Helen Littlewood, Sygnia Umbrella Retirement Fund Head of Product at Sygnia

This document provides an overview of changes proposed in the 2025 national Budget that are relevant to retirement funds.

Background

Finance Minister Enoch Godongwana’s first Budget presentation of the Government of National Unity (GNU), originally scheduled for 19 February 2025, was postponed to 12 March 2025 after the GNU cabinet disagreed over a proposed VAT increase from 15% to 17%. Although a Cabinet meeting held on 5 February 2025 agreed that VAT would have to be increased, the percentage by which it was to be increased was not agreed upon. This was the first postponement of the Budget since 1994.

On 12 March 2025, the Minister faced the unenviable task of trying to balance economic growth with such realities as: the needs of the millions of people who depend on a state income; the higher than budgeted 5.5% increase in civil servant salaries and state-owned enterprises such as Eskom as well as an increasing number of municipalities not being able to meet their financial obligations. All this within the framework of limited resources and amidst opposition to tax increases. The Minister confirmed that over the medium term, government will focus on investing in strategic infrastructure investment, job creation and maintaining a growth-friendly fiscal policy.

Personal impact

Income tax

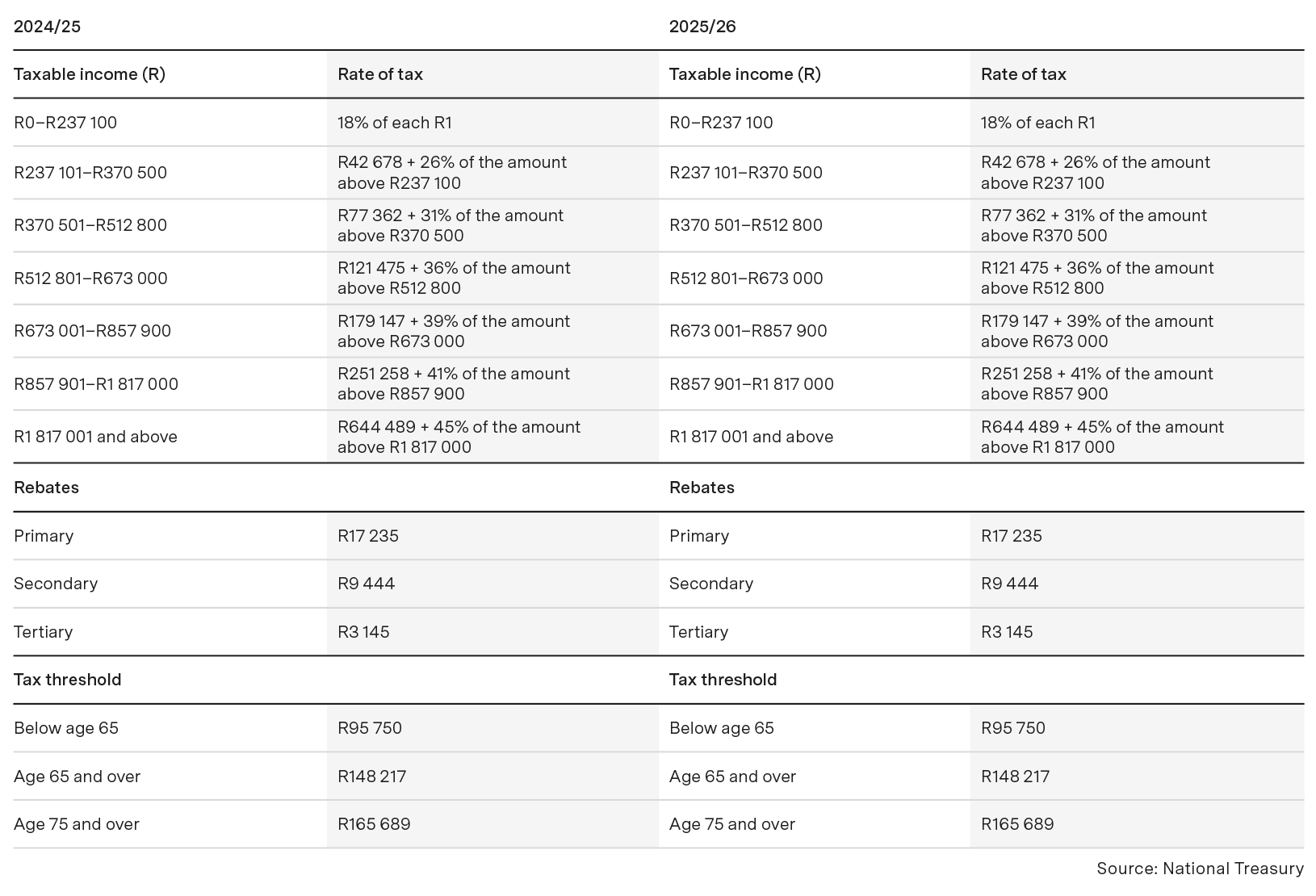

For the second year in a row, the income tax table for individuals and trusts has not been adjusted. This paves the way for bracket creep – increased tax liability as a result of higher income.

This bracket creep will have a negative impact on retirement fund members who received an increase that pushed them into a higher tax bracket. For example, a member who earned R237 000 per annum in 2024 would have paid personal income tax of R42 660 on that income, leaving them with R194 340 in pocket. If that member received a 5% increase in 2025, their income of R248 850 would now put them into the next tax bracket. If the total tax of R45 773 payable on this income is deducted, they are left with R203 077, an effective increase of around 4.5% on their take-home pay.

