Paul Nixon, Head of Behavioural Finance at Momentum Investments

The United States ‘on-again, off-again relationship with global tariffs has created tremendous volatility in markets. If there is one thing people and markets don’t like, it’s uncertainty, and there is plenty of that to go around. Investors and their advisers, therefore, need to strap in for some sustained turbulence.

History shows that the returns of the S&P 500 after big crises – like the Great Depression of 1929, the Dotcom bubble of 2001 and the Global Financial Crisis (GFC) of 2008) – was between 20% (Dotcom bubble) and 60% (Great Depression) lower over the following year, with GFC in-between at a drawdown of 45%. For minor crises – the debt ceiling crisis of 2011, the China slowdown of 2015 and the COVID-19 pandemic in 2020 – the S&P 500 provided fantastic returns in the following 12 months, ranging from 15% in 2011 to 50% in 2020 following the COVID pandemic, with a 12% uptick after the China slowdown of 2015.

What type of crisis are we in now?

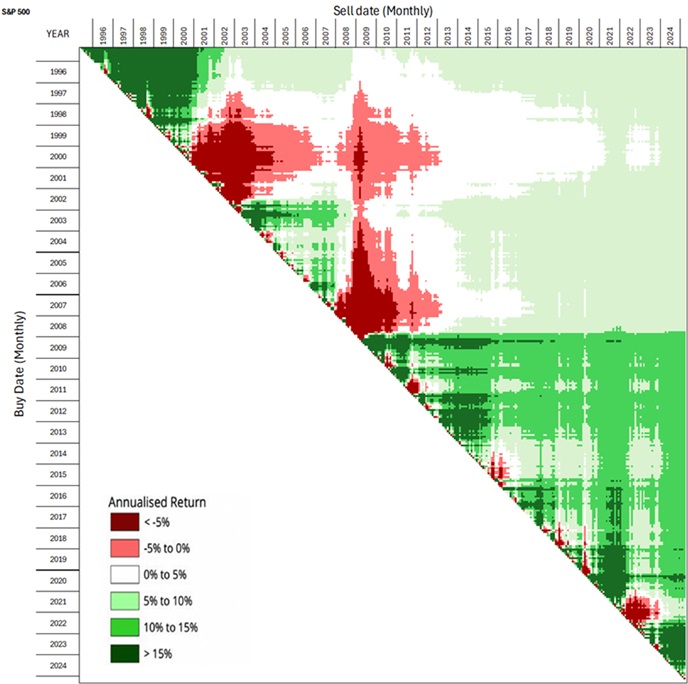

Therefore, the million-dollar question is: Are we in a big crisis or a small one? The truth is nobody knows. Few predicted that markets would shrug off and rebound as quickly as they did after the COVID-19 crash. When we zoom out, though, we may find that this matters less than anticipated. The chart on the next page shows all these events: from the end of 1996 to the end of March 2025, all possible monthly buy dates (diagonal line) and sell dates (horizontal line) for the S&P 500. Areas of light and deep red indicate negative returns, and areas of light and deep green indicate good returns. White areas represent returns of between 0% and 5%.

Here are the three key takeaways from this chart:

1. Proportionately, there is far more green than red. In fact, over the past 100 years, bull markets in the US have yielded an average cumulative return of nearly 150%, while bear markets, on average, have only yielded a 31% loss. So, the financial physics of being rewarded for taking risks generally holds. However, taking more risk does not equal higher returns – taking more risk only provides the opportunity for reward. There is no such opportunity without risk. Volatility is a feature of risky asset classes because it works in both directions.

2. The red zones are not realised losses. They are paper losses represented by the fall in index value. A real loss – or behaviour tax – is incurred by selling existing holdings (usually bought in a green zone) and selling them in a red zone.

3. Investing in the ‘market’ or having a diversified portfolio gives the investor the upper hand in a transitory shift. To illustrate this, look at the composition of the S&P 500 before and after COVID-19, with the rise of the Magnificent Seven, which now dominates the index.

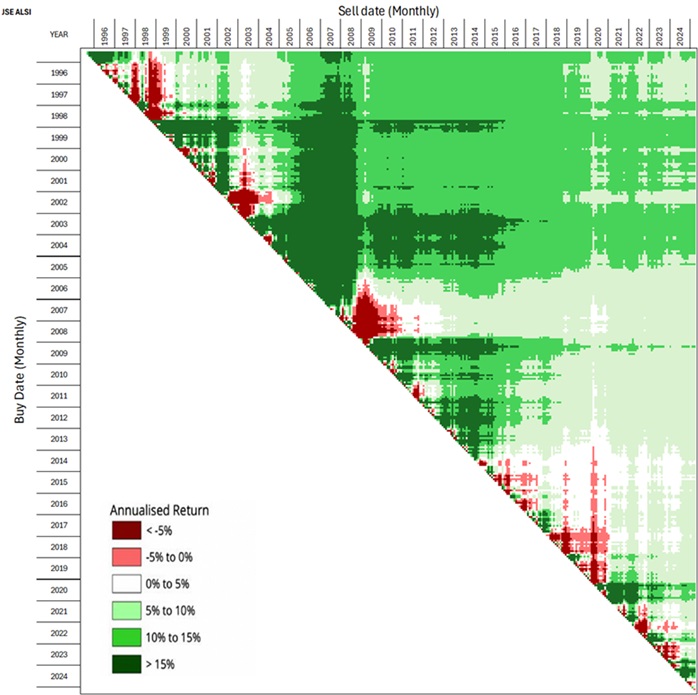

Now let’s look at the returns provided by the JSE All Share Index (ALSI) in the same format over the same period. While the same three points are clear, here it is worthwhile emphasising the third point. The image below shows how important global diversification is. Considering the dollar value of an investor’s portfolio and the digital and AI revolution post-COVID-19, local investors would have benefitted from this diversification substantially, as local economic growth has dwindled over the past decade.

The market turbulence trap, however, is always a great time to show your value as a financial adviser. But avoiding the market turbulence trap remains difficult. The average behaviour tax – the value lost from switching between different funds – remains at an annualised value of around 3% since the onset of the COVID-19 pandemic in 2020. This means, on average, investors are destroying wealth when measured against those that buy-and-hold.

Markets are likely to be volatile for some time, at least until the current policies of the United States administration or their effects have been stabilised. This is a good time to keep in close contact with clients who need the most help avoiding the market turbulence trap of becoming short-term-focused instead of keeping focused on their long-term investment goals with a well-diversified portfolio.

ENDS