Darpan Harar and Justin Jewell, Co-Heads of Multi Asset Credit at Ninety One

Darpan Harar and Justin Jewell, Co-Heads of Multi Asset Credit at Ninety One, explain that while risks that built up post the Global Financial Crisis are beginning to surface in US private markets, credit quality has improved in the mainstream high-yield market. With recent market moves masking a divergent picture of risk exposure across mainstream credit markets, investors can capitalise on the sell-off and position themselves defensively.

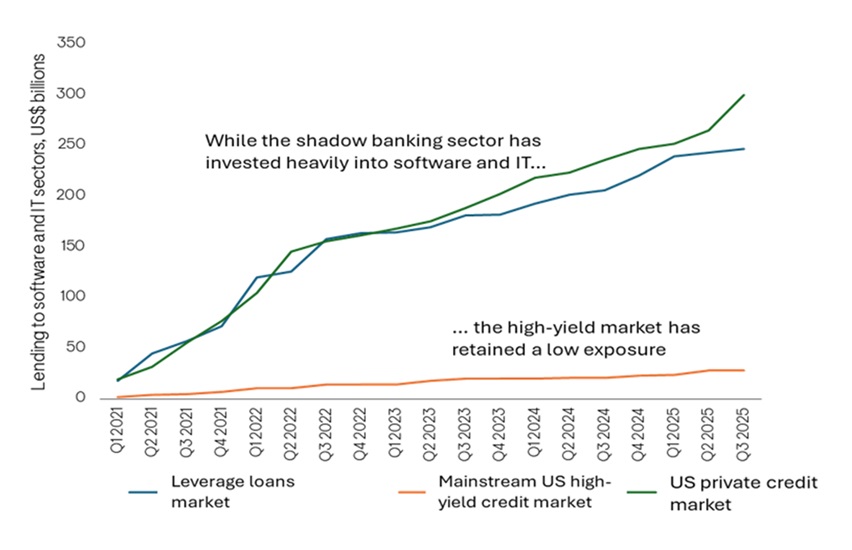

The chart

The lion’s share of lending to sectors most vulnerable to AI disruption risk has taken place outside of mainstream public credit markets.

Source: Ninety One analysis using data from Preqin for the private credit market, S&P for the loans market, and ICE index data for the high-yield market.

The context

Over recent months, one headline after another has shone a spotlight on risk in the US private credit market. Issues that have been building for years, relating to the financing of high-risk borrowers and a weakening of credit standards, are coming to a head, driving up scrutiny of the private credit market and sparking a sell-off in mainstream public credit markets, such as US high-yield debt.

For context: the US private credit industry expanded after the Global Financial Crisis in 2008. As banks scaled back their lending to riskier borrowers, private-market firms stepped in to fill the gap – fuelling the growth of the ‘shadow banking’ sector.

Jewell: “Many loans made in this period are now under pressure from higher interest rates and AI disruption risk – especially since private lenders invested heavily in the software and IT sectors – areas considered most vulnerable to disruption.”

However, as outlined here, recent market moves mask a more nuanced backdrop. With private markets and leveraged loans now dominating the riskier end of lending activity, credit risk in the mainstream high-yield market has remained remarkably stable. In fact, the average credit quality of the high-yield index is the highest it has been in several decades.

Harar: “While some segments of the public market have indirect exposure to this theme – notably parts of the insurance and banking sectors, and select business development company (BDC) bonds – we believe many of these structures will prove resilient, supported by strong capitalisation and conservative leverage metrics. As always, selectivity remains key.”

The conclusion

The credit landscape is shifting as risks that built up post the Global Financial Crisis begin to surface, particularly in US private markets. In tandem, there’s been a quiet revolution in the high-yield credit market – where overall credit quality has improved.

Jewell: “Recent market moves miss this nuance and mask a divergent picture of risk exposure across mainstream credit markets.”

Harar concludes: “By avoiding the most vulnerable sectors and targeting well-structured, higher-quality assets, bottom-up investors can navigate the risks while taking advantage of attractive valuations to capture return opportunities.”

ENDS