Mario Fisher, Head of Quantitative Research and Co-portfolio Manager of the Old Mutual Global Managed Alpha Fund, Old Mutual Investment Group

With the much-anticipated arrival of the Trump 2.0 administration, the US tech sector has been dominating headlines and global debate, as some of the US’s leading tech titans line up to collaborate with Donald Trump’s new government. In the month’s leading up to Trump’s inauguration, there has been significant focus on deregulation of the sector, tax reform, and trade policies that directly influence the technology industry, further boosting the case for US tech stocks.

The spotlight on US tech stocks and their meteoric performance – even before the return of Trump, and particularly following the Covid-19 outbreak – has highlighted concern around dominance of US equities in global benchmarks. This dominance has been driven by the US tech sector, and increasing concentration in global equity markets, a factor that has evolved into a rising risk for global investors seeking diversification, with the level of tech returns unlikely to be sustained into the not-too-distant future.

The recent global selloff triggered by the launch of China’s AI tool, DeepSeek, underscores the current heightened risks in US equities and the precarious strategy of global investors with disproportionate exposure to these markets. This is particularly pertinent as geopolitical tensions and global competition in cutting-edge technologies intensify, with many global investors lacking the global diversification needed to soften the blow of a US economic and market downturn.

The changing dynamics of global markets

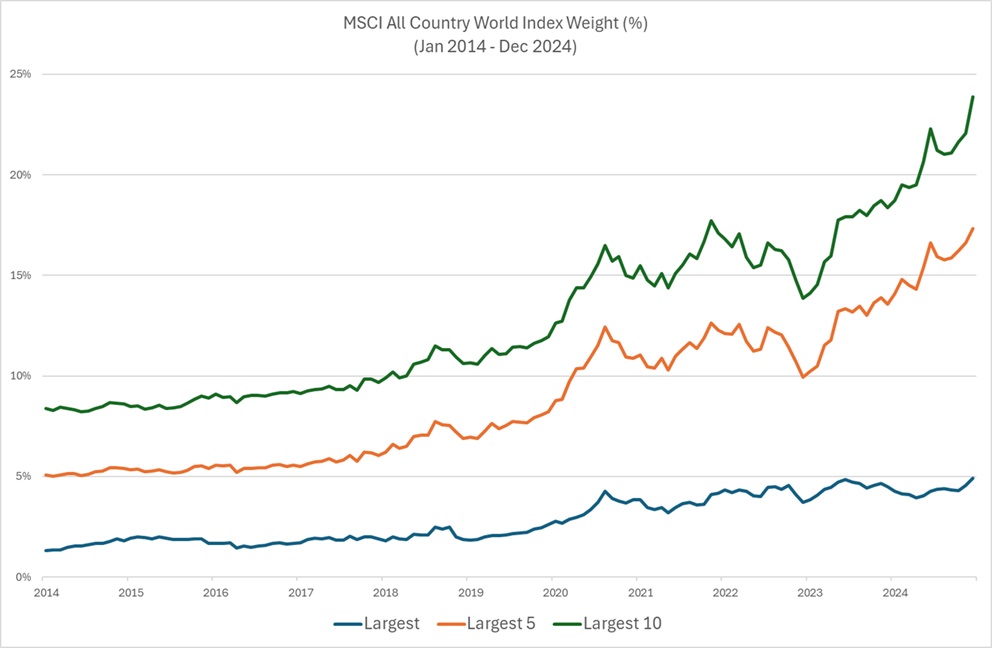

Over the last decade, the MSCI World Index’s top 25 weights have experienced noticeable shifts, largely driven by growth in large-cap technology companies and the changing dynamics of global markets. The outsized returns from mega-cap stocks have not only led to a significant increase in the concentration of market-capitalisation-weighted indexes, but also to concentration in specific Global Industry Classification Standard (GICS) sectors and the companies within certain sectors.

In the past, sectors such as industrials and energy have been concentrated, however, their index weights were not as relatively high as the current 25% weight of information technology (IT). In recent years, the top 10 stocks by weight in the index triggered higher concentration within and across global sector exposures. For example, concentration in the global tech sector increased because of Apple, Microsoft and NVIDIA, in the consumer-discretionary sector because of Amazon and Tesla, and in the communication-services sector because of Alphabet and Meta, all ultimately belonging to the US tech sector.

Financial companies like JPMorgan Chase, Bank of America and Healthcare companies like Johnson & Johnson and Roche, who were in the top 10 by weight, still hold substantial weights in the index, however, their relative influence has been diluted as IT companies expanded.

