George Brown, Senior US Economist at Schroders

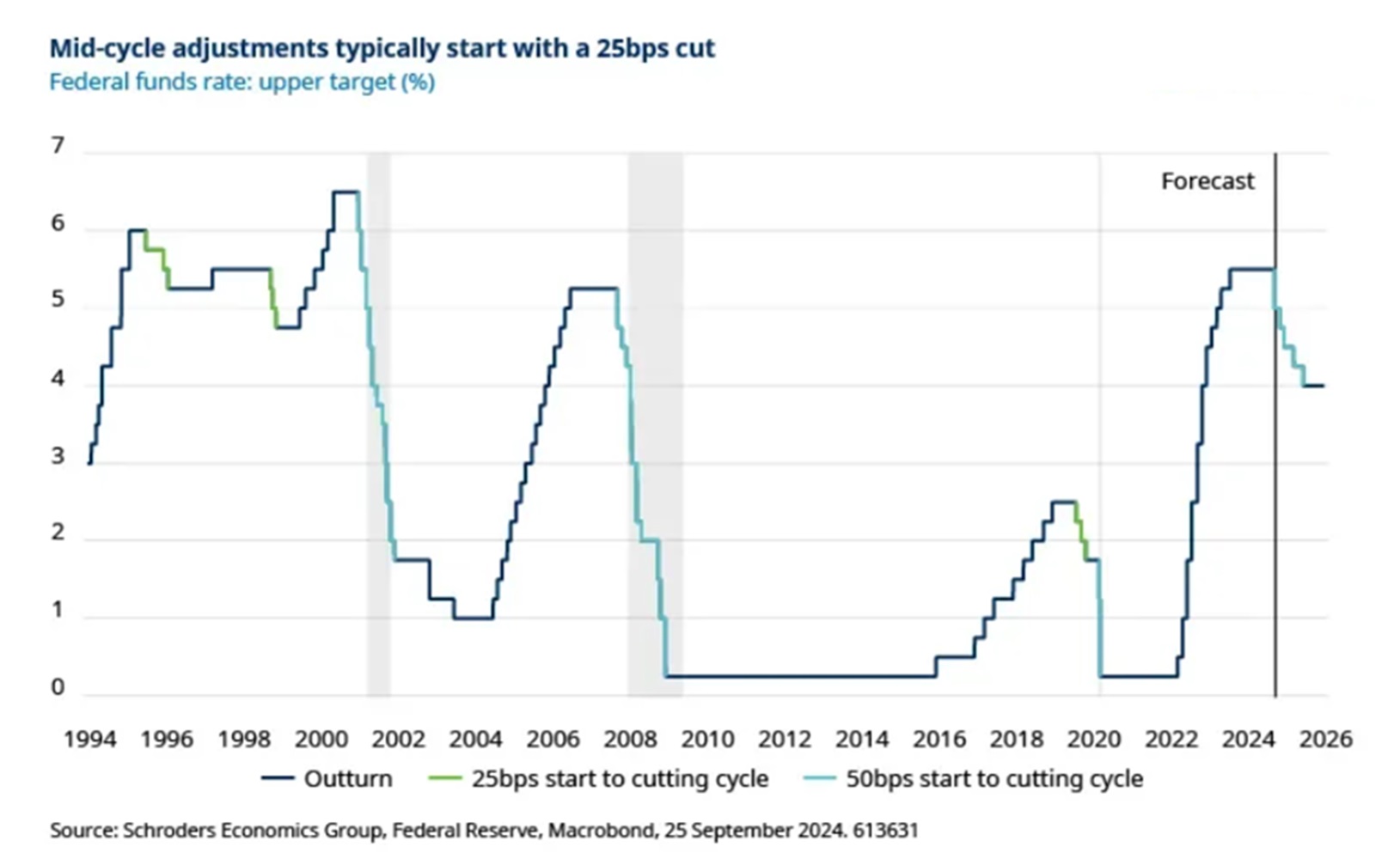

When the Federal Reserve (Fed) kicks off a cutting cycle with a 50 basis points (bps) reduction, it is typically a cause for concern. It did so in January 2001 and September 2007, just three to four months before the US economy tipped into recession, as well as in March 2020 at the start of the global pandemic. Because of the optics of such a move, we had assumed that the central bank would borrow from the playbook of the mid-cycle adjustments of 1995, 1998 and 2019. On those three occasions, a slowdown in growth (rather than a recession) prompted the Fed to start cutting with a conventional 25 bps reduction.

