Izak Odendaal, Investment Strategist at Old Mutual Wealth

Friday was the 249th anniversary of the US Declaration of Independence, signed on the 4th of July 1776 in Philadelphia. Next year will see huge celebrations and 250 candles on the cake. These will not be enough to overcome the deep political divisions, however, and the focus will quickly turn to the midterm elections in November. Whether the strength of the US economy will still be cheered is a big question for investors around the world. If the US economy can maintain a degree of vigour, it can sustain the rally in US equities. However, it might also limit the scope for interest rate cuts, at least while Jerome Powell is holding the reins as Federal Reserve chair.

With big social and political changes underway, the longer-term direction of the world’s largest economy is also in question. The topic of the US dollar and its central role in the global system will be tackled in a separate upcoming note.

Less miserable

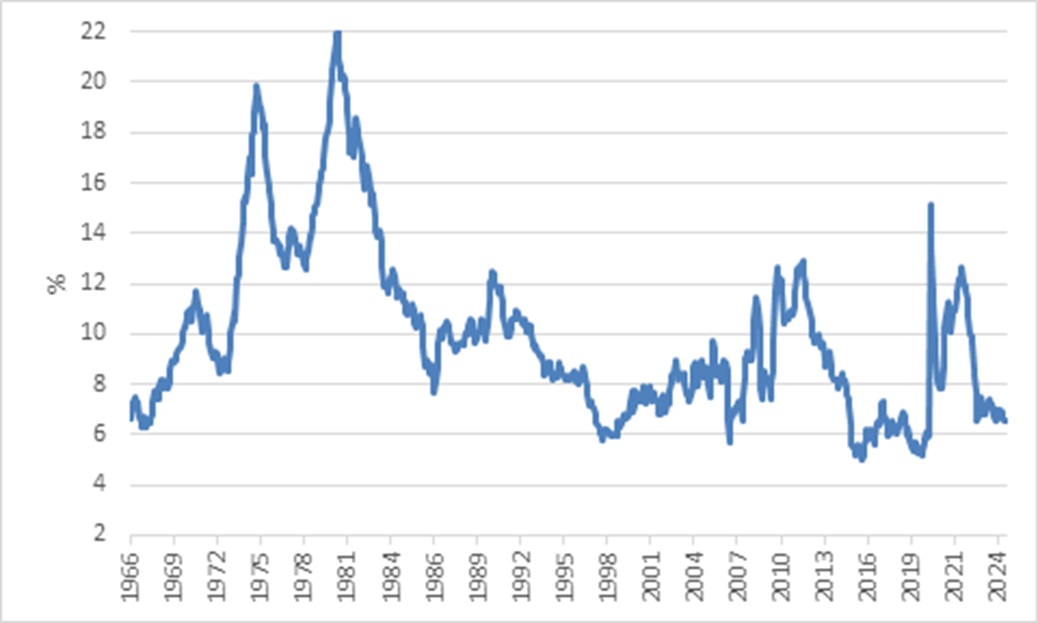

Let’s start with the near-term outlook. Despite his protestations to the contrary, Trump won the election with the US economy in decent shape, at least at the aggregate level, and certainly compared to other developed markets. One way of showing this is the so-called Misery Index, which simply adds together the unemployment and inflation rate. It jumped between 2020 and 2022 as a result of massive job losses and then due to the post-pandemic inflation surge. By late-2023, however, it was close to pre-pandemic levels.

Chart 1: US Misery Index

Source: LSEG Datastream

Inflation has been slow to return to the Federal Reserve’s 2% target, but has generally drifted lower, while the unemployment rate was 4.1% in June, near historic lows. The US economy added a healthy 147,000 jobs in June, more than expected by economists. However, most of the new jobs were in the public and healthcare sectors, and not in cyclical industries. While there is little indication of widespread job losses, there are signs that people who have lost jobs are struggling to find work again. This suggests some weakness underneath the surface.

