Rabotho Mathekga, Senior Manager Research Analyst at Novare

South Africa’s asset management industry has long been one of the quiet pillars of the financial system. It carries the retirement aspirations of millions, manages retail and institutional capital across pension funds and endowments, and plays a critical role in capital allocation within the economy. But beneath the surface, something structural is shifting.

The recent wave of mergers and acquisitions across the sector is not merely a cycle of opportunistic deal-making. It is a response perhaps even a defensive one to a shrinking financial market.

A shrinking pie

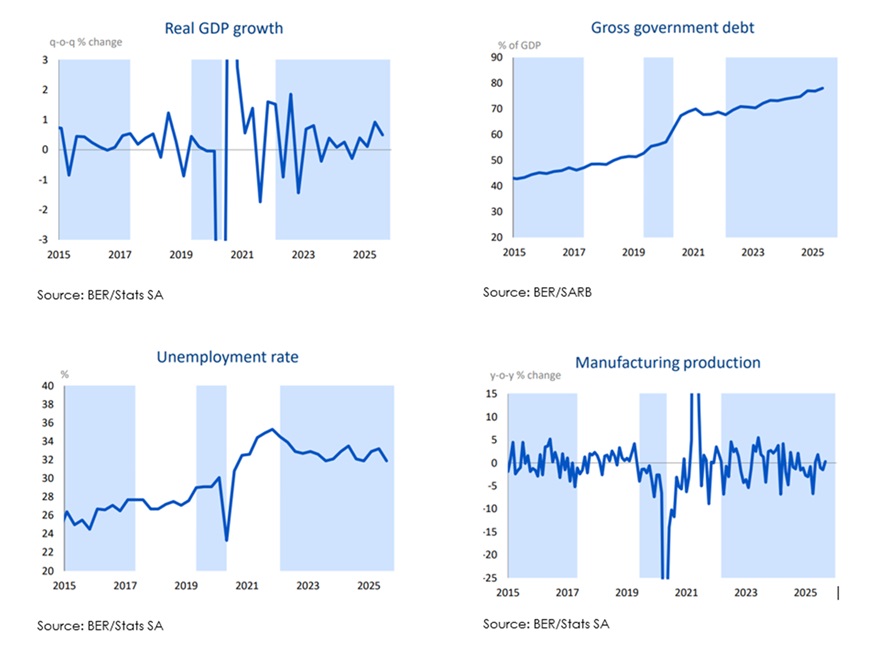

The macroeconomic backdrop is well known; low GDP growth (below 2%), rising debt-to-GDP levels (c.76%), persistent unemployment (c.31%), infrastructure bottlenecks, and declining levels of entrepreneurship. According to a September 2025 research note by the Bureau for Economic Research (BER) titled “Accounting for South Africa’s Remarkable Growth Deterioration”, South Africa experienced a pronounced and sustained decline in economic growth between 2005 and 2025. The report further highlights a contraction in productivity alongside stagnation in investment, underscoring structural weaknesses that have constrained the country’s long-term growth trajectory. Refer to the below graphs:

For asset managers, these realities translate into something more immediate: slower growth in assets under management (AUM).

Fewer jobs mean fewer pension contributions. Weak disposable income suppresses household savings. Limited business formation constrains institutional capital growth. The result is a tighter pool of investable capital.

In a low-growth environment, market share becomes a zero-sum game. Asset managers can no longer rely on organic asset expansion they must compete for slices of a declining pie.

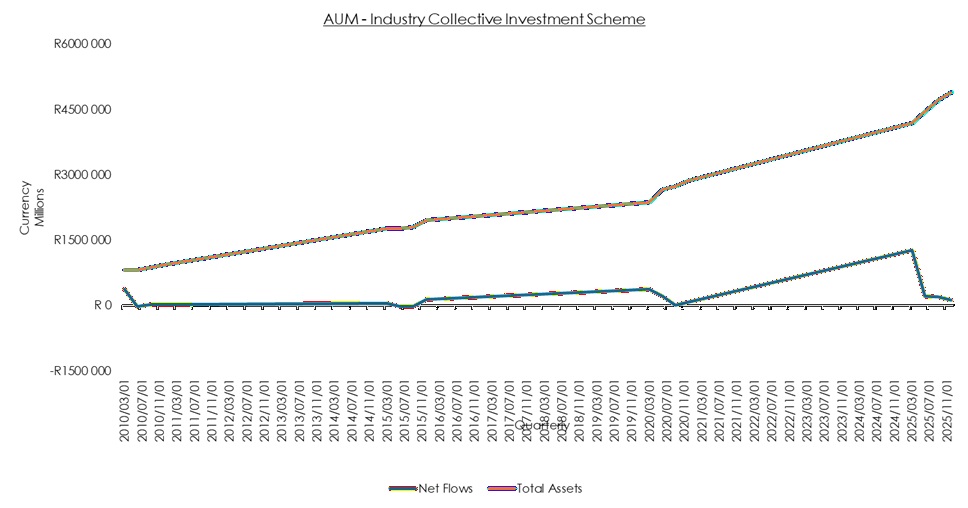

Below illustrates Industry Collective Investment Scheme (CIS) AUM – Local Fund Statistics.

Source: ASISA Statistics

According to ASISA’s CIS local fund statistics, the total assets reflect the combined effect of existing assets, new investments, and market performance. In contrast, net flows exclude market performance and capture only investor-driven capital movements, thereby serving as a cleaner proxy for assessing organic industry growth.

While total assets may suggest expansion, net flow data does not exhibit a sustained upward trajectory. Instead, it reflects extended periods characterised by stagnant to declining flows and limited growth in new investments. This pattern points to structural stagnation rather than meaningful organic expansion.

