Izak Odendaal, Investment Strategist at Old Mutual Wealth

Every now and then markets hit a serious wobble that forces the question: What is going on? And what should we do about it? The past week was one of those occasions.

Geopolitics and politics

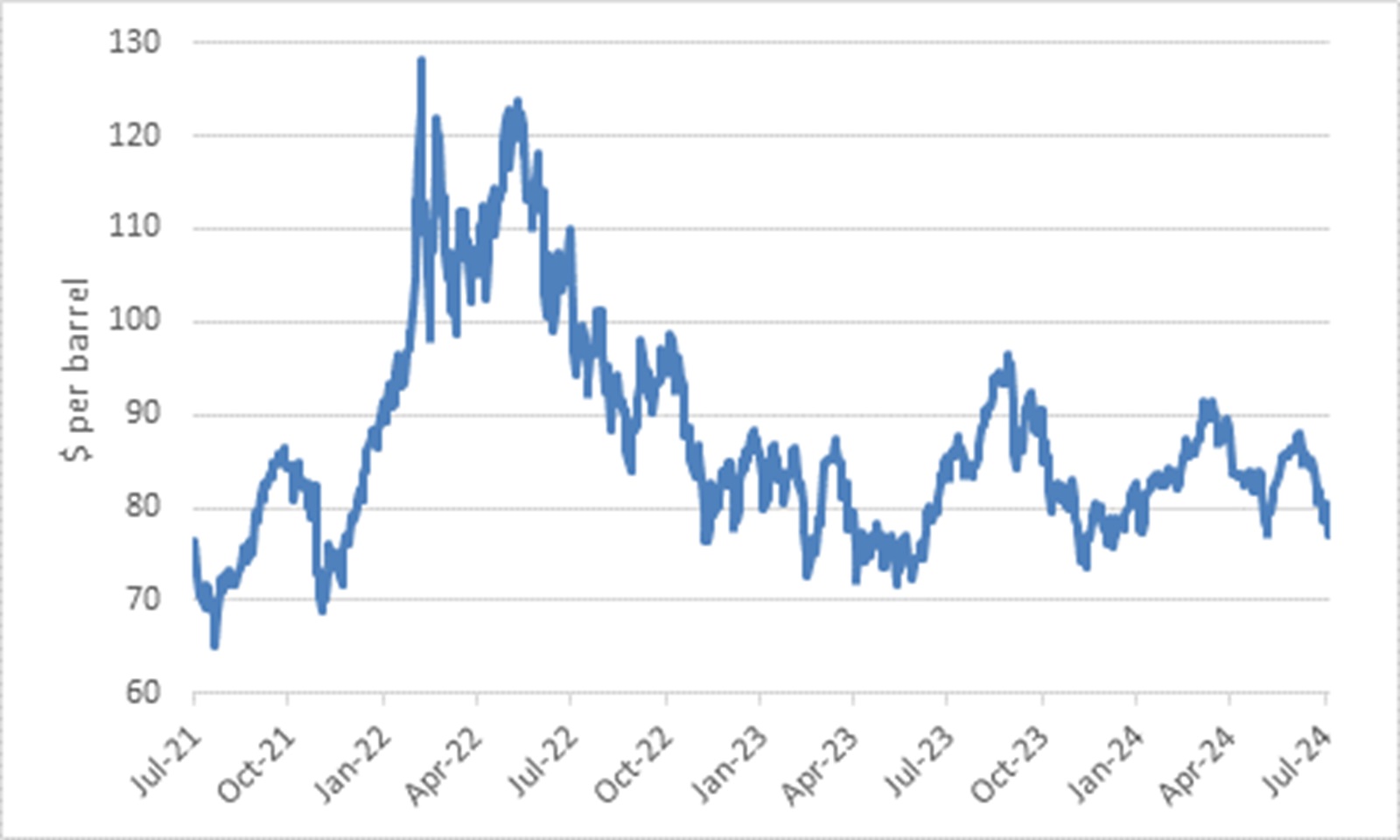

It was a week where Russia launched a massive drone attack on Kiev, and Israel killed a Hezbollah leader in Lebanon and (allegedly) a Hamas leader on Iranian soil. While the war in Ukraine seems to have ground to a bloody stalemate, the fear of an escalation in the Middle East remains real. Wars are tragic and doubly as people in other parts of the world quickly forget about them when they are not directly impacted. This conflict affects the oil price which can impact the global economy negatively. However, it remains within its trading range of the past few years and does not pose a big risk at current levels.