However, the Federal Open Market Committee (FOMC) opted for a more aggressive 50 bps cut, against the expectation of ourselves and 91 of the other 100 economists polled by Reuters. Chair Jerome Powell sought to frame this as a “re-calibration” in his press conference, with no fewer than nine related mentions, while also stressing that monetary policy works with long and variable lags. This is fedspeak for saying rates are too restrictive for where we are in the economic cycle and that the bank wants to get back to the neutral rate as fast as feasibly possible.

While we can see the logic of Powell’s reasoning, we don’t believe that such an aggressive pace of easing is warranted. Neutral is an imprecise concept, not a measurable number but a theoretical interest rate deemed neither too restrictive, nor too loose in order for growth and inflation to settle back onto steady and predictable paths. But if an aggressive rate-cutting cycle comes to pass and at the same time the US economy proves more resilient than Fed policymakers anticipate, US interest rates could end up too loose. They risk undershooting neutral and re-igniting the dying inflationary embers.

Governor Michelle Bowman, who favoured a 25 bps reduction at September’s meeting, seems to share our reservations. She argued that the labour market remains near full employment, with recent weakness being clouded by measurement issues and uncertainty surrounding immigration. And that while inflation has moderated meaningfully, she believes it would be premature to declare victory, such that it would be better to move at a measured pace to avoid unnecessarily stoking demand.

But Bowman is evidently in the minority, with the “dot plot” of FOMC members’ rate forecasts for end 2024 now pointing to another 50 bps of easing by year-end from the current fed funds range of 5.00-4.75%. While we judge this to be excessive, we know better than to fight the Fed. And so, we now expect them to cut rates by 25 bps in both November and December, having formerly expected them to only deliver the latter. Taken alongside September’s jumbo cut, this is some 50 bps more easing than we previously expected, which will also prompt an upgrade to our already above-consensus growth forecast of 2.1% for 2025.

