Leon Michaelides, Portfolio Manager at Matrix Fund Managers

With gold trading near record highs – for all the macroeconomic, geopolitical, and monetary reasons we explored in earlier articles (see here) – investors are asking how best to gain exposure to the metal’s price appreciation. In this note, we examine some options available to South African investors and outline which approach makes the most sense.

Buy the physical metal – bullion bars, gold coins and jewellery

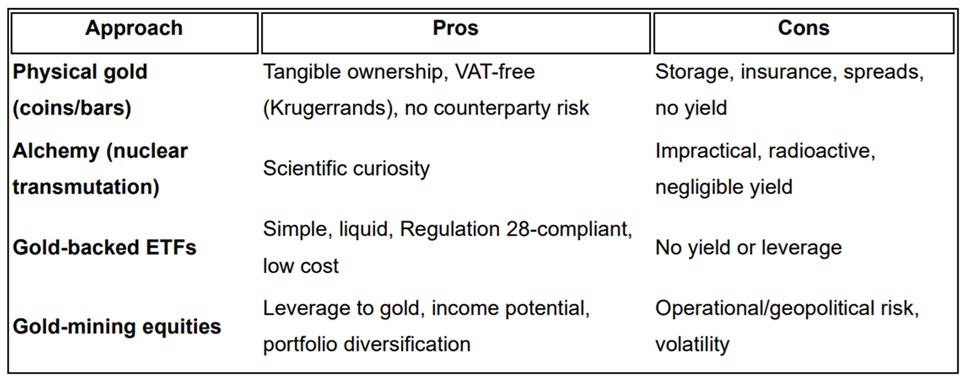

Owning physical gold offers direct, tangible exposure to the metal with no counterparty risk. There’s also an undeniable psychological appeal to holding a heavy, gleaming coin or bar. However, this route comes with significant storage, security, and insurance costs. Of these, Krugerrands remain the most practical physical option. They trade at modest premiums to the spot gold price and are highly liquid in the local market.

In South Africa, the Precious Metals Act (2005) ended the prohibition on private ownership of unwrought gold, however the downside is that gold bars are subject to VAT on purchase, unlike Krugerrand coins that are VAT exempt. You can also expect to pay a premium over spot that varies by bar size, with smaller bars carrying higher percentage premiums.

Historical gold coins – such as the 1 Pond coins minted between 1892 and 1900, featuring President Paul Kruger – can still be found at reputable dealers and usually trade close to melt value. Certain rare variants, including the Double Shaft 1 Pond, Veld Pond, Kaal Ponde, and the Sammy Marks Tickey, have collectible premiums that can reach as high as R1.5 million per coin, equivalent to roughly US $366,000 per ounce.

Gold jewellery is a far less efficient vehicle for investment. Buyers typically pay 50%-300% above melt value, depending on karat, brand, and retailer. Upon resale, emotional attachment aside, sellers often recover only 60%-85% of melt value from jewellers or pawn brokers.

Finally, physical gold provides no yield or cash flow – its value lies purely in price appreciation (and, for collectables, sentimental or aesthetic appeal).

Conclusion: Despite its allure, physical gold ownership is often impractical beyond small allocations for novelty or heritage purposes.

Use alchemy to create gold

While the ancient dream of turning base metals into gold has captivated minds for centuries, modern science shows that this is indeed possible through nuclear reactions, not chemistry. To convert mercury (element 80) into gold (element 79) requires altering the nucleus – changing one proton into a neutron or vice versa – through bombardment by high-energy particles such as neutrons or deuterons.

These nuclear reactions can create atoms of gold. However, yields are vanishingly small, and the resulting isotopes are often radioactive.

At the European Council for Nuclear Research’s (known as CERN’s) Large Hadron Collider (LHC), during Run 2 (2015–2018), physicists indeed produced gold by colliding lead ions. The total yield was roughly 86 billion gold nuclei, equivalent to 29 picograms (a picogram is one-trillionth of a gram). The “gold” nuclei existed for only a fleeting moment before colliding with accelerator components and fragmenting into other particles. Run 3 roughly doubled the production rate, but that was still microscopic.

Conclusion: Transmutation is scientifically fascinating but economically absurd. It’s also dangerous and produces negligible amounts of unstable gold.

Buy physical-gold-backed ETFs

Exchange Traded Funds (ETFs) provide a cost-effective way to gain exposure to the gold price without the complications of storage or security.

The most established local vehicle, the NewGold ETF (JSE:GLD), is a physically backed, debenture structured ETF; each security references 1/100th oz in custody with ICBC Standard Bank. The 0.30% pa fee is reflected via a gradual decline in metal entitlement.