Chart 1: Brent crude oil price

Source: LSEG Datastream

Recession risks reappear

While politics and geopolitics hog the headlines, the biggest concern of any investor with an equity-heavy portfolio is a global recession, more specifically a US recession. (US equities make up 60% to 70% of global equity market capitalisation.) In a recession, company profits fall, which drags share prices lower, but the market also usually suffers a multiple contraction. In other words, not only do earnings fall, but the price: earnings ratio also declines. People lose their jobs and must sell their most liquid investments to make ends meet. The dollar also tends to strengthen in a flight to safety, which further depresses non-US returns. With one exception (1987), the major global equity bear markets of the modern era have coincided with recessions in the US.

Unfortunately, despite the best efforts and collective brain power of thousands of economic forecasters worldwide, spotting recessions in advance remains a tough job. And as per the punchline of many a joke, put five economists in a room and you will likely end up with six or more predictions. One of the reasons recessions are so feared is because they often appear unexpectedly.

The best we can do is to see if the conditions that gave rise to a recession in the past are present today. A simple way of thinking about it is that the bigger the party, the more severe the hangover. Often when economies experience rapid growth, all kinds of imbalances build up that are prone to a vicious reversal. This usually means households taking on too much debt to fund their lifestyles and companies overinvesting for a rosy future that never materialises. A real estate boom is often at the heart of such problems. In the case of developing countries, the problem is often that hot money flows in during the good years and fund unsustainably high levels of imports. When the hot money leaves for whatever reason, these countries find themselves desperately short of hard currency and the economy is forced into contraction. (Similarly, when a particular trade becomes very popular among investors, it is also prone to a violent reversal. If everyone sits on one side of a canoe, it can tip over. That seems to be the case with the sharp rally in the Japanese yen and decline in Japanese stocks following Bank of Japan’s rate hike).

Back to the present, US household and company balance sheets are generally in good shape and there has been little by way of reckless private borrowing. This is a source of strength. Confidence surveys, for example, have remained subdued, not pointing to a mood of excessive risk-taking on the part of consumers and companies.

However, there are pockets of weakness in the US where high interest rates have really put on the squeeze, however, notably smaller businesses, commercial real estate, and low-income households. Manufacturing has also been soft, and the latest data points to fresh weakness in the US and elsewhere.

