Maarten Ackerman, Chief Economist at Citadel

South Africa’s (SA’s) economy delivered a slightly stronger-than-expected performance in the first quarter of 2026, with gross domestic product (GDP) expanding by 0.5% quarter-on-quarter and annual growth moving close to 2%. While the result offers some encouragement in a difficult economic environment, Citadel Chief Economist, Maarten Ackerman, cautions that the data reflects conditions before the latest global and domestic headwinds began to intensify.

“SA’s first-quarter GDP number came in slightly ahead of expectations and confirms that the economy still has the underlying capacity to generate growth,” says Ackerman. “However, it is important to recognise that this is largely a pre-geopolitical conflict number, supported by the continuation of favourable tailwinds from 2025, including strong commodity prices and another solid contribution from agriculture,” he adds.

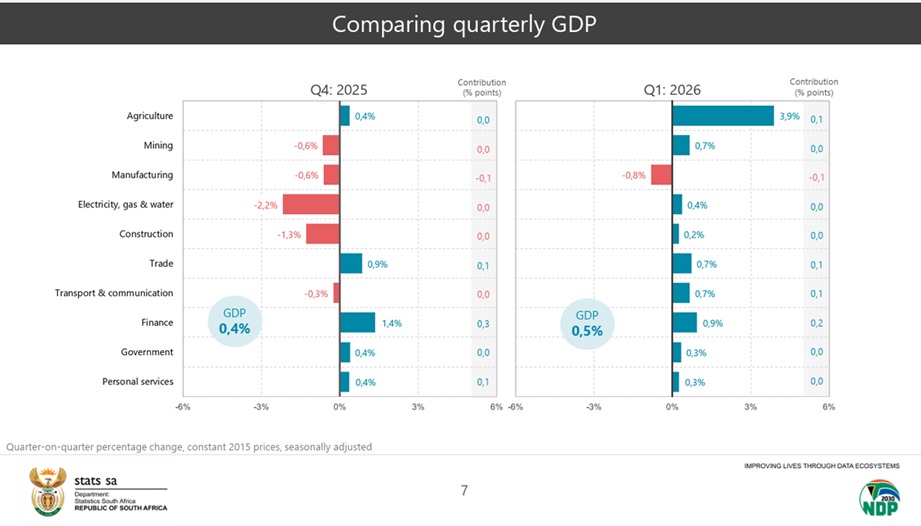

Figure 1: Source: Stats SA GDP figures for Q1 2026

Sector performance encouragingly broad-based

“Agriculture was the standout performer in the quarter, expanding by 3.9%, while the finance sector remained one of the economy’s most consistent contributors. Encouragingly, growth was relatively broad-based, with all sectors except manufacturing contributing positively,” he highlights.

“A broader-based growth profile is a positive signal, because it suggests that the recovery is not being driven by one sector alone; the fact that most sectors contributed positively gives us a better foundation than a narrowly concentrated growth outcome would have done,” he explains.