For institutional investors, this route is especially convenient because while Regulation 28 of the Pension Funds Act permits direct holdings of physical gold in the form of Krugerrands, this has its practical constraints, while investment in regulated ETFs is permitted and achieves the same exposure. The products are listed, liquid, and easily integrated into multi-asset portfolios.

Conclusion: Physically backed gold ETFs offer simple, efficient exposure to the rand gold price. The trade-off is that, like physical bullion, they pay no income and provide no leverage to a rising gold price.

Invest in gold mining equities

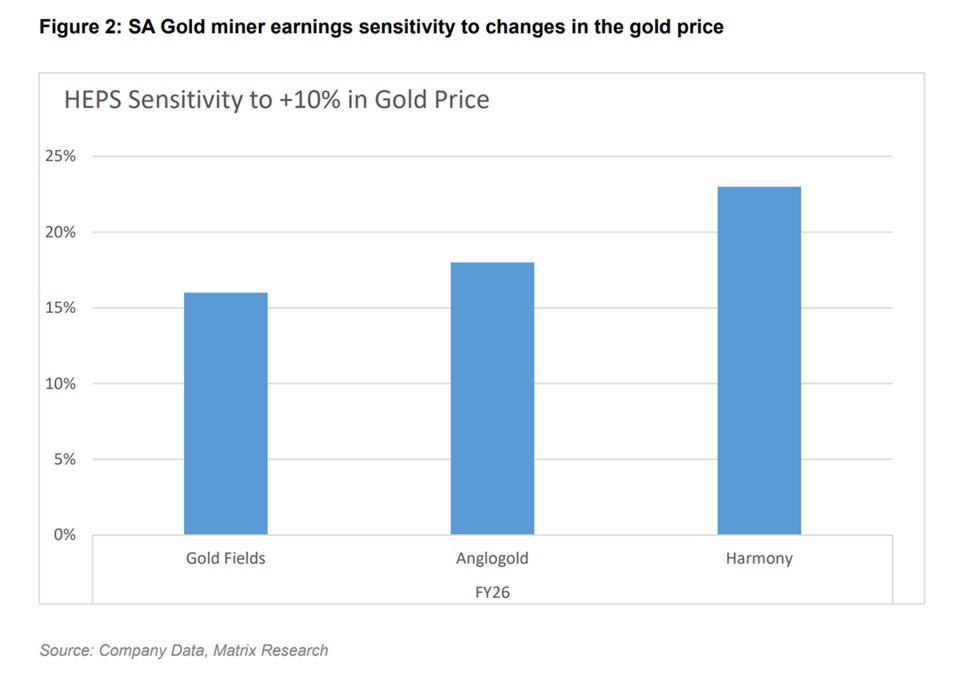

Investing in shares of gold mining companies affords investors leveraged exposure to the gold price. Mining companies typically have large, fixed costs including capital, energy, and labour. When the gold price rises, revenue increases immediately but costs rise more slowly, so profits expand disproportionately. Figure 2 illustrates the current sensitivity of gold miner earnings to changes in the gold price. This means miners are likely to outperform physical gold during bull markets. In the current cycle, gold mining stocks have already outperformed the metal.

Importantly, gold miners can return cash to shareholders through dividends or share buybacks – an income component missing from physical gold or ETFs. Currently, Gold Fields, AngloGold Ashanti, and Harmony Gold are trading on forward dividend yields of approximately 3.9%, 4.4%, and 2.3%, respectively.

Gold miners are publicly listed equities, traded on major exchanges. This allows institutional investors to include them within existing equity mandates. In South Africa, they can also be held in retirement portfolios under Regulation 28, unlike physical bullion (with the exception of Krugerrands), which fall within the 10% commodities allocation. Liquidity for large-cap miners is typically high, with shares trading daily with tight bid offer spreads.

