Philipp Wörz, Fund Manager, and Greg Hopkins, Deputy CIO, PSG Asset Management

The Magnificent 7 stocks (Microsoft, Apple, Nvidia, Alphabet, Amazon, Meta and Tesla) have dominated market returns over the past year and currently loom large in the investor consciousness.

In fact, global stock markets, dominated by the US, are at their most concentrated levels in a hundred years. There are currently some clear parallels to the period leading up to the dotcom bubble. We are seeing extreme euphoria in the market, a fear of losing out, complacency in terms of the assumed risks, and importantly, lofty expectations for future returns.

Amidst the euphoria, investors are overlooking the cyclical factors driving these shares’ performance: low inflation, abundant liquidity, and US economic growth. It is doubtful these conditions will persist, which may lead to disappointment.

PSG Asset Management follows a globally integrated process, analysing local and global stocks concurrently. Given the changes in Regulation 28 of the Pension Funds Act, which now allows for up to 45% of assets to be invested offshore, we believe our approach gives us a substantial advantage when it comes to constructing multi-asset portfolios.

We believe that numerous opportunities for attractive returns exist beyond the Magnificent 7. We find these prospects in the often ignored and undervalued sectors of the market. In the long run, we believe this tilts the odds of investment success in the favour of patient investors.

We are also optimistic that some of these unloved sectors are on the verge of a resurgence, as the world adjusts to a higher inflation environment.

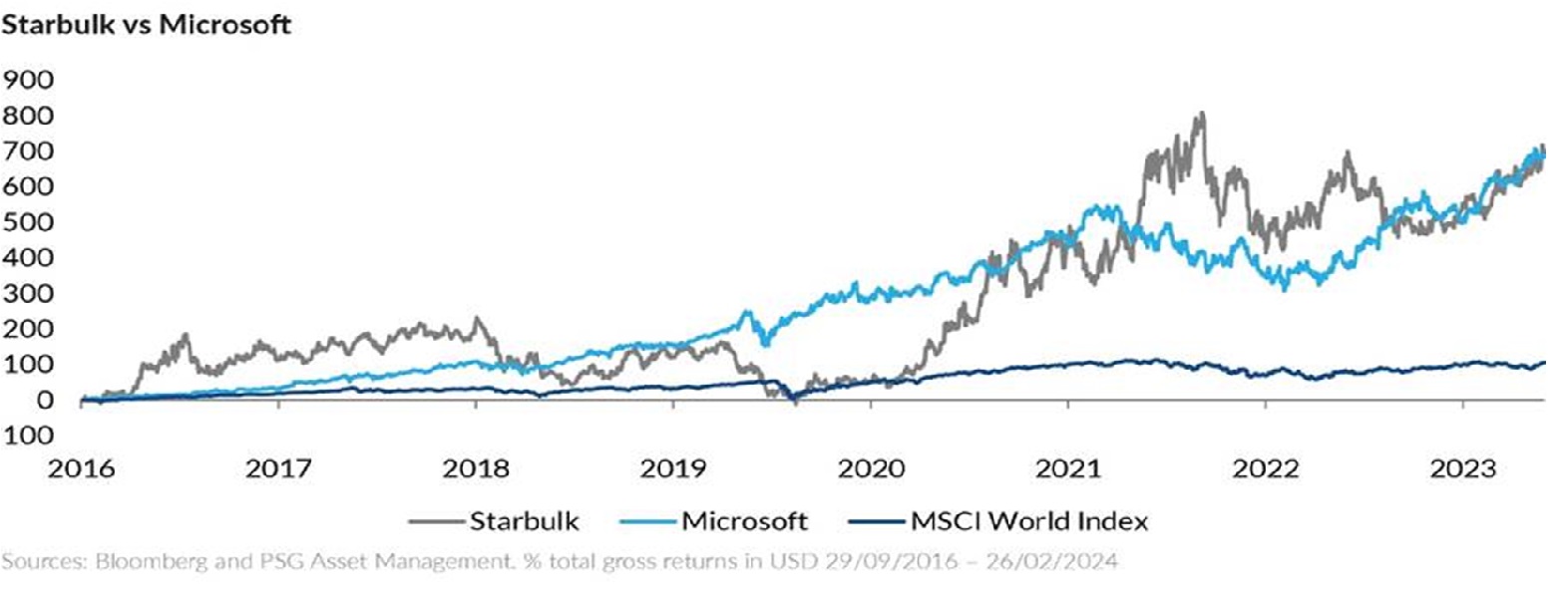

It might seem impossible that any stock could outcompete the current market leaders. However, consider this example from our portfolio history. Starbulk, in which we have been investors since 2016, is a global bulk shipping company which transports grains, iron ore, commodities and coal. After owning Microsoft since 2010 (when it was trading at US$25 and on a price-to-earnings ratio of 9 times), we sold our last shares in Microsoft in 2017 at $73 and switched some of the proceeds into Starbulk.

We watched Microsoft’s subsequent rally with some regret and learned a few lessons from the process. Today, Microsoft trades at over $400. However, the chart below shows that Starbulk has outperformed Microsoft over this period, illustrating that there is life beyond the Magnificent 7.

A recent Bank of America fund manager survey not only reveals the high levels of concentration in currently popular areas of the market (e.g. tech and US bonds), but also clearly shows us what is out of favour at the moment: the UK, energy, the Eurozone, and commodity markets. It should come as no surprise these are areas where we are finding exciting opportunities for future investments.

On a relative basis, opportunities in the unloved and overlooked areas of the market, such as the EU and UK, are the most undervalued they have been in 30 years. Emerging markets are also marking 50-year relative valuation lows vs the S&P 500.

We also believe that despite current investor complacency, clear structural factors support our view of a higher inflation future.

These include a chronic underinvestment in the energy sector, even as energy demand continues to ramp up (in part driven by the ramp-up of artificial intelligence (AI) data centres) and increased reliance on fiscal spending and ballooning government deficits.

Despite these realities investors remain positioned in securities that benefit from a continued low inflation environment, as highlighted in the Bank of America survey mentioned above.

However, we believe the environment that lies ahead is more likely to resemble the period post 1999 than the last decade, and looking at history can provide an important perspective. In the five years following the peak of the market in 2000, technology and US stocks underperformed substantially, while the sectors and stocks that did exceptionally well (emerging markets, real estate, consumer staples, materials and energy) are all sectors that global investors are currently underweight on.

In assessing opportunities, we look to construct portfolios that are well poised to unlock value for investors. Importantly, the earnings forecasts for many of our investee companies are not significantly lower than those of the Magnificent 7, although they trade at far lower valuations.

For example, comparing our portfolios with the MSCI World Index, we see that the MSCI World Index is trading at a price earnings ratio (PE) of 22 with a dividend yield of 1.8%, while the stocks in the PSG Global Equity Fund are trading on a 10.3 PE and a 2.7% dividend yield.

By looking to the unpopular and unloved areas of the market, PSG Asset Management is able to construct portfolios with excellent return prospects (even if current market conditions continue), while also offering upside in a higher inflation environment – at very attractive valuations.

ENDS