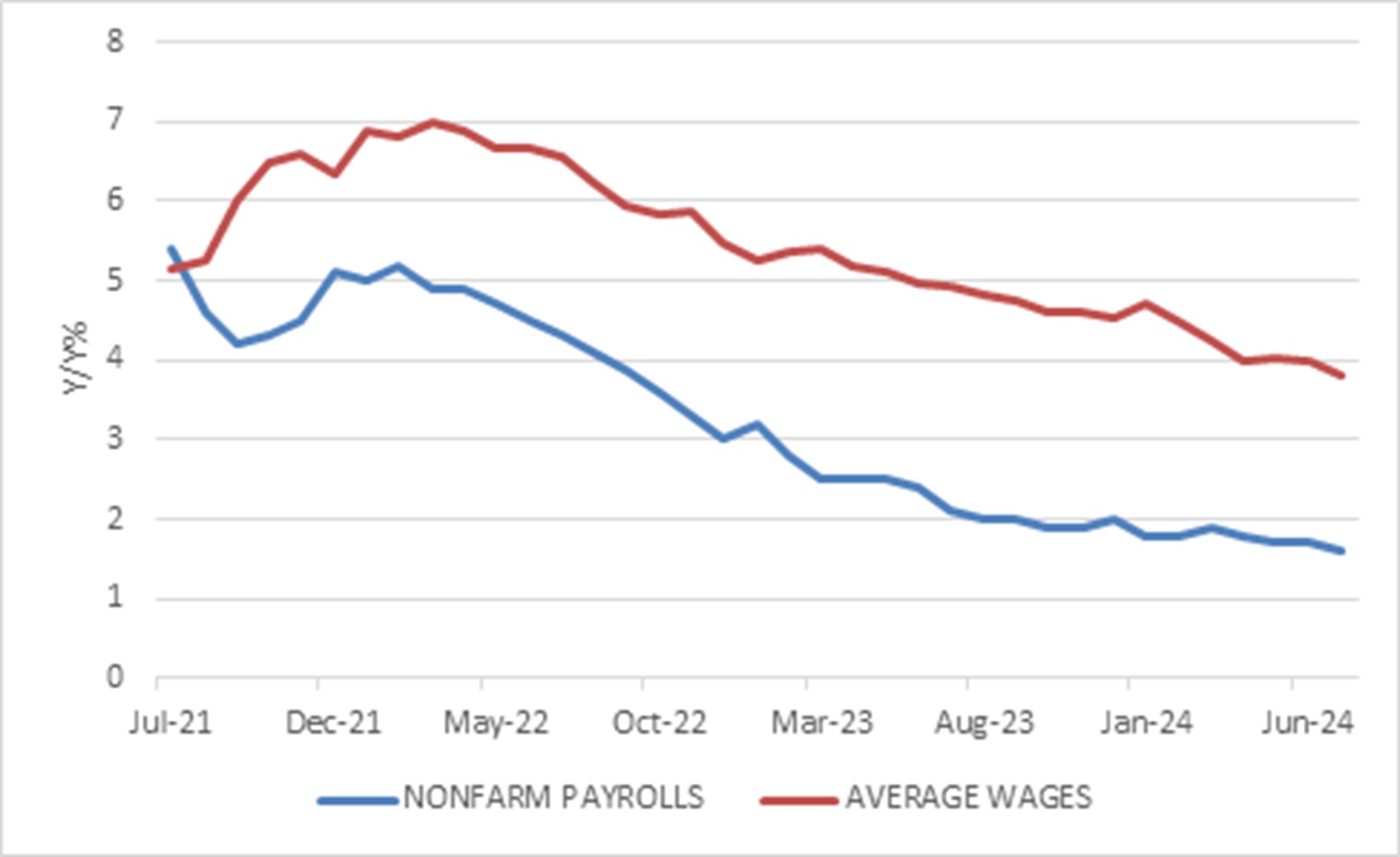

The main concern is that American job growth slowed notably in July, with only 114,000 jobs added, below expectations. Moreover, the unemployment rate ticked up to 4.3%. While still low, it has increased in recent months. Wage growth slowed to below 4% year-on-year. The labour market is clearly cooling (“normalising” is probably a better description, following pandemic and aftershocks) though the current pace of growth can still sustain a decent, if slower, expansion in consumer spending. Moreover, the labour market is increasingly unlikely to be a source of upside inflation pressure, i.e. a wage-price spiral. The big question is whether it goes from cooling to cold. Rising joblessness would put pressure on consumer spending, which would in turn lead to companies cutting jobs to preserve margins. Things can snowball quickly.

Chart 2: US employment and wage growth

Source: LSEG Datastream

Already, several large consumer-facing companies reporting earnings have noted that they are unable to raise prices to expand margins since consumers are not able to absorb such price increases. But this also implies lower inflation.

The good news is that the US Federal Reserve (the Fed) can cut rates from the current elevated level to relieve pressure on vulnerable sectors of the economy, since inflation worries have reduced significantly. The same is true of central banks elsewhere, especially given that the Fed easing creates room for others to cut rates without fear of major currency weakness.

The Fed held rates steady at its scheduled meeting last week, but its statement and comments by officials suggest it will start cutting rates in September. Specifically, with progress being made towards its 2% inflation target, it acknowledged that it is time to start paying attention to the other side of its dual mandate, maintaining full employment.

Is September too late to start cutting? Some argue that it is, but bear in mind that a large part of the easing happens not because of what the Fed does with its short-term interest rate, but where the market believes it is heading. In other words, bond yields across the curve already price in the coming interest rate cuts, lowering borrowing and refinancing costs for a range of borrowers. If the expected cuts did not materialise, however, it would really upset the apple cart.

