Kyle Hulett, Co-Head: Investments at Sygnia

Markets broke to new highs last week, driven by two reinforcing forces: geopolitical de-escalation and strong momentum in artificial intelligence (AI). The key catalysts both occurred on 7 April, when the US announced a ceasefire in the Middle East and Anthropic unveiled its latest model, Mythos, reigniting investor appetite for AI-related themes. The strength within the theme has been strik ing – 74% of AI-related stocks have subsequently outperformed the broader market. Overall S&P 500 breadth has narrowed to just 26%, however – a dangerously low level. The divergence is telling: this is not a broad-based bull market but a theme-driven rally resting on a narrow and concentrated leadership base.

The fundamental backdrop supports the move. Anthropic’s revenue run rate has tripled year-to-date, and OpenAI’s upcoming Spud release is expected to demonstrate another significant improve ment in capability. Concerns about AI-induced job displacement, particularly in software engineering, appear to be easing for now, with hiring resuming across the industry. An Anthropic study found no statistically significant difference in unemployment changes between occupations most exposed to AI and those least exposed since the release of ChatGPT. This is significant, as job losses are the major risk associated with AI.

AI capital expenditure and technology spending more broadly are expected to remain a key driver of S&P 500 earnings this year. The tech sector has shown a stronger trajectory of cash flow than expected, supporting capex – the outlook for which is likely to be revised even higher in light of recent cybersecurity headlines. Mythos can apparently find and exploit previously unknown software bugs on its own, and Anthropic has consequently not made Mythos publicly available as yet. Many companies will have to spend significantly more to secure their systems in a post-Mythos world. Another possible implication is that Mythos’ efficiency may soften demand for data warehouse infrastructure and energy.

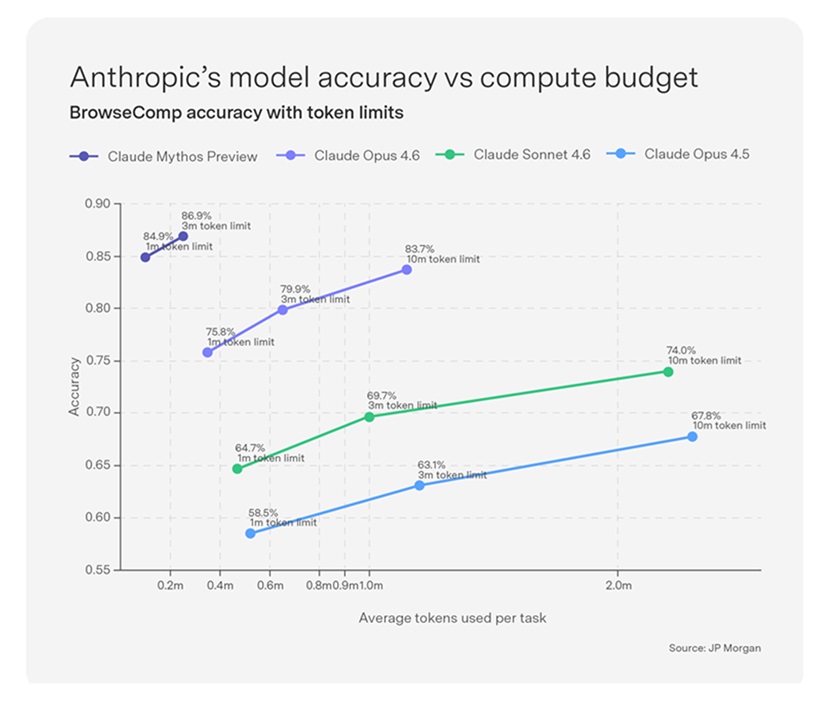

Claude Opus 4.5 was only released 6 months ago and Mythos needs a third of the tokens to generate vastly improved accuracy (see Chart). This and the fact that not every AI model will be a winner means that while there is a scramble for computing capacity now, there may be excess in the future.

Results announced last week highlighted AI’s momentum. Google rallied 4% on news that strong AI demand has boosted its cloud division, while Amazon rallied as its cloud unit posted its fastest growth in three years. Microsoft also reported strong growth in its cloud computing business, with revenue up 39%. However, Meta fell 6% on news it was increasing its capex on AI. Looking further ahead, we expect a broader range of companies to steer toward a meaningful productivity boom as AI adoption reduces marginal costs, expands output and raises real incomes, supporting the broader business cycle.

ENDS