Kevin Cousins, Head of Research at PSG Asset Management

Recent research by the IMF highlighted that global bonds have become less effective in mitigating volatility since the start of the Covid-19 pandemic. Traditionally, bonds have been seen as a key diversifier in the traditional 60/40 portfolio (60% equities, 40% bonds), with rises in bonds offsetting falls in equities. However, more recently bonds have started moving more in line with stocks, meaning that global bonds are no longer acting as effective equity hedges. Our own research in 2021 and early 2022 reached similar conclusions, and caused us to rethink the nature of safe-haven assets in our global portfolios.

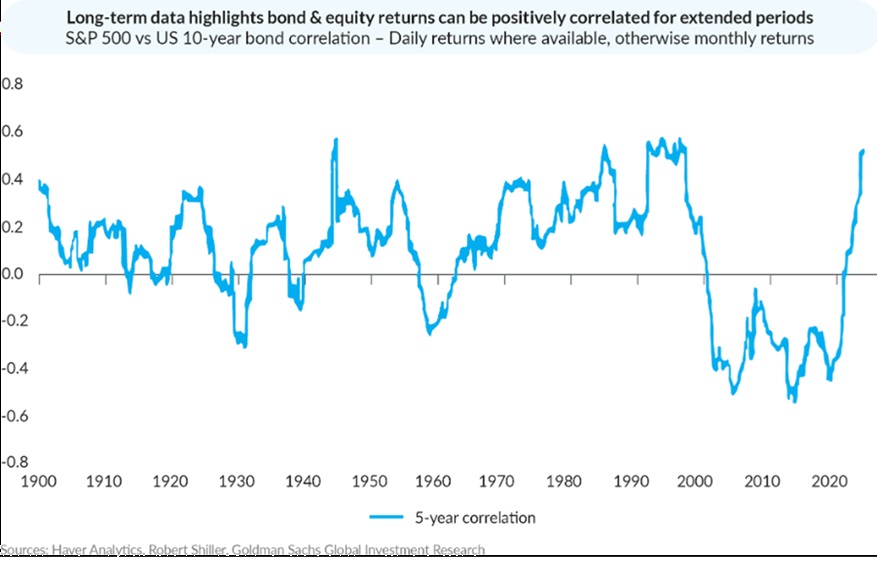

This may prove anathema to a whole generation of investors, who have grown up in a world where US long bonds were the exemplary safe-haven asset. However, a bit of historical perspective can be helpful. The popularity of US long-bonds as a portfolio diversifier were really cemented over the 40-year period from 1981 to 2021, when US bond yields trended downward. The annualised total return over this period was around 9%, compared to CPI averaging 2.8% per annum, resulting in strong real returns. Since the equity market crash in 1987, bonds have also displayed strongly uncorrelated performance when risk assets are sold off. This is driven by the so-called ‘Greenspan Put’, as investors anticipate monetary policy easing by the US Federal Reserve (Fed) in response to economic or market stress. When investors fear a looming recession, massive purchases of bonds take place as portfolios load up on ‘insurance’.

Most investors believed that the negative correlation between equities and bonds was just how markets worked, perhaps because it was the only environment they had experienced. Taking a longer-term view, it is clear that there have been long periods of positive correlation as markets experience a ‘supply-side’ regime. This is when growth declines are driven by supply-side shocks (such as the rise in energy prices, tariffs and trade wars or wage pressures) rather than demand-side shocks. Supply-side shocks are much more difficult for policymakers to deal with (they can’t just cut rates to solve the growth problem without triggering inflation) and hence both bonds and equities can drop together.

Given poor US fiscal discipline, a continued reliance on debt issuance, inflation that is still above the Fed’s 2% target rate, and the weaponisation of the USD, some of the key pillars that have supported US long-bonds’ safe-haven asset status have started to erode. This was evident in 2022 when as equity markets sold off, developed market long bonds, including US Treasuries, delivered their worst performance on record. Despite this the thinking that entrenches bonds as safe-haven assets is treated as foundational in the financial industry and is seldom questioned.

The breakdown in correlations generally has some material implications for investors. Most of the standard risk-management practices in finance rely on historic average correlations to construct well-diversified and optimised portfolios. The underlying assumption is that historic average correlations between assets correctly describe future correlations. However, in reality, correlations tend to rise sharply during periods of market turmoil. This wreaks havoc in multi-asset portfolios that have been quantitatively optimised based on historic average correlations.

Some quirks of the financial services industry amplify the impact of this reliance on historic data and tend to erode the efficacy of traditional safe-haven assets. Firstly, the whole industry uses similar quantitative risk models drawing on similar historical data, and they are all searching for ‘idiosyncratic’ positions that will enhance portfolio resilience. Markets are dynamic, and future returns are hugely influenced by position crowding and starting valuations. This means an asset that acted as a good hedge historically may no longer behave in an uncorrelated fashion during the next big market event if it is widely owned and expensively valued.

Secondly, many investment strategies today carry significant leverage. The hedge fund industry provides one good example, with leverage near all-time highs. This, together with client redemptions, increases the need for market participants to de-gear and sell holdings during market declines. If they have significant exposure to the popular ‘safe havens’, these assets will correlate with the collapsing market rather than act as a hedge.

In an increasingly fragmented world, in which inflation is likely to remain at elevated levels, the importance of constructing resilient portfolios cannot be underestimated. However, the approaches that served investors well in the past look increasingly unlikely to work in the future. US long bonds may not serve as reliable portfolio diversifiers and historic quantitative measures of price volatility calibrated during the secular stagnation period may be poor guides to future price behaviour. We believe constructing our portfolios with securities that are uncrowded and cheap relative to their histories is a good starting point when building resilience. In addition, the use of portfolio hedging plays an important role in ensuring we can carry enough risk assets to meet our clients long-term return objectives and can still weather periods of market turmoil. Finally, the energy and gold sectors, (despite the latter’s strong run in 2024 and 2025), have embedded optionality to the price spikes that typify geopolitical upheavals. Recent events provide an important reminder of how the crucial role thoughtful portfolio construction and diversification is likely to play in portfolios in the future.

ENDS