Leanne van Wyk, Head of Legal at Ensimini Administration Services (Pty) Ltd

If a member has taken a savings withdrawal benefit and in the same tax year is now leaving the fund, what may the member take from their savings pot?

Well, it is all a bit confuddling, the iterative legislative changes made over the years have left us all drawing pictures with crayons to make sure we have it right now. I speak for myself…

The changes over time

The rules now

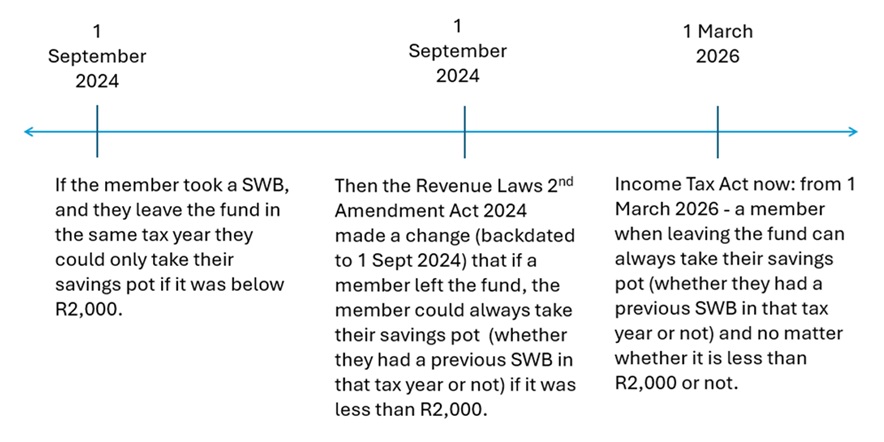

With effect from 1 March 2026, a member whose membership of a fund terminates may withdraw the total balance in their savings pot, regardless of the amount and regardless of whether they have already made a savings withdrawal benefit (SWB) from that fund during the same year of assessment.

The general rule remains that a SWB may not be less than R2,000 (before charges and transaction costs). However, where a member exits the fund, this minimum threshold falls away entirely. The member is entitled to take whatever amount stands to their credit in the savings pot, even if it is below R2,000, and even if they have already made a withdrawal from the savings pot during that tax year.

Termination of membership is required

A member may leave employment but may retain money in the fund, which means they have not left membership. The second bite at the savings pot in the same tax year applies not on termination of employment but on termination of membership of the fund. You actually have to leave the fund (not have any funds left in it) to gain access to the savings pot again in the same tax year.

Treasury received comment requesting termination of “membership” to be changed to termination of “employment”, but this change was not included in the final version.

So you can’t have a second bite at your savings pot if you leave money in the fund and remain a member, your membership has to terminate: for example, you take your savings pot and vested pot in cash and transfer your retirement pot off the fund. You can’t take a second bite at your savings pot in the same tax year if you, for example, want to preserve your retirement pot in the fund and become a paid up member[1] because your membership has not terminated.

This applies equally to paid-up members of a fund whose membership terminates.

Example 1

Priya is a member of the ABC Pension Fund. In August 2026 she made a savings withdrawal benefit of R5,000 from her savings pot. She then resigned from her employer in January 2027 and exercises her options such that her membership of the fund is terminated. At the point of exit, her savings pot balance is R1,400.

Because Priya is terminating her membership of the fund, she is entitled to withdraw the full R1,400 savings pot balance. The fact that she already made a withdrawal earlier in the same tax year does not prevent this. And the fact that R1,400 is below the general R2,000 minimum does not prevent it either. She may take the full balance in the savings pot.

Example 2

I hope that this new rule does not lead to members who are in need of cash in the tax year leaving employment to get a second bite at their savings pots.

Thabo has R20,000 in his savings pot. On 1 April 2026 he makes a savings withdrawal benefit of R2,000, leaving a balance of R18,000 in his savings pot.

On 1 May 2026, Thabo needs additional funds urgently and cannot wait until the next tax year. He resigns from his employer. He applies to withdraw the remaining R18,000 from his savings pot and exercises his options such that his membership of the fund is terminated.

Because Thabo is terminating his membership of the fund, he is entitled to withdraw the full R18,000 balance. The fact that he already made a savings withdrawal benefit of R2,000 earlier in the same tax year does not prevent him from withdrawing his remaining savings pot balance on exit from the fund. He receives the full R18,000.

Communication to members

Many administrators are going to need to make system changes for this amendment. The two pot rules on withdrawal from a fund are already difficult to explain. This change to the law has added some extra nuances. It will need to be explained to members…

More changes down the line

Treasury is likely to consult on whether and what access retrenched members should have to their retirement pots. We will keep you posted.

[1] See my Pension World article Q1 of 2025 for an explanation of the complicated options on withdrawal rules here

ENDS