Herman van Papendorp, Head of Investment Research & Asset Allocation and Sanisha Packirisamy, Economist at Momentum Investments

Economies at a Glance by Momentum Investments’ macro research team consists of an easy-to-read chartbook of what is happening in the economy and a snapshot of the index returns for the month.

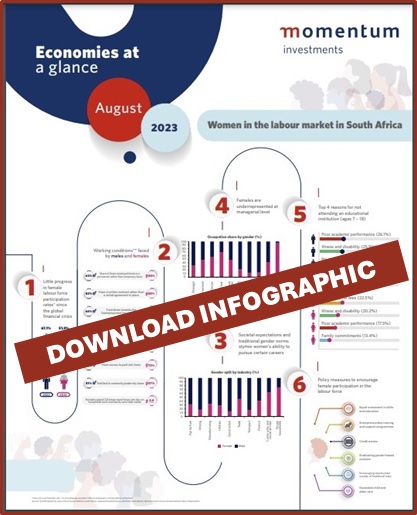

This month’s infographic features women in the South African labour market with a focus on the relatively flat growth rate in female labour force participation rates, working conditions, skewed gender representation on a sectoral basis given societal expectations and traditional gender norms, reasons holding back young females from completing their schooling and potential policy measures to encourage a higher level of participation in the labour market.

Below is a short summary of what is happening in the world’s largest economies:

Unites States

At the annual Jackson Hole Symposium, Federal Reserve (Fed) Chair Jerome Powell noted that though inflation had moved lower from its peak, it remained unacceptably high. He affirmed the Fed’s readiness to raise rates further if necessary and committed to maintaining tight monetary policy until inflation exhibited a sustained move lower toward the central bank’s 2% target.

Eurozone

Germany is once again wearing the mantle of the ‘sick man of Europe,’ a sobriquet it first bore in the late 1990s. According to the International Monetary Fund, Germany stands alone among major advanced economies in facing contraction this year. The industrial sector continues to grapple with feeble activity, while exports have underperformed. Unlike in the late 1990s, today’s Germany enjoys a lower unemployment rate of 3% and is a more open economy.

United Kingdom

The Confederation of British Industry’s monthly retail sales balance, comparing year-on-year volumes, plummeted from negative 25 in July to negative 44 in August, signifying a concerning contraction in the retail sector. However, there’s a glimmer of optimism in the form of the GfK’s Consumer Confidence Index, which climbed five points to register at negative 25 in August.

Japan

Japanese growth surprised positively at 1.5% in quarterly terms for the second quarter of the year thanks to robust auto exports and a rise in tourist arrivals. Although external demand added a firm 1.8% to quarterly growth output, domestic demand detracted 0.3%. Private consumption contracted by 0.5% during the quarter, a consequence of elevated inflation impacting the sales of food and household appliances.

China

Weak confidence, geopolitical tensions, an ageing population, negative headline inflation, burgeoning debt and a troubled real estate market have raised the spectre of a balance sheet recession, where real debt escalates due to deflation, triggering defaults amid moribund economic growth. However, signs of resilience persist.

Emerging markets

Despite expectations for a more aggressive positioning of the BRICS grouping in opposition to the Group of Seven (G7) countries, the annual BRICS summit instead focused on enhancing cooperation between its members. Cooperation agreements spanning space, education and health were raised, while commitments were made to promote cross-border trade and financial flows within the bloc.

South Africa

Inflation cooled by more than expected in the July figures from Statistics South Africa (SA). The headline figure, registering at 4.7% in year-on-year terms, marked a notable decline from the previous month’s 5.4%. This pronounced drop was largely owing to a fall in food inflation to below 10%, alongside the transport category, which dipped into deflation. Softer-than expected core inflation figures offer some relief amid concerns of broadening inflation pressures exacerbated by a weakening currency and inflation expectations shifting beyond the midpoint of the 3% to 6% inflation target.

Download the infographic – click below…

ENDS

Author

@Herman van Papendorp, Momentum Investments

-

@Herman van Papendorp, Momentum Investments

-

@Herman van Papendorp, Momentum Investments

-

@Herman van Papendorp, Momentum Investments

-

@Herman van Papendorp, Momentum Investments

-

@Herman van Papendorp, Momentum Investments

-

@Herman van Papendorp, Momentum Investments

-

@Herman van Papendorp, Momentum Investments

-

@Herman van Papendorp, Momentum Investments

-

@Herman van Papendorp, Momentum Investments

-

@Herman van Papendorp, Momentum Investments

-

@Herman van Papendorp, Momentum Investments

-

@Herman van Papendorp, Momentum Investments

-

@Herman van Papendorp, Momentum Investments

-

@Herman van Papendorp, Momentum Investments

-

@Herman van Papendorp, Momentum Investments

-

@Herman van Papendorp, Momentum Investments

-

@Herman van Papendorp, Momentum Investments

-

@Herman van Papendorp, Momentum Investments

-

@Herman van Papendorp, Momentum Investments

-

@Herman van Papendorp, Momentum Investments

-

@Herman van Papendorp, Momentum Investments

-

@Herman van Papendorp, Momentum Investments

-

@Herman van Papendorp, Momentum Investments

-

@Herman van Papendorp, Momentum Investments

-

@Herman van Papendorp, Momentum Investments

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments