Laura Marais, Cross Border Tax and Fiduciary Adviser; & Lieze-mari Brink, Cross Border Tax and Fiduciary Adviser; at Investec

Planning for retirement is one of the most important journeys you will ever embark on. Yet, for many people, even high‑earning professionals, the process can feel abstract, overwhelming or something to worry about “later.” The reality is that successful retirement preparation requires early action, continuous engagement and disciplined decision‑making across your entire financial life.

With that in mind, the questions such as “Where to start and how to plan?”, “What retirement savings vehicles to use?” and “What tax benefits are there?” are often asked. Let’s dive in and answer some of them.

1. How to start planning:

Have a vision: Every good retirement plan begins with a vision. You should consider what your day-to-day life will look like in retirement. Where will you live? What hobbies will you pursue? And so forth.

Calculate: From this vision, the next step is quantitative – calculate how much capital you require and how much you need to save today. The rule of thumb is that most South Africans need to save between 15% and 20% of their total remuneration for 30 to 40 years to achieve a 75% replacement value of their final salary.

However, this depends on a multitude of factors that can affect your plan, such as:

- When you start saving, whether in your 20s or in your 50s.

- Dipping into your savings via pre-retirement withdrawals.

- Incorrect asset allocation (too conservative for your age and retirement needs) and high fees.

Get advice: Engaging a qualified financial adviser is a critical and often overlooked step in developing a retirement strategy that aligns with your long‑term goals. Professional guidance ensures that your plan is tailored to your circumstances and adapts as your life and financial position evolve. Importantly, this is not a one-off exercise. Conducting an annual review of your retirement plan enables you to assess whether you remain on track and identify any adjustments needed to keep your savings strategy aligned with your objectives.

2. Investment vehicles to help you save for retirement

South Africa offers a robust and diversified landscape of retirement savings options. The primary pre‑retirement vehicles include pension funds, provident funds, pension and provident preservation funds, and retirement annuities (RAs). In addition to these formal retirement structures, individuals can further enhance their long‑term savings through complementary investment products such as tax‑free savings accounts (TFSAs) and other discretionary investment portfolios.

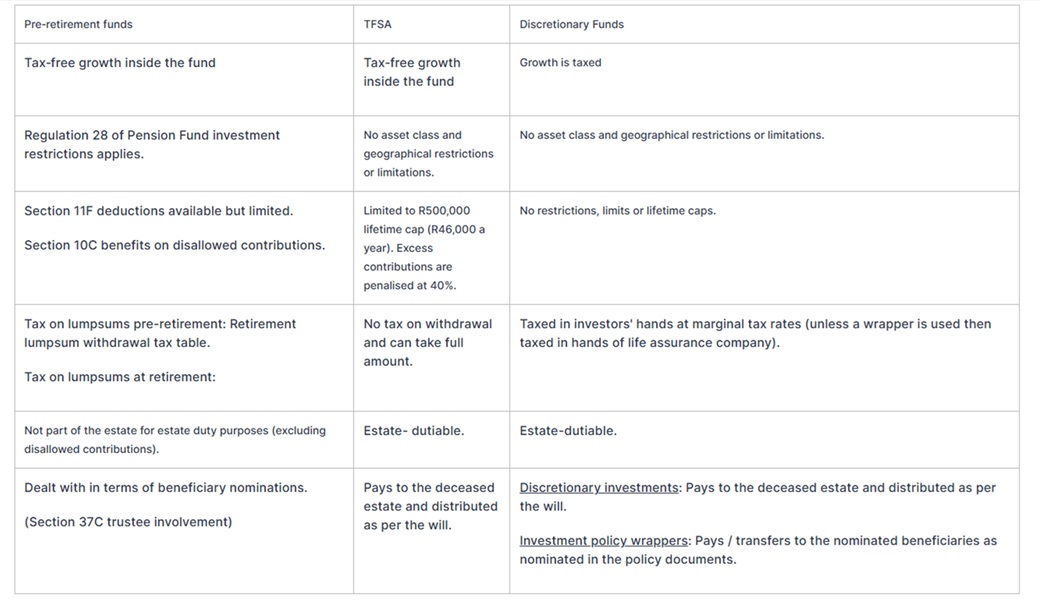

Pre-retirement funds:

These investment vehicles offer tax‑efficient growth, as returns within the fund are not subject to income tax, dividends tax, or capital gains tax. Importantly, these pre-retirement funds (excluding any disallowed contribution) are excluded from your estate for estate duty purposes. They also provide favourable tax treatment at retirement, together with two key tax incentives for investors while saving for retirement: deductions under section 11F of the Income Tax Act (ITA) for qualifying contributions, and exemptions under section 10C of the ITA for recognised over-contributions.

