Lyle Sankar, Head of Fixed Income at PSG Asset Management

Elevated interest rates over the past few years have meant that investors have enjoyed attractive returns from cash investments, deposits and fixed income funds. However, your selection of income options is more important now than ever with the South African Reserve Bank (SARB) poised to start a rate cutting cycle. The returns on offer from these investments will soon deviate significantly as rates on lowest risk investments (cash, money market and short-term fixed deposits) will move lower in lockstep with the repo rate. The good news is that investors still have the opportunity to benefit, provided that they position their portfolios to capitalise on the opportunities available in the market.

How investing in longer-dated bonds creates the opportunity to lock in yields

Funds with the ability to access longer-dated fixed income instruments, like income and multi-asset income funds, have the ability to take advantage of higher starting yields in nominal and inflation-linked bonds. South Africa’s fixed income curve is upward sloping: the longer-dated the instrument, the higher the yield. When interest rates come down, nominal bonds are expected to continue to offer greater yields than cash, but also offer the prospect of capital gains, as instruments offering higher returns become more valuable when interest rates decrease. By positioning in these assets ahead of time, fund managers can extend the availability of higher yields for investors in their funds and cushion investors from rapid rate reductions.

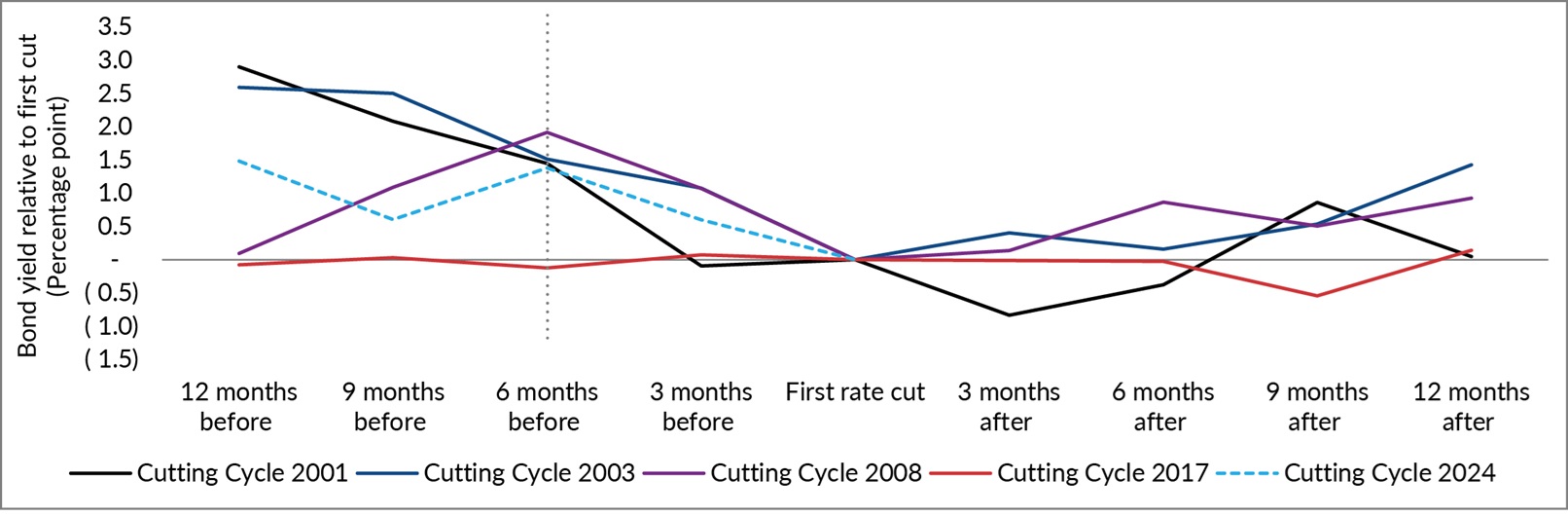

Markets however are forward looking, and bond investors have started positioning portfolios to take advantage of repo rate cuts. Analysis of previous rate cutting cycles indicate that the bond curve begins to rally (outperform) about six months in advance, with bond yields typically reducing by 1% to 1.5% across the yield curve. This means that investors who wait for actual rate cuts to progress before moving to fixed income funds with a longer tenor, can potentially miss out on an opportunity to participate in attractive returns.

Change in 10-year bond yield relative to first rate cut

Markets are forward looking

Sources: Bloomberg and PSG Asset Management

Is it already too late?

Given the above, it may seem paradoxical that we believe there is still scope for local investors to benefit from pending moves in fixed income markets. However, the key for why we think this, lies in the significant risk premium still embedded in our yield curves.

