miss out on high returns”.

We can see what the S&P ex-Mag7 performance was over the past 10 years. An active portfolio manager that did not hold these shares would have had to account for severe underperformance. While a passive portfolio manager would have had no choice but to follow the benchmark.

Although the general theme of these Mag7 shares is the same, the corporate structures differ. Microsoft ring fences most of its AI optionality inside a partnership and minority stake in OpenAI, leaving the blue-chip, cash flow engine of Azure, Office and LinkedIn largely intact. Operational or regulatory setbacks at OpenAI hit the sidecar, not the core.

Contrast that with Alphabet, Meta or NVIDIA, whose group-wide valuations hinge directly on AI execution. Model slippage, chip shortages or unexpected rule-making feed straight into the P&L and therefore into share price volatility.

Investors grouping them altogether is also a phenomenon that Minack stresses may not be entirely accurate. Apple has not revamped its operations to tap into the Generative AI hype and neither has Tesla, hence they put forward the AI-8 vs the Magnificent 7.

The positioning of these companies as both blue-chip and new-frontier innovators is fuelling concerns about an impending AI boom or bust, whether it’s excitement over the abnormal returns from AI efficiencies or fear of the AI bubble bursting.

Why this matters for all investors, but especially pension funds

Long-horizon, liability-aware investors like pension funds prefer steady cash generation from blue-chip companies. These same investors also recognise the need for growth assets as the majority (70% in OECD countries) of pension funds transition from defined-benefit (DB) pension funds to defined-contribution (DC) pension fund structures. In a DC pension fund the upside from alternative assets becomes mission critical, the downside, fatal to the portfolio.

In the current set up, a fund classifies Meta or Alphabet as a “defensive mega-cap” because of their weight in the index which then inadvertently sneaks venture-style risk into its liability-matching sleeve.

These shares all have massive network effects that rewards the first to market – a “winner-takes-all” venture capital characteristic. We saw this in May 2025 when Apple announced its ambitions for an AI-powered search engine which resulted in Alphabet’s share price sliding 7% on the day.

The Magnificent 7 companies also share the similarity of having an internal portfolio of “start-ups” that create embedded optionality which is a classic late-stage venture capital fund characteristic. We see this with Alphabet having Waymo and Verily and NVIDIA having an inception programme with over 15,000 startups in it.

54% of Meta still belongs to Mark Zuckerberg, 13% of Tesla to Elon Musk and Jeff Bezos’s executive role means he still guides Amazon’s long-term bets. This speaks to the founder-driven mentality of these companies which keeps risk appetite high, and it closely mirrors VC fund preferences for founder control.

The problem is this: high risk high return new-frontier ventures embedded in trusted, stable, blue-chip companies are drawing interest from investors without a clear breakdown of which part of the offering they are subscribing to.

Hypothetical solution

A pension fund wanting exposure to the core company with a side of the VC should be able to do so in a clear fashion. The question in 2025 should not be “Should we own Meta?” but rather “Where should we own Meta?” in the steady-income bucket that finances near-term pensions, or in the high-risk, high-reward sleeve that targets venture-style returns?

My solution would be a dual-bucket framework separating core income vs growth. Think of it as a tale of two balance sheets where many of the Magnificent 7 cohort would separate their AI ventures into a distinct portfolio which would then be managed like the venture portfolio it is, while leaving the core operations of the blue chip, household name in a sleeve of its own.

The benefit is two-fold: it would allow the companies to ring-fence their exploratory generative AI projects without worrying about an adverse impact on the company’s overall performance (no AI boom or bust scenario); and funds would be able to allocate capital to the blue-chip company with a demonstrated history of consistent returns with the knowledge that there was limited downside (bust) in their core income sleeve. The fund would then also allocate a portion of their risk capital towards the AI venture sleeve (boom potential) in line with the growth fund allocation.

Not only would this solution help manage the “AI boom or bust” concerns in the market, but it would also facilitate better governance structures with assets that are ring-fenced on the company’s side and with clear asset allocation in terms of traditional and alternative investments on the investor’s side.

So, where should we own Microsoft in 2025? In the steady-income bucket or in the high-octane sleeve?

Answer: Both, but with a clear demarcation!

ENDS

This article was first published in Glacier by Sanlam’s Funds on Friday issue of 10 October 2025.