Prof Haroon Bhorat, Chair: Investment Committee at Sygnia

One of the most important relationships in economics, almost intrinsically understood, is that taxes are both necessary for an economy but may also act as a disincentive to economic activity. That governments require revenue to provide public goods and services (hopefully at a high quality and with minimal corruption!) to its citizenry is widely accepted. However, the art of taxation is to avoid generating such high levels of taxation – corporate or individual – that they undermine economic growth and development. If taxes are set too high, individuals will stop working, emigrate or switch to less productive work. Companies may switch jurisdictions, choose to invest less in growth and so on.

One way to think about this impact of higher taxes is through the Laffer curve, a theoretical relationship in search of empirical evidence. It suggests an inverse U-shape relationship between taxation rates and government revenue: tax rates can be increased and will raise revenue, but continue and the disincentive effects kick in and government revenue may actually decline! If ever an example was required of why Economics is often called the “dismal science” – this is it!

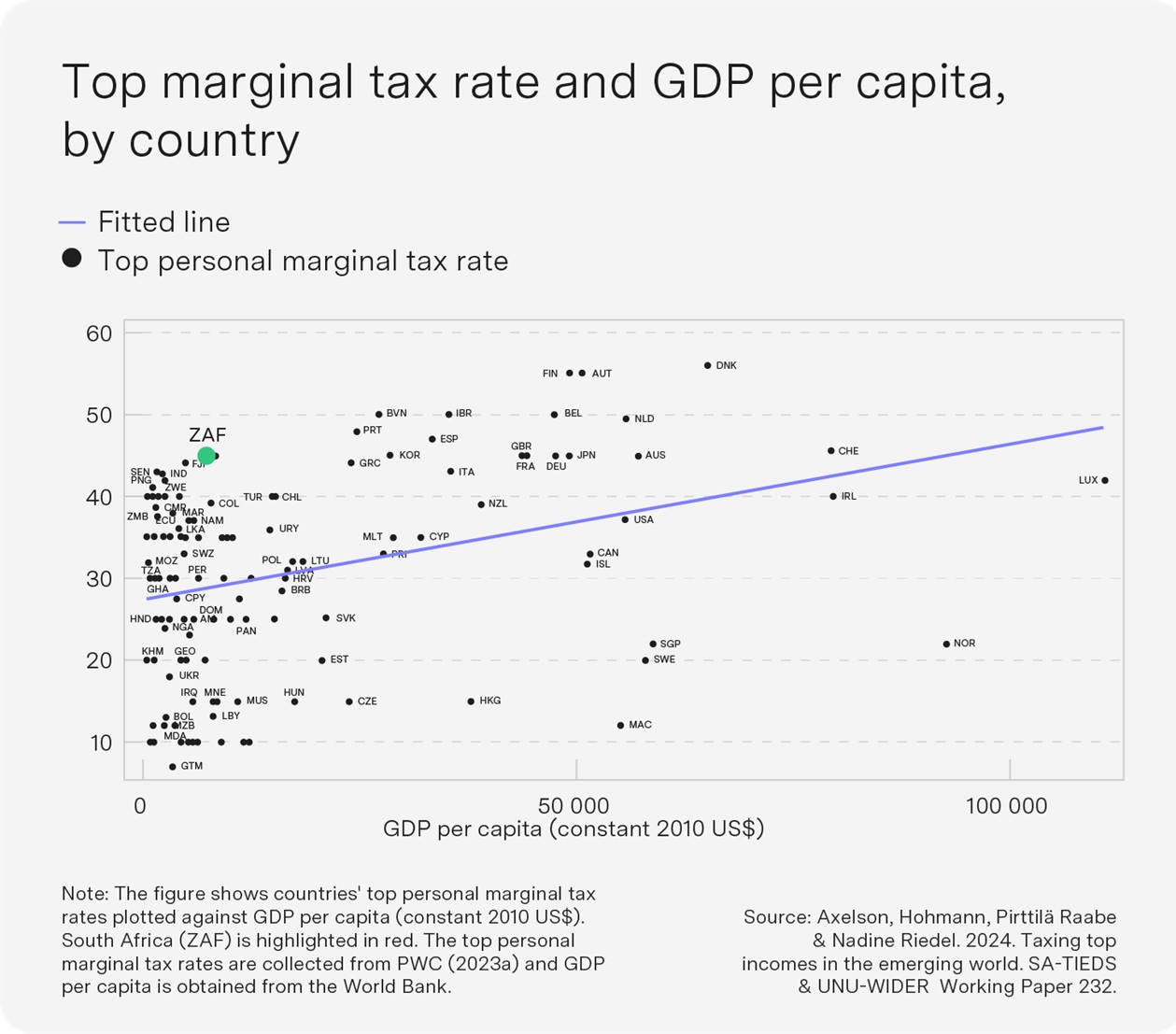

Recent research from National Treasury and the University of Helsinki explored the impact of an increase in the top marginal tax rate on South African personal income in 2017 from 41% to 45%. As the graphic below indicates, South Africa’s economy already has one of the highest top marginal personal income tax (PIT) rates in the world at its level of GDP per capita. PIT in South Africa is crucial for revenue generation, accounting for close to 40% of total tax revenue in the country. The researchers explored whether this specific increase in the marginal tax rate might have undermined its intention to increase government revenue.

The core finding is that the tax hike did not achieve its primary aim of raising revenue. Specifically, the data show that while the projection was for tax revenue to increase from R103bn to R109bn, revenue to SARS actually declined to R97bn – the 2017 tax hike reduced revenue from this income bracket (which represented 0.6% of all income earners in South Africa for that tax year). We effectively moved onto the wrong side of the Laffer curve as individuals worked less, switched jurisdictions and/or evaded taxes to avoid paying at the new top marginal rate. On this evidence, the tax hike was a policy failure.

One positive outcome, though not necessarily a focus of the tax policy, was that the Gini coefficient measuring wage inequality declined marginally. However, the research found that revenues declined first and foremost because reported taxable income declined! The evidence suggests that individuals essentially diverted previous taxable income to other forms of income and benefits that are at lower rates – a classic tax evasion response feeding into a Laffer curve “turning point”. Another very real possibility is that incomes fell because individuals worked less to avoid paying the new, higher taxes. This is terminal to a country like South Africa, which is in desperate need of high-productivity individuals with the scarce skills implicit in taxpayers in this bracket.

But perhaps the most damning finding is that companies linked to these high-income earners showed a significant drop in output after the tax change. In simple terms, companies faced with this sharp hike in taxes contracted – so the tax increase only served to constrain the growth of the affected South African companies. More than any other, this result suggests that the tax authorities should seriously reconsider the PIT adjustment, which appears to have done more harm than good to the South African economy.

ENDS