Now, it is often said that “this time is different” is the most dangerous phrase in investing. Nonetheless, it has been a very unusual cycle due to the shock of the pandemic and the aftershocks of war, supply chain disruptions, commodity price spikes, inflation and ultimately, a once-in-a-generation surge in global interest rates. Some of the usually trusty leading indicators, such as the inverted yield curve, have seemingly not worked (not yet anyway). Key cyclical sectors such as manufacturing and housing have already experienced the downturn that in the past would have spilled over into other sectors. Rather than a single recession, the US economy might have already experienced a series of rolling sector-level contractions.

It was always likely that overall US economic growth will slow from current levels, but we also know that there is a lot of pent-up demand in the housing sector, for instance, which can be unlocked if interest rates start to fall.

Diversification is back

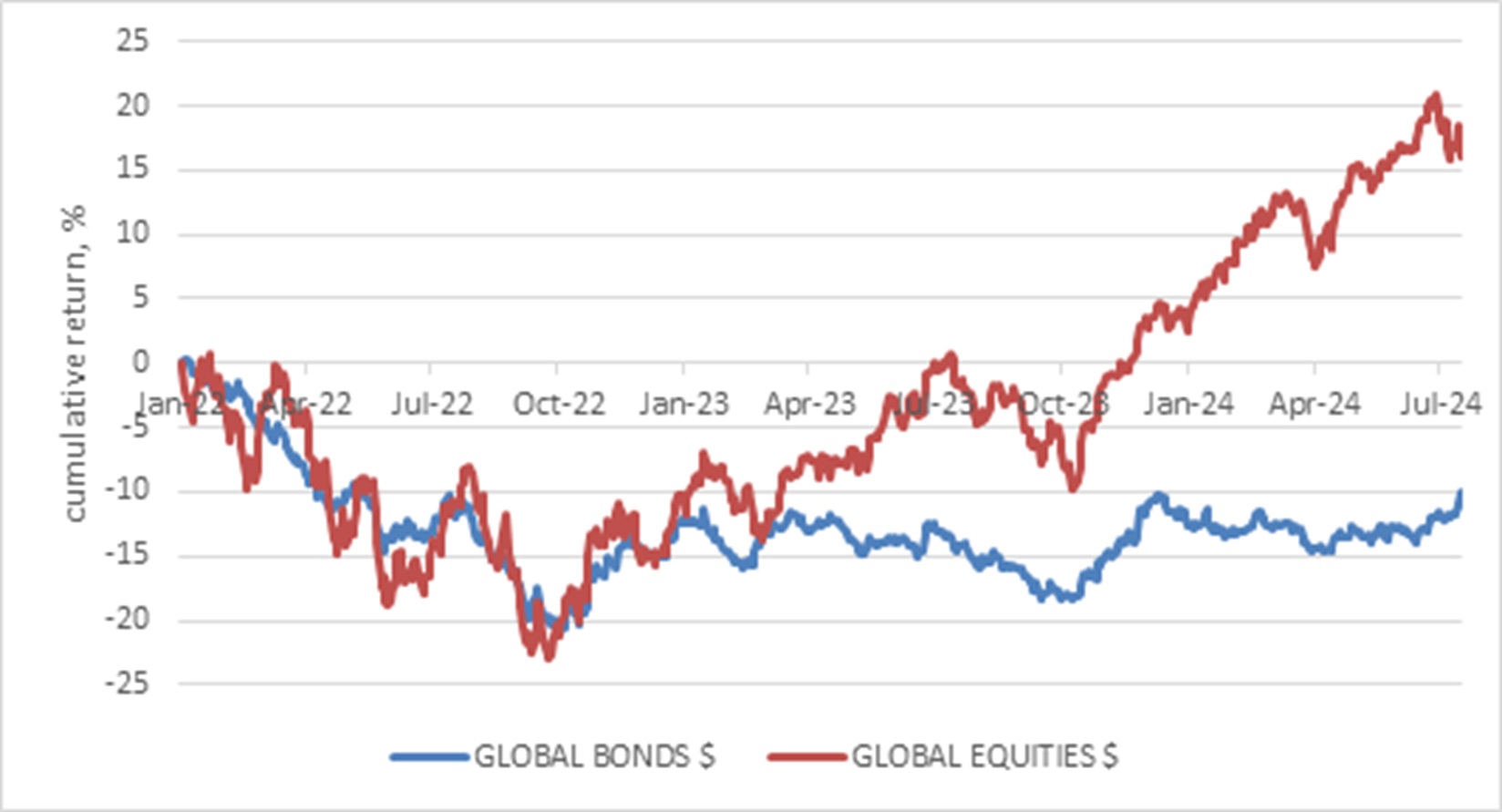

While one should never read too much into a few days’ market movements, there was one notable feature: as equities fell, bonds rallied. Diversification is back. In contrast, during the 2022 global equity bear market, bonds had a historically big collapse, leading some commentators to declare the 60/40 balanced portfolio dead. Aggressive interest rate hikes by the Fed and other central banks cratered equity and bond valuations, especially since the latter was so expensive to begin with (bond yields and prices move in opposite directions).

At the start of 2022, the 10-year US government bond yield was only 1.4%, while the UK equivalent was only 0.7%. German bond yields were still negative. From such low levels, yields could only go up as inflation rose and central banks responded, and they did, meaning that bond prices fell sharply.

In fact, global bond returns have not yet recovered from the 2022 crash However, at the start of this year, the 10-year US bond yield was at a far healthier 4%, and in recent weeks bond prices have rallied, pushing the yield below 4%.

Chart 3: Global equity and bond returns since 2022

Source: LSEG Datastream

What about equity valuations? It is probably a factor in the sell-off of the past few days. US equities have been trading at elevated valuations, implying that investors were pricing in a very rosy future. With no margin of safety, the slightest disappointment on reported or expected earnings growth can see share prices fall.