Tariff trouble

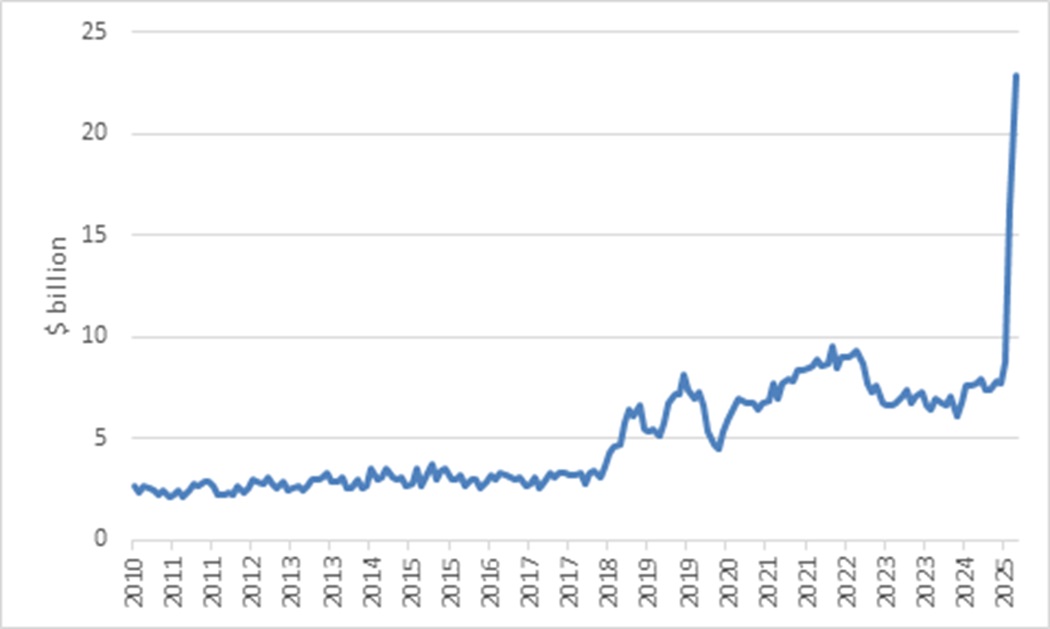

There is an obvious headwind: President Trump’s tariffs. These are already clearly visible in customs data, with $23 billion collected in May, a significant jump from previously. What we don’t know is where exactly tariff rates will settle. A handful of countries, notably the UK, China and Vietnam, have reached trade agreements with the US, but for the rest we’ll find out this week when the 90-pause on reciprocal tariffs will expire. It is unlikely to be the end of the matter completely, and new threats and deadlines are likely to emerge from time to time. The uncertainty is not helpful, but the effective tariff US rate (the average across all categories and countries) will probably eventually end up somewhere between 10% and 15%, much higher than the 2.5% at the start of the year, but not quite as bad as feared in April.

Chart 2: US tax receipts from customs duties

Source: LSEG Datastream

What we also don’t know yet is how exactly the tariffs are impacting business activity, pricing and margins. Many companies and households brought forward purchases to avoid tariffs, and this might be giving us an artificially upbeat view of the US economy as well as exporting economies. Similarly, few firms will have passed on tariff-related costs to consumers yet, so the latest inflation data is not telling the whole story either. It is unlikely that the full impact has been felt, in other words.

Easing the blow

Other policies can ease the blow of the tariffs. As noted, the Fed has not cut rates this year, mainly because it’s been concerned about the potential inflationary impacts of tariffs, but also because of the seeming resilience of the US economy. With its policy interest rate at 4.5%, there is room to ease, and the market is discounting two cuts before year-end and more next year, notably after Powell’s term in office ends in May. Trump has been arguing volubly for lower rates and insisted that Powell’s successor will be cutting rates.

Fiscal policy will also provide a boost. Congress passed the (absurdly named) One Big Beautiful Bill Act (OBBBA) last week, which includes tax relief, especially early next year when refunds are due.

However, the stimulative impact is limited by the fact that the bulk of the relief is not new but rather an extension of the 2017 cuts, which were set to expire. Secondly, there are deep cuts to healthcare and social welfare that will start kicking in next year. The political wisdom (and morality) of reducing the tax burden of the affluent while shrinking the safety net aside, there is also bound to be a negative economic impact. Less public health coverage means patients will either have to cough up or forego treatments. The latter will impact healthcare providers and slow the strong pace of job creation in the sector noted earlier.