The growth of major US tech giants and their global market dominance has come at the expense of other regions like Europe and Japan, who have seen their relative weights shrink over time. US companies now represent approximately 73% of the index, which is a significant rise from about 50% a decade ago.

Aside from the fact that equity markets are currently plagued by geopolitical concerns, assumptions about growth and interest rate projections, most concerning for investors is that US stocks are trading at historically high valuation levels. On this basis, returns from US stocks over the medium to long term will probably be subdued. A lack of diversification in global portfolios exposes investors to the increasing risk posed by US equities, as a downturn could disproportionately affect returns.

Emerging opportunities

While one of the core benefits of global investing is diversification, most global equity strategies available to South African investors often have a bias toward developed market (DM) stocks, where there is a plethora of stocks to invest in from across the globe, but where concentration is a hindrance.

Higher risk is often cited as the key reason for the omission of emerging market stocks; however, little is said about the diversification benefits and growth potential that investors can get from having such exposure.

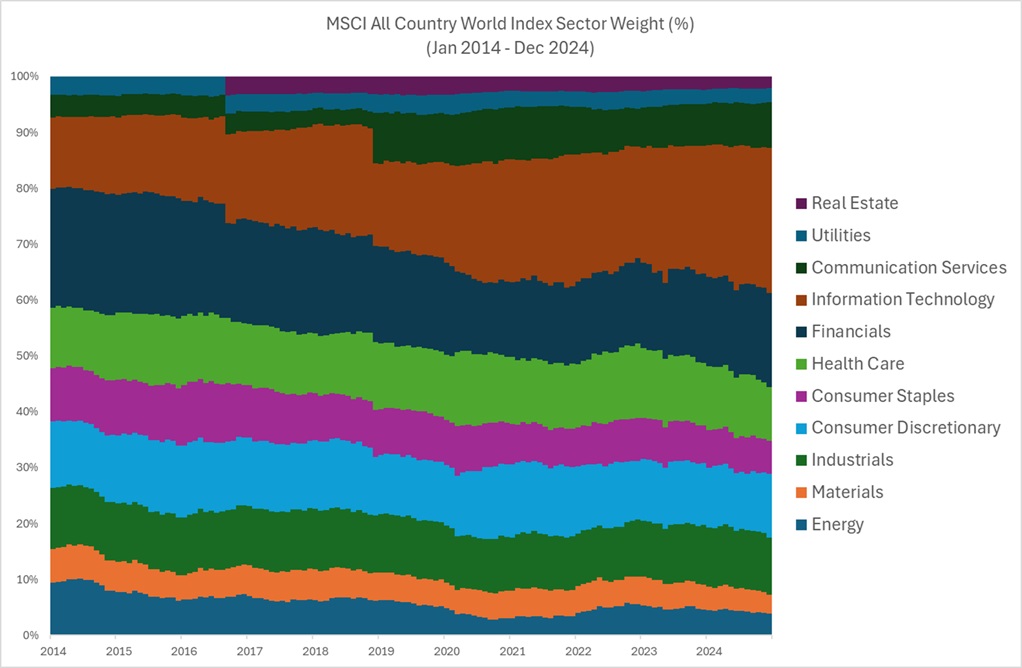

Unlike the MSCI World Index, which only includes developed markets – specifically 23 countries that are considered economically developed – The MSCI All Country World Index (ACWI) represents large and mid-cap companies across developed and emerging markets countries. The index covers approximately 85% of the global investable equity opportunity set and is more diversified than the MSCI World index predominantly due to the countries they represent, such as China, India, Brazil and South Africa, and their sector exposure.

While emerging markets tend to be more volatile, they also provide higher growth potential, a factor that is often overlooked by global investors seeking the relative stability offered by developed markets. The MSCI ACWI’s exposure to emerging markets also gives it more sector diversification and more geographic exposure, as emerging markets are often driven by different economic factors than developed markets.

Both the MSCI ACWI and MSCI World indices are market-cap weighted, meaning that companies with higher market capitalisations have a larger weight in the index. However, because the MSCI ACWI includes emerging markets, it captures the growth potential of large-cap companies in these regions, adding another layer of diversification in terms of the types of companies and industries.

Ultimately, the inclusion of emerging markets introduces more diversity in terms of sector composition. MSCI ACWI still has a large weight in technology, however, the addition of countries like China, India, and Brazil means more exposure to sectors like consumer goods, energy, and materials, which are not as dominant in the developed world.