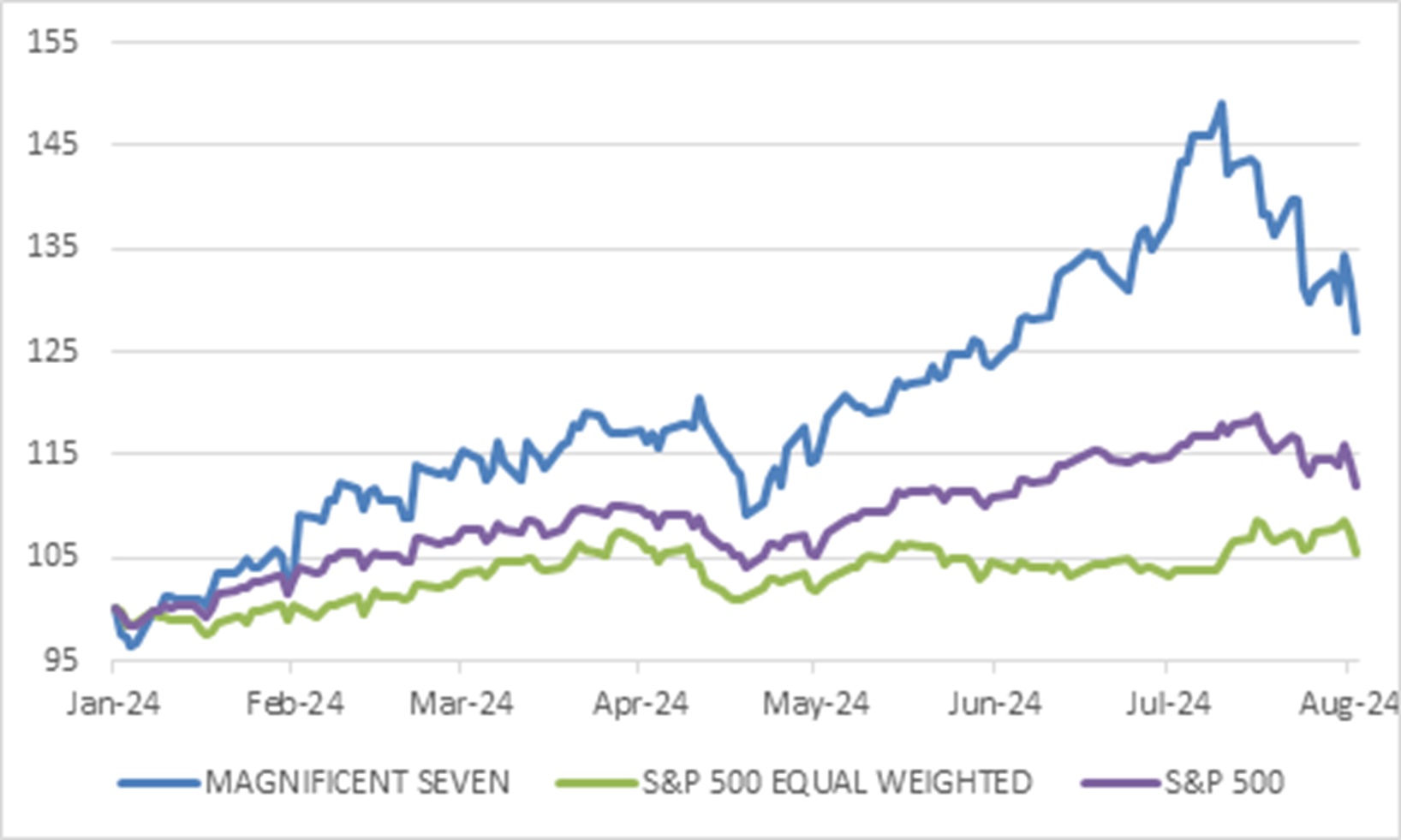

That has been the case with the mega cap tech companies, grouped together as the Magnificent Seven (or six, depending on who you ask). Since these companies now dominate global equity benchmarks, it is relevant to practically all investors. Several of these companies reported results to the market last week that showed ongoing strong earnings growth, yet still disappointed a market that expected more. Phenomenal companies that they are, they were seemingly priced for perfection. And after the incredibly strong run they’ve had, no one should be surprised that there has been a pull-back, though the timing can be quite surprising.

Chart 4: The Magnificent Seven versus the rest

Source: LSEG Datastream

Valuations still matter

Often, the bigger risk to investors is not volatility, but overpaying. An investment, such as a share or a rental property, can deliver strong and growing cash flows and still generate a disappointing total return if the starting price is too high. The more its valuation was dependent on blue sky, the further it is likely to fall in a downturn. Cheap shares do not escape a general sell-off or a recession, but they usually have less room to derate.

For the Magnificent Seven, this might turn out to be a short-term headwind. It depends a lot on whether artificial intelligence turns out to be a truly revolutionary technology, or merely evolutionary, offering incremental productivity gains. We’ll only know for sure in the years to come. What we do know is that the last time the US traded at a forward price: earnings ratio of around 21, in 2002, the