The higher customs receipts from tariffs will not offset the budget impact of the tax cuts, and the OBBBA will therefore add an estimated $3 trillion to the already-large US budget deficit over the next decade. This is a massive and reckless expansion of US government debt given that there is neither an economic crisis nor war underway to justify so much extra borrowing.

Long-term headwinds

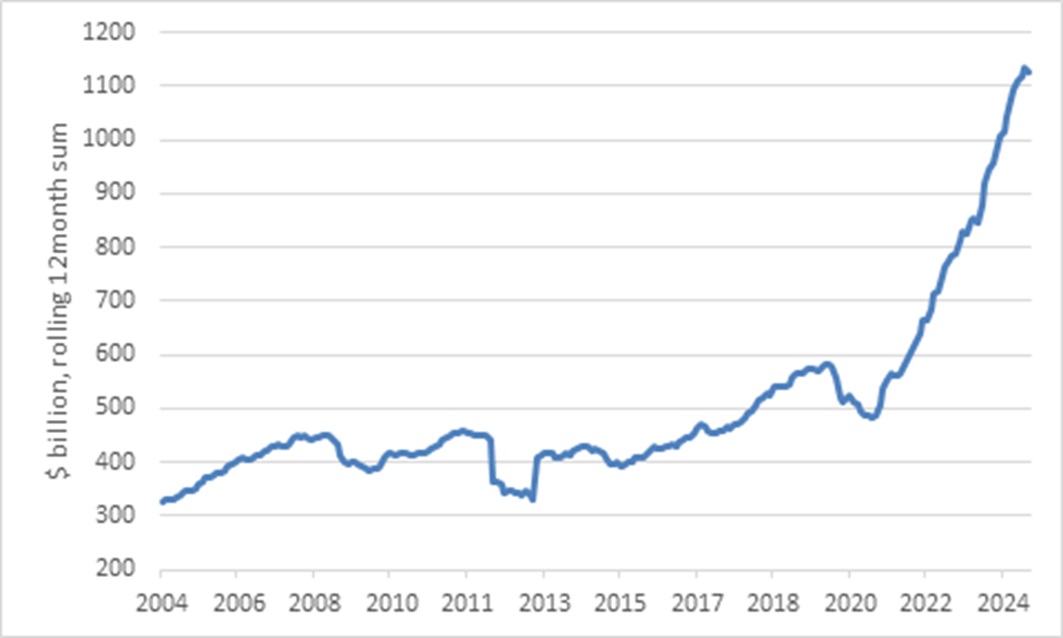

This is the first of five long-term headwinds to highlight. The US government is already spending $1 trillion dollars on interest payments a year. Ten years from now, the number will likely have doubled. The US will be where South Africa is today in terms of spending around 5% of national income on interest. This is not a debt crisis per se but means that interest payments will squeeze out more important spending items. If the US economy was to face a serious economic downturn, there would simply be less fiscal space to respond with genuinely needed stimulus.

It could also lead to a vicious cycle where deteriorating perceived creditworthiness puts upward pressure on bond yields, which raises the interest burden, and in turn further worsens creditworthiness. This is South Africa’s experience over the past decade, and it is not an easy cycle to break. The US is not South Africa. It issues the world’s risk-free sovereign bond and reserve currency, but seems to be gambling with that status. Unfortunately, the deep political divisions make it difficult to see where the backbone will come from to turn the situation around absent a crisis.

Chart 3: US federal government interest payments

Source: LSEG Datastream

Moreover, the US is spending tomorrow’s money today, and not necessarily on useful things. It is one thing to splurge on new infrastructure and military capabilities, as Germany’s new chancellor wants to do. That will have positive payoffs over time. But the OBBBA is mainly giving away to people who are already rich, doing little to enhance the country’s economic potential (unless you believe, as some do, that tax cuts are by themselves positive for long-term growth).