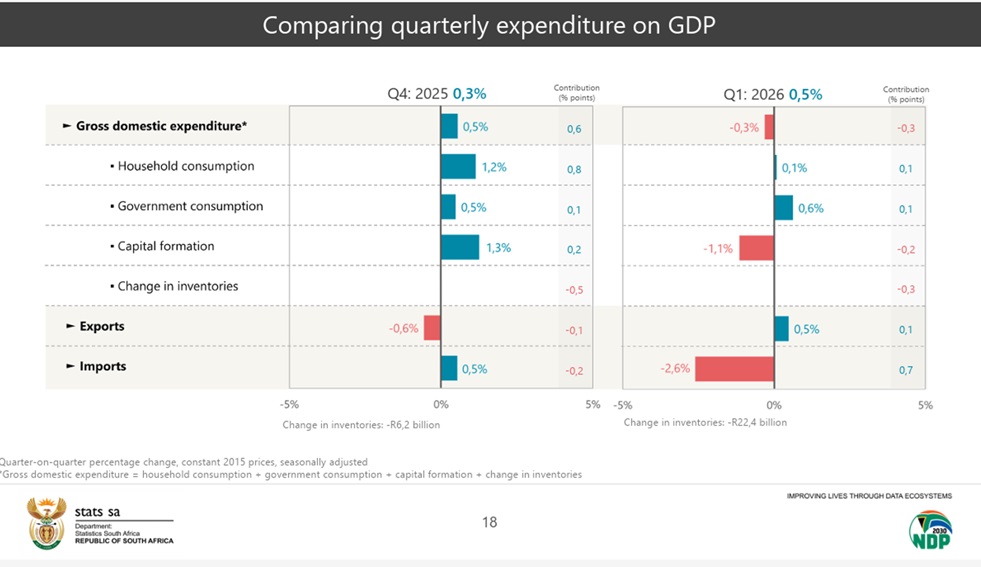

Figure 2: Source: Stats SA GDP figures for Q1 2026

Consumer weakness raises concern

“However, beneath the positive headline number, there are signs of fragility. Household consumption, a key driver of SA’s consumer-led economy, slowed sharply to just 0.1% in the quarter, down from 1.2% in the previous quarter,” notes Ackerman.

“The sharp slowdown in household consumption is concerning; consumers were already under pressure before the latest geopolitical and inflationary risks emerged, which suggests that households may find the coming quarters increasingly difficult,” he cautions.

Figure 3: Source: Stats SA GDP figures for Q1 2026

Structural weakness in investments

“Investment also remains a structural weakness. Gross fixed capital formation declined again in the quarter, extending a persistent multi-year trend. Over the past three years, only two quarters have recorded positive investment growth,” observes Ackerman.

This remains one of the clearest constraints on SA’s long-term growth potential; without stronger private sector investment and sustained capital formation, it becomes very difficult for the economy to shift onto a structurally higher growth path,” he highlights.

Outlook: Headwinds likely to intensify

“The outlook for the remainder of 2026 is expected to be more challenging. Since the end of the first quarter, rising geopolitical tensions in the Middle East have pushed energy costs higher, inflationary pressures have intensified and tighter monetary policy is likely to keep interest rates elevated for longer. This places further pressure on consumers and businesses,” says Ackerman.

“Domestically, agriculture, one of the key drivers of recent growth, is also likely to come under pressure in the coming quarters as disease outbreaks, adverse weather conditions, flood-related infrastructure damage and higher input costs, particularly fuel and fertiliser, weigh on output,” he notes.

“While the Q1 data gives us a better starting point, the growth outlook has become more difficult; the combination of higher energy costs, sticky inflation, elevated interest rates and pressure on agriculture means that economic momentum is likely to slow as the year progresses,” Ackerman explains.

Growth expected to slow below 1% in 2026

“Taking these headwinds into account, Citadel expects SA’s GDP growth to slow to below 1% for the full year in 2026,” says Ackerman.

“The Q1 number tells us that SA still has pockets of resilience, but it does not remove the structural challenges facing the economy; the real test will be whether the country can sustain growth in an environment of tighter financial conditions, weaker consumer momentum and renewed global uncertainty,” he points out.

Investment implications

For investors, Ackerman says the GDP result should be interpreted with discipline and context.

“Investors should avoid assuming a direct link between GDP growth and market returns; markets are forward-looking and often respond to changing interest rate expectations, currency movements and global risk appetite as much as they do to local economic growth,” he says.

He adds that the current environment reinforces the importance of diversification.

“In an uncertain environment, investors should remain well-diversified across asset classes and geographies; fixed income markets may offer improved opportunities as the monetary policy cycle shifts, while currency markets can present tactical opportunities during periods of heightened volatility. Offshore diversification also remains important, as it provides exposure to broader global growth drivers,” Ackerman concludes.

ENDS