For the second year in a row, the tax rebates have also not been changed.

The tax table for individuals and trusts for 2025/2026 is as follows (the 2024/2025 table is included for comparison).

VAT

The proposal to increase value-added tax (VAT) by 0.5% in 2025/26 and by another 0.5% in 2026/27 to bring VAT to 16% in 2026/27 did not come as a surprise. The Minister announced an expansion of the basket of goods that are zero-rated for VAT purposes to include more items consumed by low-income households, such as canned vegetables, dairy liquid blends, and organ meats from sheep, poultry and other animals.

Social security grants

Due to the lower than initially budgeted VAT increases, the increases in the social security grants have been adjusted upwards at a lower percentage than expected. The grants will increase as follows from April 2025:

- Old age grant, disability grant and care dependency grant increase by R130 (5.9%) to R2 315 (from R2 185).

- War veterans grant increases by R130 (5.9%) to R2 335 (from R2 205).

- Child support grant and grant-in-aid grant increase by R30 (5.9%) to R560 (from R530).

- Foster care grant increases by R70 (5.7%) to R1 250 (from R1 180).

The Covid-19 social relief of distress (SRD) grant increases to R370 (from R350) per month per beneficiary, including administration costs, and will continue to be paid until the end of March 2026.

Medical tax credits

There were no inflation adjustments to medical tax credits. The current tax credit of R364 of the monthly contributions to a medical scheme for each of the first two persons covered by the medical scheme and R246 for each additional dependent will still be available to the contribution payer.

