Kevin Cousins, Head of Research, PSG Asset Management

Indexation and passive investments have become extremely popular over the past few decades. In theory, these strategies offer cost-effective access to markets and an easy way to construct portfolios. However, their efficacy (and continued success) is predicated on a few pivotal assumptions about how markets function. These assumptions may, however, be less foolproof than many investors realise, which has substantial implications for investors’ portfolios, especially in highly concentrated markets.

Index use tends to go unquestioned in the investment industry

Indices have become ubiquitous in the investment industry. Firstly, active managers use them as benchmarks (typically in their risk models), and secondly, they serve as the basis for passive investing. As such, there is hardly a corner of the investment industry that has remained untouched by the use of indices. However, this also means that their use tends to go largely unquestioned.

The effectiveness of indexation is predicated on a few key assumptions. John Bogle launched the first retail passive index fund, the Vanguard 500 Index, in 1975. Today, Vanguard’s assets under management (AUM) have grown to US$10 trillion and more than 50% of total US equity AUM is managed on a passive basis. Passive investing has proved popular because it offers lower fees, good performance and a simple strategy that is easy to understand (and replicate).

However, Bogle frequently highlighted that indexation works for some very specific reasons. To paraphrase him:

- Indexing works because it’s a free ride on the efforts of others. If there were no others, there’d be no free ride.

- The beauty of indexing is that it works because it’s not the dominant strategy. If it ever became the dominant strategy, we’d have problems. (Ref 2)

- If everybody indexed, the only word you can use is chaos, catastrophe… The markets would fail. (Ref 1)

Effective passive management requires a thriving active manager population

Ironically, passive investment needs active management to dominate the price formation process and ensure the market functions as intended. Left to its own devices, cap-weighted indexation is prone to growing imbalances and risks, as momentum tendencies in markets become exaggerated. And it is flows, rather than the existing stock of assets, that determine how markets function. Markets dominated by active manager flows tend to be equilibrium seeking, as these managers buy cheap and sell expensive, pushing stocks towards intrinsic value.

When active manager trades no longer dominate flows (which historically tended to happen only at cycle extremes) markets change character and become deviation amplifying, with higher prices attracting more buying and lower prices more selling. This creates an unstable market, very dependent on continued liquidity flows. Stocks typically end up trading far above any valuation underpin and risk severe declines or crashes when the flow of liquidity slows or reverses.