Section 11F of the ITA allows taxpayers to deduct pre-retirement contributions from their taxable income. The deduction is limited to the lesser of: R430,000 (previously R350,000) or 27.5% of the greater of remuneration or taxable income, including taxable capital gains or taxable income excluding taxable capital gains (i.e., “allowed contributions”).

If you over-contribute above the section 11F “allowed contribution”, the excess is known as a “disallowed contribution” with no immediate tax benefit. However, you don’t lose the tax benefit. Under the workings of section 10C of the ITA, the disallowed contribution can later be used to reduce tax on retirement lump sum withdrawals pre- or at retirement and/or annuity income drawn from post-retirement annuities. Disallowed contributions form part of the dutiable estate if paid to your beneficiary as a lump sum. However, if beneficiaries elect to receive the benefit as an annuity rather than a lump sum, those amounts are not subject to estate duty.

Other considerations to be mindful of regarding pre-retirement funds are:

Regulation 28 of the Pension Fund Act limits the exposure of the savings in the pre-retirement fund to certain asset classes. For example, in the pre-retirement fund, the maximum exposure to such equities is 75%, to property 25%, and to offshore assets 45%. Therefore, it imposes investment restrictions on your pre-retirement savings.

Section 37C of the Pension Fund Act governs the distribution of death benefits. It imposes a fiduciary duty on the trustees of a pre-retirement fund to ensure that the deceased’s dependants benefit from the fund’s savings. Therefore, the trustees can alter your beneficiary nominations and percentages to fulfil this fiduciary duty.

Tax-free savings account:

Once you have maximised your contributions to pre‑retirement investment vehicles, a TFSA becomes an excellent additional tool for long‑term retirement planning. A TFSA offers tax‑free investment growth; however, contributions are limited to R46,000 per tax year and a lifetime cap of R500,000. Because any capital withdrawal permanently reduces your remaining lifetime limit, a TFSA is best suited for long-term compounding investments rather than a short-term savings account. It is also important to note that TFSAs form part of the estate for estate duty purposes and are distributed in accordance with your will.

Discretionary funds:

The third category is discretionary investments, which includes unit trusts, direct equities, exchange‑traded funds, property investments and investment policy “wrappers”. Incorporating discretionary funds into your retirement plan offers several advantages:

- Unlimited contribution capacity, unlike TFSAs.

- No Regulation 28 constraints, providing full investment flexibility.

- Enhanced diversification, as you have complete discretion over asset allocation.

However, investment growth in discretionary funds is taxable as capital gains tax, while dividends tax and income tax may apply. These assets form part of the dutiable estate on death. Generally, your discretionary assets are dealt with in terms of your will. Should you have invested through an investment policy wrapper, your beneficiary nominations will be adhered to upon your passing. Only in the event of no beneficiary being nominated on the policy, will this wrapper be dealt with in terms of your will.

While discretionary investments do not offer the tax advantages associated with pre-retirement funds and TFSAs, they provide valuable liquidity and flexibility at retirement, making them an important component of a well‑balanced retirement strategy.

3. Comparison of the tax benefits of each investment vehicle

Source: Investec Wealth & Investment International, April 2026

Retirement planning is not a one-off event. It’s a continuous process requiring adjustments as life and family circumstances change and career progression occurs. Changes in tax legislation, investment performance and other legislative reforms all influence your plan. By understanding how the various tax rules, investment vehicles and behavioural factors interact, you can build a retirement strategy that is robust, sustainable, and aligned with the life they aspire to live.

ENDS