It might even be harmful. The second headwind of note is that the OBBBA phases out Biden-era tax credits for renewable energy. In other words, while the rest of the world is actively pursuing renewable energy, the US wants to discourage it. This is tragic from the point of view of tackling climate change, a truly global problem, but from a purely economic point of view, also doesn’t make sense. The US has vast oil and gas reserves, so the country won’t face loadshedding as we’ve become used to in South Africa. However, it is surrendering leadership to China and missing out on the energy sources of the future. The solar panel was invented in America, and President Carter installed some in the White House back in 1979 already. Today China dominates the renewable energy supply chain and is adding as much solar and wind capacity as the rest of the world combined.

Lost labour

The third long-term concern is immigration. The Trump administration has already tightened up border security substantially and started rounding up suspected illegal immigrants. The OBBBA will provide significant financial firepower to scale up, $150 billion over 10 years in total. this up to $150 billion in total. Immigration is a political hot potato across the world and must be properly managed. However, it is possible to go too far. And putting morality and politics aside again, from a purely economic point of view, the US needs immigrants especially on farms and building sites. With the native-born labour force no longer growing, labour shortages could be a reality in years to come, and not just low-skilled workers. One of the biggest advantages in the US over the years has been attracting the most talented people to its universities and cutting-edge industries. These people could now be more reluctant to come to the US, and indeed other countries are actively trying to lure them away from America. This leads to the fourth area of concern.

It is difficult to know what the long-term impact of deep cuts in public funding for scientific research and universities will be, but it can’t be good. Public funding sits behind some of the most important technological and scientific breakthroughs of the past 60 years. The list includes the flu vaccine, MRI scans, microchips, barcodes, smartphones, genetic screening and GPS. Modern life would not be possible if the US government did not provide financial support to scientists who were able to turn theories into practical applications and ultimately into businesses.

If some of the above sounds pessimistic, you wouldn’t say so by looking at the equity market. The S&P 500 recently hit new all-time highs and unwounded some of its first quarter underperformance against non-US equities. The equity market seems to reflect a view that earnings growth will remain robust, despite tariffs, and that the tariffs themselves will not end up at extreme levels. But it also seems that US corporations, unsure of what to do in an uncertain environment, have decided to buy back their own shares instead. According to S&P, first quarter buybacks amounted to a record $283 billion, 20% higher than the fourth quarter of 2024. The second quarter data is not out yet but is unlikely to show a marked slowdown.

No margin of safety

At a forward price: earnings ratio (PE) of 22 times, there is no margin of safety should the economy turn out worse than expected, particularly if spending on artificial intelligence (AI) slows. While AI is very exciting, tech companies might eventually realise they are overdoing things and scale back AI-related capex.

Chart 4: US bond and equity yields, %

Source: LSEG Datastream

The inverse of the PE ratio is the earnings yield, which we can compare with bond yields as an indicator of the equity risk premium, the compensation for holding riskier equities over “risk-free” bonds. With the forward earnings yield at 4.4% and the 10-year Treasury yield at 4.3%, that premium is currently close to zero. This suggests some combination of investors either seeing no risk at all in equities or not considering bonds to be risk-free anymore given the fiscal problems highlighted above. This doesn’t tell us anything about where the market will trade over the next few months, but if we stretch our horizon to five to 10 years, it points to below average returns.

Multi-polar

Back in 1776, America’s Founders knew they were busy with something of world importance, even if the 13 colonies that declared independence from Britain were a backwater at the time. They wouldn’t have known how the US would become the greatest dominant economic, financial and military power ever.

With an unrivalled geography, entrepreneurial culture, massive internal market for goods and services, deep and liquid financial markets, world-class universities, and more, one can never bet against America. However, one can get carried away betting on its enduring exceptionalism. Much of the outperformance of US equities over the past 15 years can be attributed to superior earnings growth and being home to the world’s best technology companies. But at least some of it was due to rising public debt levels, increased spending on healthcare even as health outcomes worsened, a strong dollar, and expanding equity valuations, factors that cannot repeat again and again. There are good reasons to believe that the next ten to 15 years will be different. It is not that there is one obvious alternative, since Europe, China, Japan and other large economies all have shortcomings of their own. Instead, it is shaping up to be a more multi-polar world, in geopolitics as much as in portfolio positioning.

ENDS