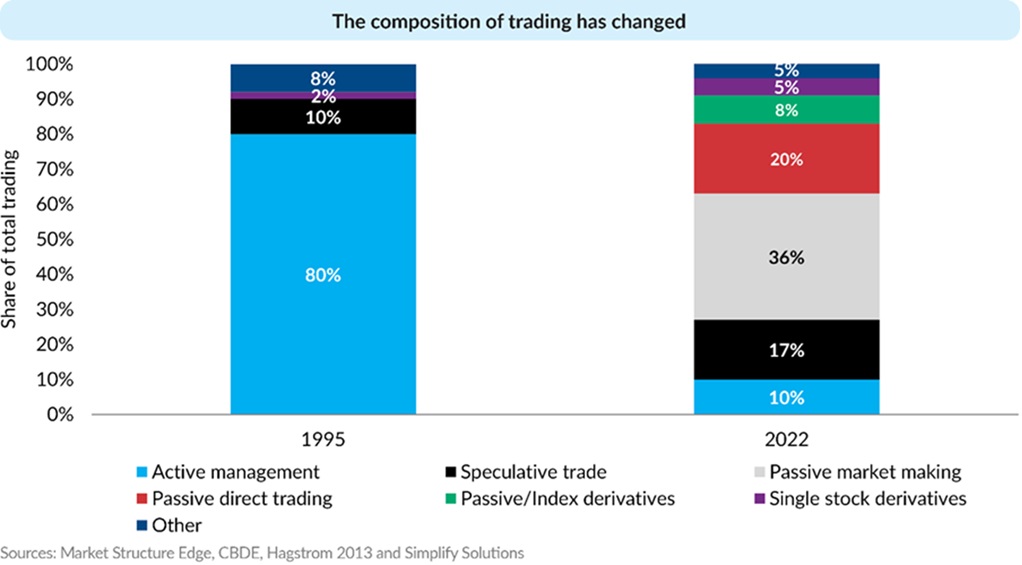

The chart below by Simplify Asset Management shows an estimate of the change in US equity trading by source. Simplify believes that active management-originated trades declined from some 80% of the total in 1995 to only 10% in 2022.

The implication is that periods of deviation amplification have become more prevalent and extended.

Could this be why the S&P 500 and MSCI World Indices are at record levels of concentration?

The top 10 companies account for 39% of the S&P 500 Index’s total market capitalisation. Of these, eight companies comprising 35.5% are broadly driven by the artificial intelligence (AI) theme (Nvidia, Microsoft, Apple, Amazon, Alphabet, Meta, Broadcom and Tesla). Over the past few years, the index has become more concentrated than ever. While the MSCI World Index in theory covers 1 320 companies across 23 countries, in practice it is no better than the S&P 500 Index. Its top 10 holdings are essentially the same as those of the S&P 500 Index and comprise 36% of the index, of which also eight companies totalling 33% are AI-themed.

Ignore the underlying assumptions at your peril

The industry tends to assume indices have certain characteristics that underpin their functionality and suitability for use in various models and risk measures. Given their widespread use, investment managers using quantitative risk models must ensure the six key embedded assumptions are well understood.

One key assumption is that the index displays stable statistical characteristics over time. Another is the assumption that returns are distributed predictably and can be modelled with known statistical properties. Neither of these are supported by actual market behaviour, meaning some scepticism regarding model outputs has always been important. Remarkably, many asset managers (and financial institutions generally) appear to blindly manage to model-derived risk constraints despite this.

What has changed now is that the dramatic increase in index concentration to record levels tests the validity of three of the last four key assumptions that underpin their use. These include: that the index is representative of the market, that it’s constituents’ prices are set efficiently by active market participants and reflect risk accurately, that it provides sufficient diversification, and finally that its constituents are liquid and tradeable to allow portfolio adjustments to align with the index or hedge risks effectively.

The current levels of index concentration calls into question whether the S&P 500 Index and MSCI World Index are still effective benchmarks. This means passive investors are effectively taking very substantial idiosyncratic risk, and by implication, the output of most quantitative risk models using these benchmarks should at the very least be viewed with a common-sense overlay.