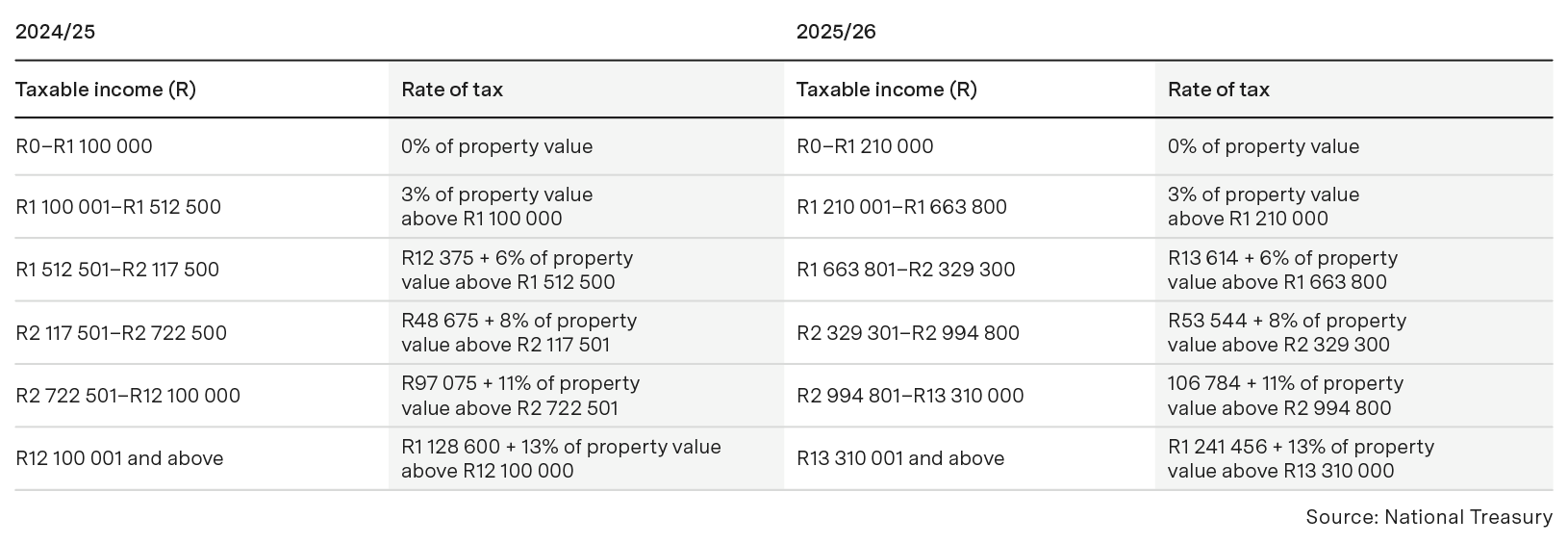

Transfer duty

The transfer duty brackets will be adjusted by 10% to compensate for inflation. The proposed transfer duty table effective from 1 April 2025 is as follows:

Fuel levy

There will be no changes to the fuel levy.

Carbon fuel levy

From 2 April 2025, this levy will increase by 3c per litre:

- to 14c per litre for petrol; and

- to 17c per litre for diesel

as required under the Carbon Tax Act.

Sin tax – alcohol and tobacco

The Budget stated that excise duties on alcohol and tobacco products will be adjusted above the expected inflation rate.

The proposed increases are as follows:

- Spirits, wine, beer, pipe tobacco and cigars will all increase by 6.75% from 1 April 2025. However, traditional African beer will remain unchanged.

- tobacco, cigarettes, cigarette tobacco and electronic nicotine and non-nicotine delivery systems (“vaping”): increase of 4.75%

Retirement fund impact

Contributions

The tax-deductible limit for contributions has not been adjusted. The 2025 Budget tax guide confirms that the contribution that may be deducted in a year of assessment is still limited to 27.5% of the greater of the amount of remuneration for employees’ tax purposes or taxable income (both excluding retirement fund lump sums and severance benefits). The deduction is further limited to the lower of R350 000 or 27.5% of taxable income before the inclusion of a taxable capital gain.