The current case for emerging markets

Emerging markets have hardly been the darling of the global investment sphere in recent years, lagging their developed market peers over this period. With President Trump’s tariff policy casting an increasing shadow over the region, confidence in emerging markets prospects for a rebound is declining further.

However, over the past, while emerging markets offer only 20% of global market value, they contribute around 45% of global GDP. And if you look at energy consumption and carbon emissions, over 60% is consumed in emerging markets, with emerging markets land area at over 80% and population closer to 90% of the global population. What is striking is that all these factors are the fundamental drivers of productivity. Therefore, shouldn’t we naturally expect that over the coming decades the market cap of emerging markets will also positively change?

Contrary to popular belief, investors need to be prepared for the next investment wave, which belongs to emerging markets.

Emerging markets diversification in practice

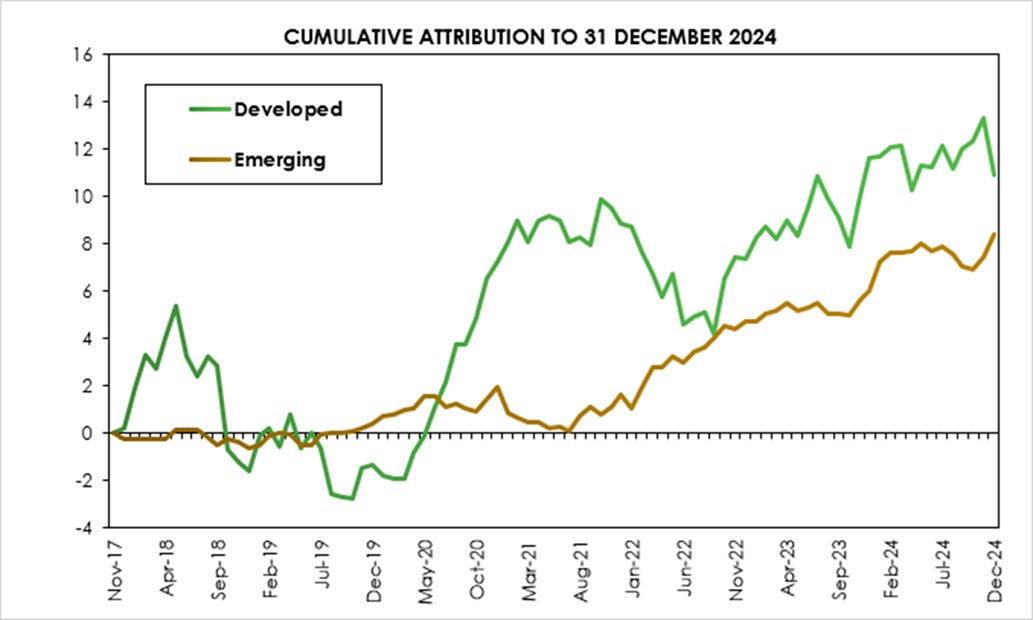

Our Old Mutual Global Managed Alpha Equity Strategy, launched in 2017, is an ideal case study for why investors should consider emerging markets exposure in global investments, particularly against the current global market backdrop and rising dominance of US tech stocks. The strategy uses a systematic model which allows for a widened opportunity set – adopting the MSCI All Country World Index (ACWI) as our benchmark instead of the MSCI World Index. This is one of the fund’s key differentiators from other global funds.

Despite the tough emerging markets environment, the model has successfully identified emerging market counters that exhibited the relevant factor drivers. In the below chart we have split the excess return that the fund achieved since inception into stocks from developed markets and stocks from emerging markets.

Emerging market risk management

Although we have access to emerging markets stocks, the fund is positioned as a core equity building block and therefore adheres to stringent tilt limitations versus its benchmark – a maximum of 1.0% over- or underweight per individual stock and a maximum of 3% over- or underweight per country and sector.

Potential double whammy

From the data above, it is evident that an expanded universe, covering both developed markets and emerging markets, can be a real benefit to a systematic model – even in a tough environment. Importantly, the Old Mutual Global Managed Equity Alpha Fund’s performance has shown that it is not reliant on a recovery in emerging markets. However, it is worth noting that if emerging markets do reverse the current trend and stage a recovery off a low relative base, this could be an additional tailwind for a fund that uses the ACWI, as opposed to most global equity strategies exposed to a developed markets-only universe, and it could therefore see better returns.

ENDS