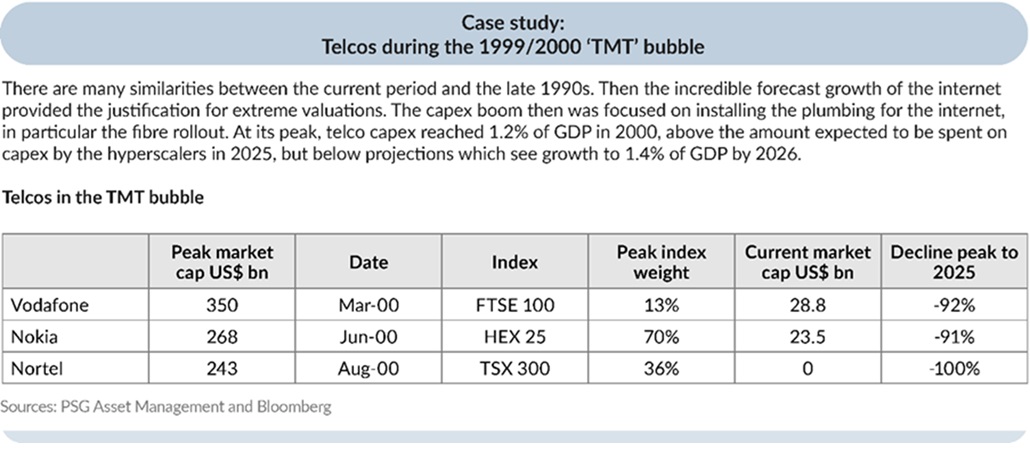

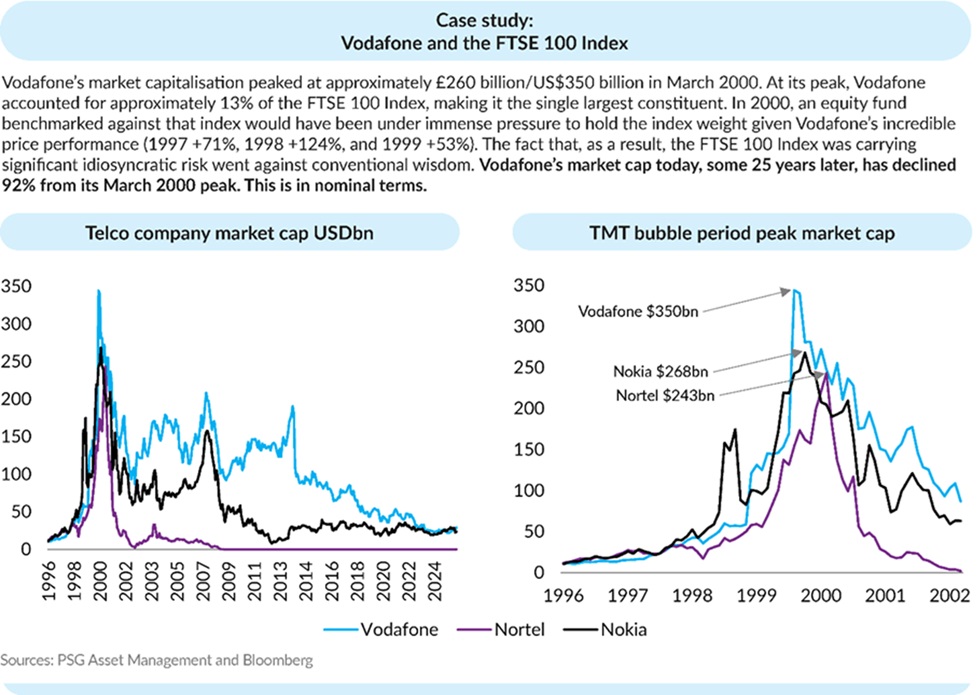

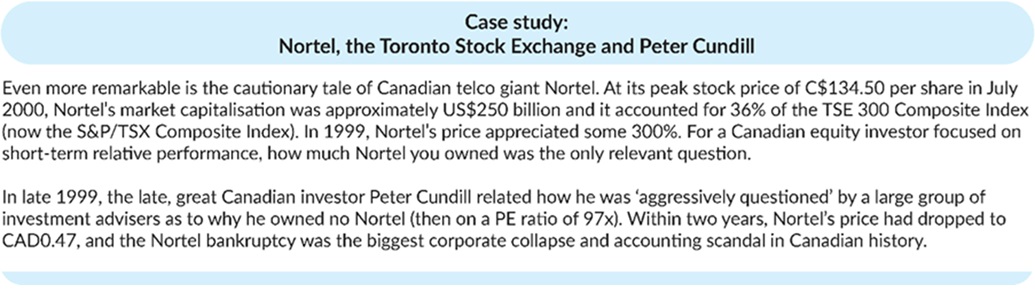

The importance of this is highlighted by our case study below, which focuses on a previous occasion when benchmark indices became overly concentrated.

How should investors respond?

Indices, as it turns out, are not infallible instruments, and hugging an index is not risk free. If your global equity investments are dominated by passive funds and ‘benchmark-hugging’ active mandates, consider looking for some true differentiation via products based on equal weight or fundamental indices, or active managers that are not as benchmark focused.

ENDS