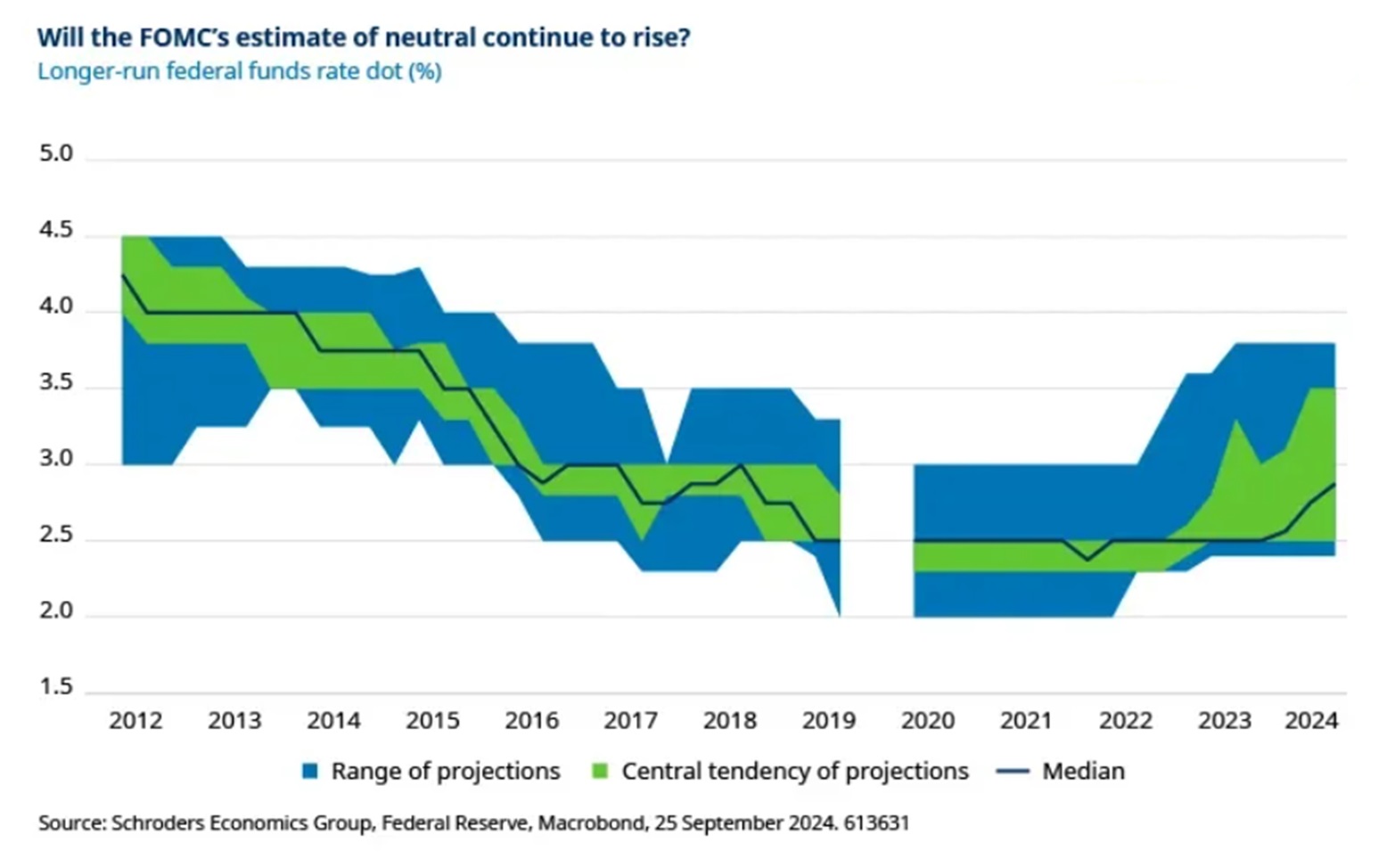

Even so, we doubt the Fed will ease another 100 bps next year, as suggested by the dot plot. We don’t believe this trajectory will transpire given the uncertainty evident both in the wide range of forecasts among the 19 FOMC members and in external forecasts as to where the neutral rate lies. The committee’s own estimate of where neutral lies can be implied by the median of its members’ “longer run” dot plot, which is currently about 2.875%, some 200 bps lower than the current range. This implied neutral has, however, risen at each meeting this year after having languished at 2.5% for much of 2019 to 2023 (see chart below; in March 2020, the FOMC did not release a projection because of the pandemic). And so, if a more optimistic outlook for the US economy comes to pass, it is reasonable to assume the median dot could rise further still.

