Rob Southey, Head: Asset Consulting at Momentum Corporate

Members retiring at the end of March 2026 would have seen a difficult short-term result in their market-linked investments. A typical conservative investment portfolio decreased by about 4,1% (source: Morningstar) during the month. This was mainly due to declines across most asset classes, including bonds, which lost value as interest rates increased.

While it can be worrying to see negative returns just before retirement, it’s important to understand that higher interest rates also improve the pricing of life annuities (a guaranteed pension for life) over the same period.

What happened to interest rates in March 2026?

During March 2026, long-term interest rates in South Africa increased significantly. For example, the yield on the 10-year government bond rose from about 8,1% at the start of the month to around 8,9% by the end.

When interest rates rise, bond prices fall. This is why the portfolio delivered a negative return for the month. But there is a positive side to this. Higher interest rates also mean that life annuities become more affordable, allowing members to secure a higher guaranteed income at retirement for the same amount of savings.

Why higher interest rates can be good for members’ retirement income

Life annuities are mainly priced on long-term interest rates. Insurers invest the members’ retirement savings in assets like government bonds. When interest rates are higher, these investments earn better returns.

This has two important benefits:

- Members need less money to buy the same level of guaranteed monthly income, or

- They can receive a higher monthly income from the same retirement savings

In practical terms, although investment markets fell during March 2026, the rise in long-term interest rates actually improved how much income members’ retirement savings could buy. In other words, life annuities became better value, which helped offset the impact of the short-term investment losses.

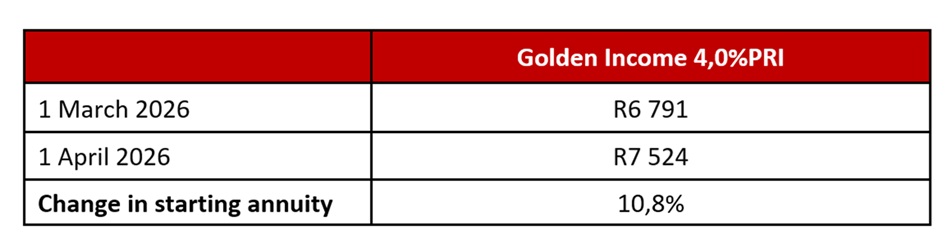

Illustration

To illustrate this, this table shows the monthly pension a 65-year-old could buy with R1 million at the beginning and end of March 2026. We’ve used the Momentum Golden Income 4% PRI annuity as an example, but the same principle applies to other life annuities.

At the beginning of March 2026, R1 million could buy a monthly pension of R6 791. By the end of the month, this had increased to R7 524 — an improvement of R733 per month.

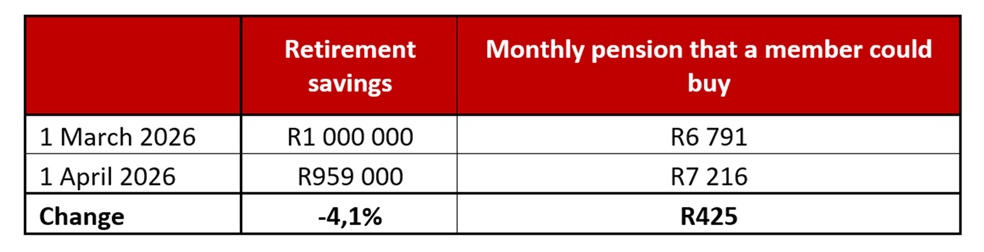

Consider the following example where a member started March 2026 with retirement savings of R1m. Note the actual monthly pension the member could buy at each of the two dates.

Because the investment return was -4,1%, the retirement savings would have decreased to R959 000 by the end of March 2026. But the monthly pension that could be bought at that point was R7 216 — which is R425 more than at the beginning of the month.

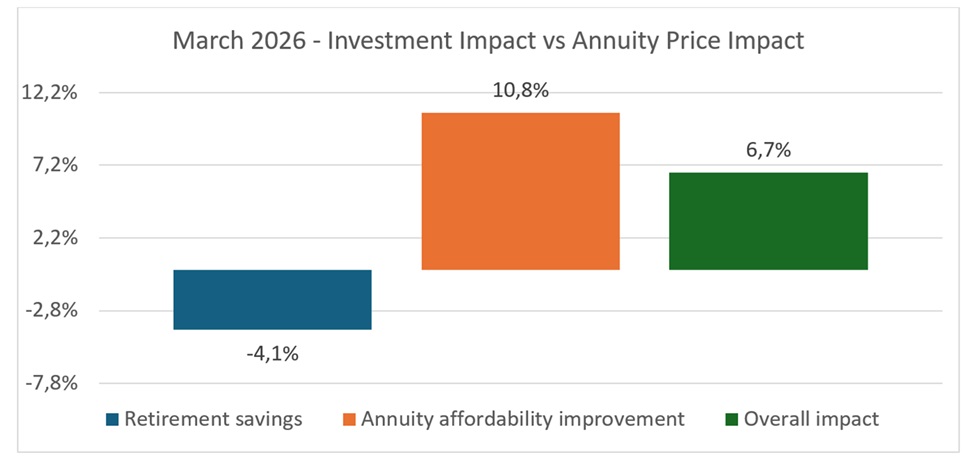

Although investments fell by 4,1% in March 2026, the rise in long-term interest rates made life annuities about 10,8% more affordable. This means the improvement in annuity pricing was greater than the investment loss by roughly 6,7%.

Key takeaway for retiring members

Short-term investment returns are important, but they shouldn’t be looked at on their own. When interest rates are higher, like in March 2026, life annuities become better value. This means members can secure a guaranteed retirement income on more favourable terms, even if markets have been volatile. For members considering a life annuity, higher interest rates can help improve their retirement income, even during periods when investment returns are weak.

ENDS