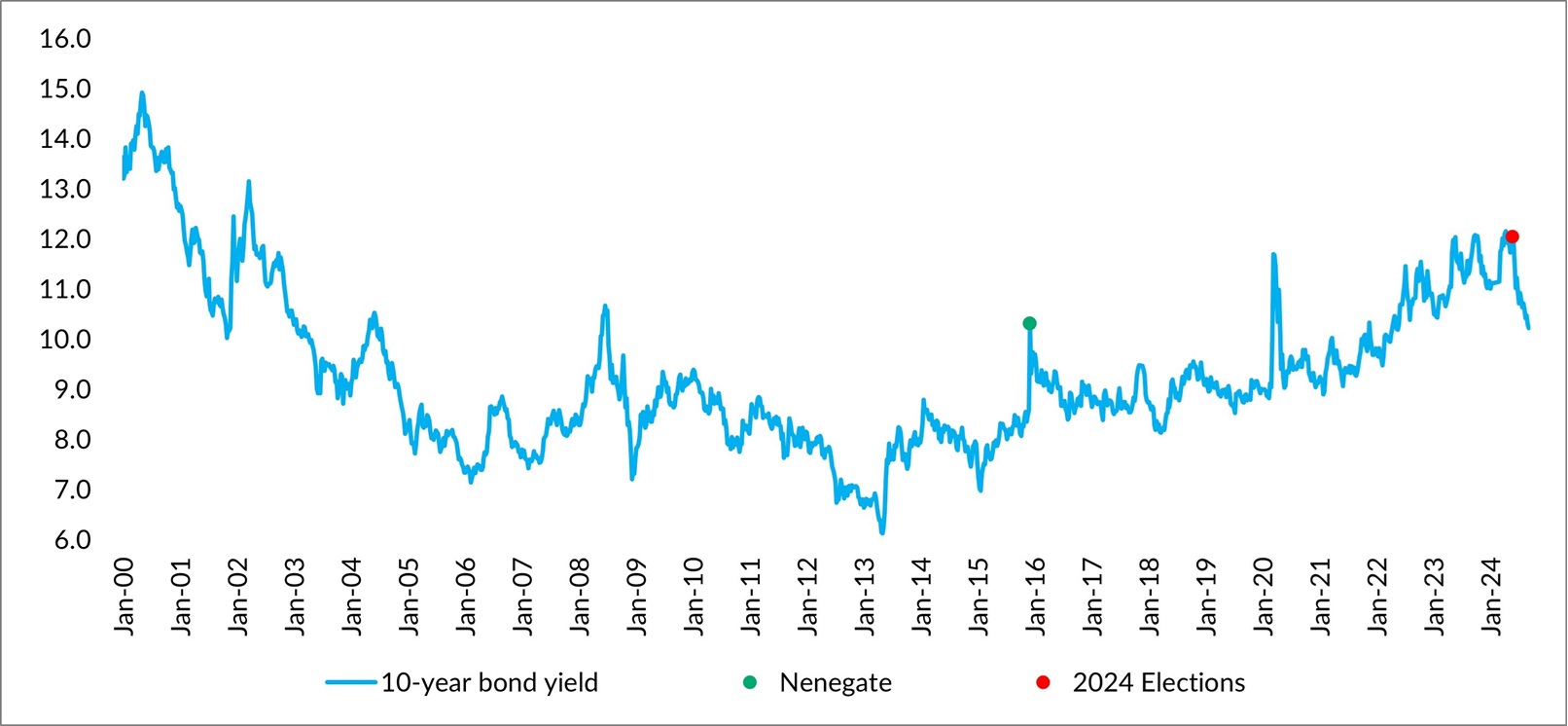

From 2005 to 2015, SA 10-year bond yields typically ranged between 8% and 9%. However, the Nenegate scandal sent bond yields climbing, and they have remained at elevated levels since. We have also seen increased volatility in government bond yields as confidence in Government ebbed and the country’s financial position eroded.

10-year bond yield

Sources: Bloomberg and PSG Asset Management

Although bond yields have retreated substantially from highs of over 12% ahead of the national election, we don’t view bonds as currently being expensive and believe substantial scope remains for yields to come down further in this asset class.

A reduced political premium and deeper-than-expected rate cuts bode well for investors

Post the outcome of the local election, political concern has subsided somewhat, and we believe this has been a partial driver of some of the repricing we have already seen in bond markets. In addition:

- An improved political environment has also supported the local currency. Since rand weakness feeds into the inflation loop, a stronger currency bodes well for the SARB’s ability to contain inflation further down the line.

- With central banks globally commencing cutting cycles, we expect the SARB to have room to cut interest rates in unison. Typically, when the Fed begins cutting, this could provide a further boost to ZAR strength since a weaker dollar tends to benefit emerging market performance.

- GDP forecasts remain subdued, but we see scope for outcomes surprising to the upside. Growth forecasts have not yet been adjusted upwards, and we have to ask what the potential for higher-than-expected growth rates are going forward. The continued absence of load shedding is likely to contribute to a more supportive environment for SA businesses and enhance consumer and business confidence. However, more importantly in our view, it provides an important insight into how relatively small improvements could potentially start moving the local economy out of the doldrums. Could transformation at Transnet be the next positive surprise to see the country’s economic growth rate move upwards?

Markets are only pricing in around 1.25% in rate cuts over the next twelve months, remaining tentative on the upside potential for rate cuts. However, considering the repo rate is well above expected inflation next year, the window for the SARB could potentially be wider. This means that substantial scope remains for bond yields to strengthen, and that investors who position early into this asset class could benefit from these positive movements.

ENDS