subsequent returns were flat for a decade. Granted, it was much more of a speculative bubble back then compared to today – the Magnificent Seven are all very profitable – but the warning still stands. A high starting valuation is a headwind to longer-term returns.

Fortunately, other areas of the global equity market are not as expensive, and investors still have much to choose from. In 2002, non-US developed market equities traded at similar valuations to the US, as chart 4 shows. Only emerging markets were not caught up in the dotcom bubble and enjoyed a rerating and stellar returns thereafter. Today however, the MSCI World Ex US Index (non-US developed markets) trades at a substantial discount to the US, as do emerging markets apart from India.

Chart 5: Forward price: earnings ratios

Source: LSEG Datastream

In conclusion, market volatility is never pleasant, but one benefit is that it forces investors to grapple with the assumptions they’ve previously held. If those assumptions have changed, it might call for a different asset allocation. If not, it is best to just stay the course. The biggest mistake is usually to react to the market volatility itself, instead of to perceived changes in the fundamentals. A US hard landing still seems unlikely, but economic growth is cooling. Elsewhere in the world, such as South Africa, it is picking up speed. As noted above, a valuation-based approach does not protect against such volatility in absolute terms, but it does help to avoid some of the big air pockets. It also helps investors to keep a look out for opportunities where the market overreacts.

ENDS