According to ASISA’s 14 August 2025 report titled “Local CIS Industry Celebrates R4 Trillion in Assets Under Management”, the Collective Investment Schemes (CIS) industry recorded total net inflows of R146.13 billion for the 12 months ending June 2025. However, the majority of these inflows were attributable to reinvested income (dividends and interest) rather than new capital. Of the total inflows, only R23 billion represented new investments, with R18 billions of this amount received in the first half of 2025 (R12 billion in Q1 and R6 billion in Q2).

Subsequently, ASISA’s 25 November 2025 statistics release indicated that, for the quarter ended September 2025, a larger proportion of net inflows consisted of new investments rather than reinvested income — the first occurrence since 2020. Of the R65 billion in net inflows recorded in the third quarter of 2025, R27 billion was attributable to new investments. Nonetheless, reinvestments continued to constitute the majority of overall net flows after 2020 till 2025.

The data suggests that new capital remains challenging, with industry growth largely supported by reinvested income rather than sustained inflows from new investors. This reinforces the view that organic expansion within the industry remains constrained.

The turn to scale

Over the past few years, consolidation has accelerated. Transactions involving firms such as Taquanta Asset Managers, Ngwedi Asset Managers, Absa Asset Management, Sanlam Investments, Ninety-One, 10X Investments, CoreShares, Old Mutual Investment Group, Vunani Fund Managers and Sentio Capital etc. – reflect a broader strategic pivot. According to the DEInvest Annual Survey (2025), corporate activity among asset managers has increased materially, rising from 4% of firms in the 2024 survey to 17% in 2025. This sharp uptick reflects a consolidation trend within the industry.

Some of the rationales would include:

- Achieve economies of scale

- Spread fixed regulatory and technology costs

- Strengthen distribution networks

- Improve pricing competitiveness

- Protect or expand market share

In a compressed-fee environment, scale matters more than ever. Regulatory compliance, technology platforms, ESG reporting requirements, and distribution costs are largely fixed. Larger balance sheets absorb these costs more efficiently.

But consolidation raises an uncomfortable question: Is scale being pursued as a growth strategy or as a survival mechanism?

The hidden impact on allocators

The ripple effects extend beyond asset managers themselves.

Investment consultants and multi-managers, the allocators of capital rely on a broad and diverse universe of asset managers to construct differentiated portfolios. Their value proposition depends on access to unique strategies, niche capabilities, and uncorrelated alpha sources.

As consolidation reduces the number of independent managers, allocators face a narrowing opportunity set.

Less diversity in the managers universe may lead to:

- Greater concentration risk

- Fewer specialist or entrepreneurial offerings

- Increased homogeneity in portfolio construction

- Reduced competition-driven innovation

In short, fewer independent managers can mean fewer genuinely differentiated solutions for pension funds and end investors.

Consolidation may strengthen individual firms, but it could also compress diversity across the ecosystem.

Consolidation: Cure or consequence?

There is nothing inherently negative about mergers and acquisitions. In fact, well-executed consolidation can enhance operational resilience and create globally competitive firms.

However, the current wave in South Africa appears to accommodate both strategic expansion and structural pressure with leaning to the latter.

When economic growth is weak, savings pools stagnate. When savings stagnate, AUM growth slows. When AUM slows, margins compress. When margins compress, firms seek scale.

The real long-term solution to industry competitiveness does not lie in balance-sheet engineering. It lies in economic expansion.

Sustainable job creation would expand pension contributions. Revived entrepreneurship would increase institutional capital formation. Infrastructure investment would unlock productivity and corporate growth. Domestic manufacturing and private sector confidence would stimulate broader savings.

Without these structural drivers, consolidation may continue not because firms are thriving, but because they must adapt to survive.

An industry at a crossroads

South Africa’s asset management industry remains sophisticated, well-regulated, and globally respected. The country has produced firms with international reach and strong governance standards. But it now stands at a crossroads.

The next years will determine whether consolidation creates stronger, more competitive national firms or whether it signals a slow contraction of diversity and dynamism within the financial industry.

If scale becomes the only viable model, smaller entrepreneurial managers may struggle to emerge. And yet, history shows that innovation often comes from precisely those smaller, agile firms. The industry cannot outgrow the economy indefinitely.

Until the broader macroeconomic engine is repaired, consolidation may remain the defining feature of South Africa’s asset management landscape not as a bold growth strategy, but as a rational response to constrained conditions.

ENDS

References List

Bureau for Economic Research (2025). Accounting for South Africa’s remarkable growth deterioration: And how can growth be restored? Research Note, September. Stellenbosch: Stellenbosch University.

Bureau for Economic Research. (2025). Economic snapshot: December 2025. Stellenbosch: Stellenbosch University.

27four Investment Managers. (2025). DEInvest Annual Survey 2025. Available at: https://27four.com/wp-content/uploads/2025/10/DEInvest-Annual-Survey-2025.pdf

27four Investment Managers. (2025). DEInvest Annual Survey 2025. Available at: https://27four.com/deinvest-annual-survey-2025/ (Accessed: 12 March 2026).

Association for Savings and Investment South Africa (ASISA). (2025). Local CIS industry records second-highest ever net quarterly inflows. 25 November. Available at: https://www.asisa.org.za/media-releases/local-cis-industry-records-second-highest-ever-net-quarterly-inflows/

Association for Savings and Investment South Africa (ASISA). (2025). Local CIS industry celebrates R4 trillion in assets under management. 14 August. Available at: https://www.asisa.org.za/media-releases/local-cis-industry-celebrates-r4-trillion-in-assets-under-management/

Association for Savings and Investment South Africa (ASISA). (2025). Local fund statistics. Available at: https://www.asisa.org.za/statistics/collective-investments-schemes/local-fund-statistics/