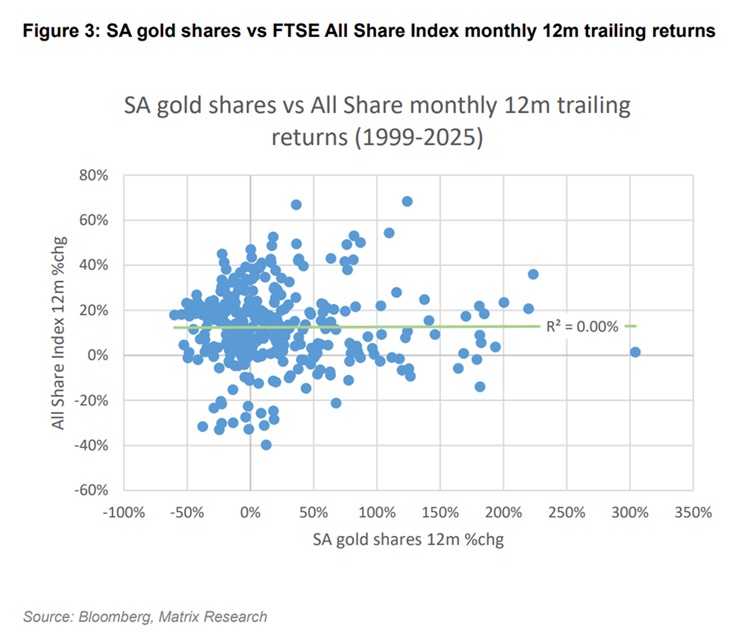

Gold-mining shares also provide diversification benefits to an investment portfolio, as gold stocks have a low correlation to other equities as well as the broader equity and bond market. Figure 3 below shows that gold shares have a very low correlation to the FTSE All Share Index.

Unlike bullion, miners can discover new reserves, expand production capacity or reduce costs via new technology or efficiency gains. This gives mining equities an embedded optionality beyond the metal’s price.

There are, however, risks inherent in gold mining and key risks for the companies include:

- Operational volatility: energy costs, labour disputes, and mine-specific issues such as flooding or accidents.

- Political and regulatory risk: changes in taxation, mining codes, or resource nationalism (notably in Tanzania, Mali, Papua New Guinea).

- Environmental and ESG scrutiny: emissions, cyanide handling, tailings-dam safety, and community relations.

- Reserve depletion: mines are wasting assets; replacement requires continual exploration and capital expenditure.

- Capital-discipline risk: historically, many miners over-invested during booms, destroying shareholder value.

- Dividend instability: payouts fluctuate with gold price volatility and can be suspended in downturns.

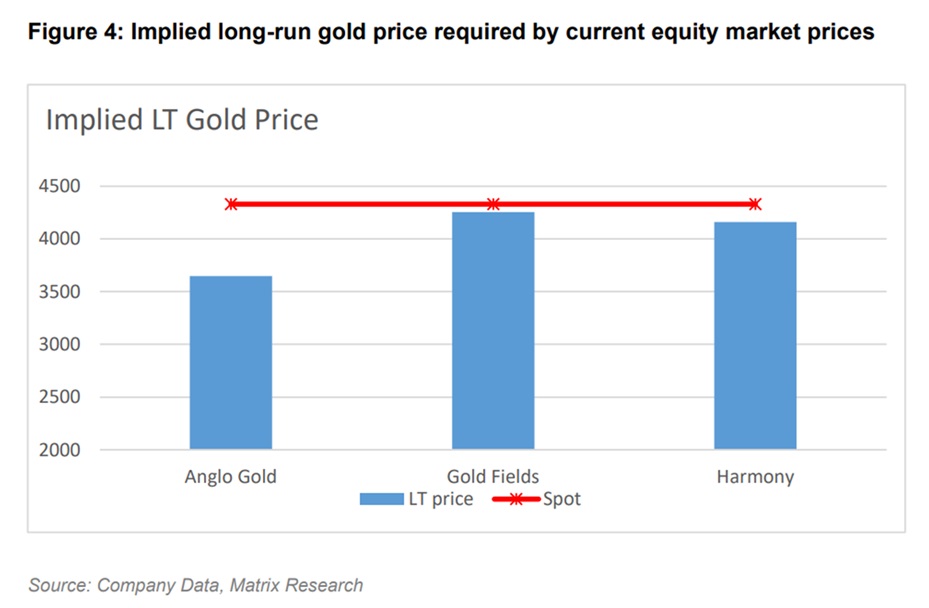

At Matrix Fund Managers, our investment process currently favours select gold equities. Strong earnings momentum and valuation support allows us to focus less on spot forecasts of future gold prices. Using our proprietary valuation framework, we assess the implied long-term gold price that each company’s share price discounts.

Figure 4 shows that AngloGold Ashanti, Gold Fields and Harmony are all pricing in long-run gold prices lower than current spot prices.

Conclusion: While gold-mining equities carry operational and market risks, they can deliver meaningful total returns – combining capital appreciation with dividends – if selected through a disciplined, fundamental process that correctly prices those risks.

Final thoughts

Investors have multiple routes to benefit from rising gold prices:

Each investment option plays a different role: physical gold preserves wealth; ETFs provide liquid price exposure; miners offer leveraged growth and yield.

In our view, equities are where the real glitter lies, provided investors apply rigorous valuation discipline and understand the risks. In today’s environment, well selected gold miners combine exposure to the metal’s momentum with the potential for superior, total returns over time.

ENDS