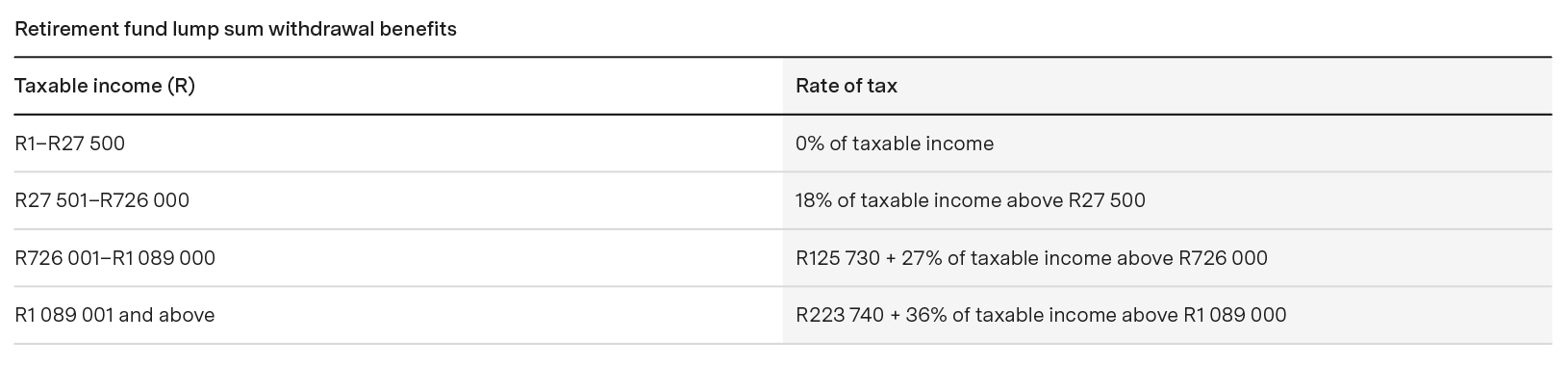

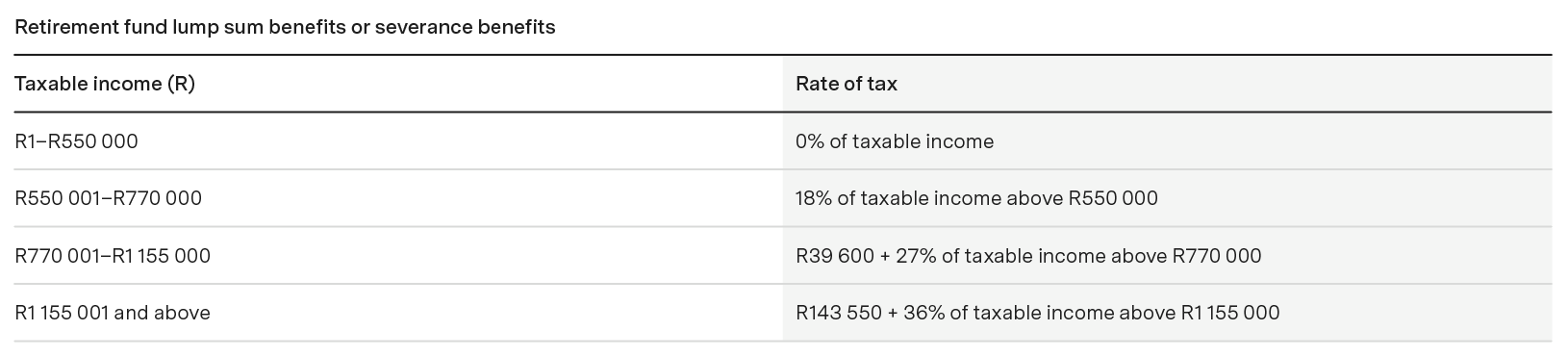

Tax tables

The tables that must be used to determine the tax payable on retirement fund lump sum benefits and retirement fund lump sum withdrawal benefits have also not been adjusted. The following tables still apply:

Access to retirement component on retrenchment

A member who is retrenched may currently only access their vested component and, subject to certain requirements, their savings component. A retirement component may be transferred to another fund but may only be accessed on retirement.

Allowing limited access to the retirement component on retrenchment is part of the second phase of the two-pot system. Government has started work and discussions on the restructuring of the two-pot system to allow a retrenched member who is in financial distress to get some access to their retirement component, subject to strict conditions.

Cross-border tax treatment of retirement funds

The lump sum and annuity payments from a foreign fund are exempt from taxation in South Africa for a member who was previously employed outside of South Africa and was a member of a foreign retirement fund. If those payments are also not taxed in the foreign retirement fund’s country, the member may end up not paying any tax at all on those benefits. A proposal has been made to change the rules around this so that South Africa has the taxing right under a tax treaty.

Technical amendments related to retirement funds

Divorce order deductions relating to marriages in accordance with religious tenets

Paragraph 2(1)(b)(iA) of the second schedule to the Income Tax Act will be amended to align with the change to the Pension Funds Act No. 14 of 1956, which became effective from 1 September 2024.

This will allow a fund to deduct the portion of a member’s pension interest awarded in a divorce order from the member’s individual account or minimum individual reserve in the fund when the parties were married in accordance with religious tenets.

Payment of death benefits from the savings component

The definition of “savings component” in the Income Tax Act will be amended to allow a beneficiary of a death benefit to receive the deceased member’s total benefit in the fund, including the savings component, as a lump sum, taxable in accordance with the retirement benefit lump sum tax table.

Other proposed amendments

Child maintenance payments funded from after-tax income

Where maintenance to a child is paid from after-tax income, the maintenance is currently taxed as income in the hands of the recipient. To better align with government’s social policy objectives, it has been proposed that these payments be excluded from the recipient’s taxable income.

Revenue Laws Amendment Bill (RLAB)

The RLAB was also released on 12 May 2025 and proposes technical amendments to, among other things, the two-pot system. We will provide further information once the RLAB has been distributed for further comment and is closer to finalisation/enactment.

ENDS