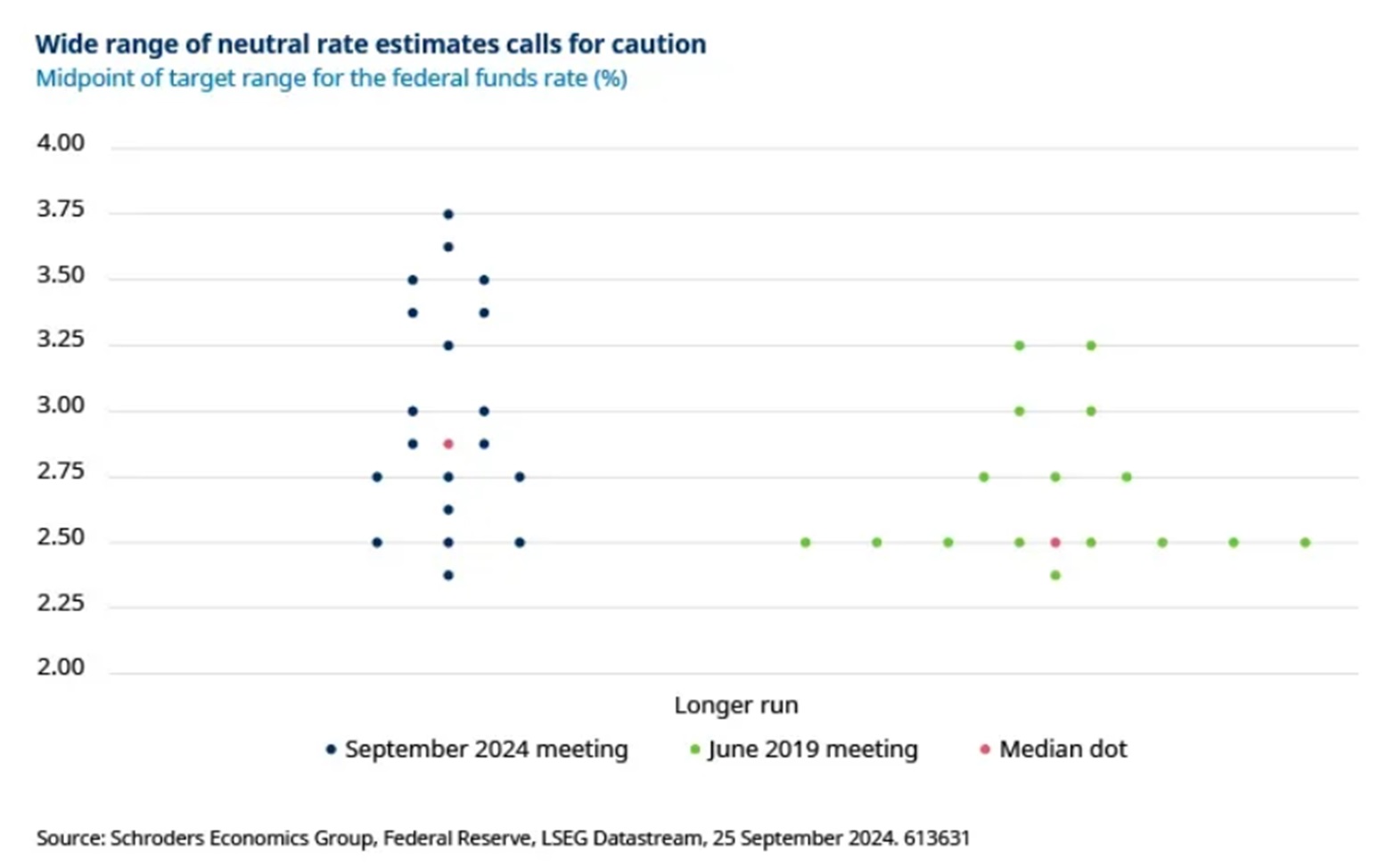

As an illustrative exercise, extrapolating the trajectory of the median longer run dot since the end of 2023 would put the neutral rate on course to be 3.5% in a year’s time. This would bring it broadly in line with our own estimate of the neutral rate. Regardless, the uncertainty about where neutral lies is the more significant point. As already mentioned, the empirical estimates of neutral vary enormously and this extends to the committee as well, with one FOMC member estimating it to be as low as 2.375%, whilst another believes it is as high as 3.75%.

This is in stark contrast to the divergence between members when the Fed implemented its last mid-cycle adjustment in 2019. At that time half the committee’s dots implied that the neutral rate was 2.5% and only two members thought it was higher than 3%. Powell acknowledged that there is more ambiguity about the neutral rate than there has been in the past, twice saying in his press conference that the committee will “know it by its works”. In other words, they are unsure how much they need to ease and will rely on the data to determine when they have reached neutral.

To our minds, there is a greater risk of inadvertently undershooting the neutral rate than overshooting it. This calls for a more measured pace of easing than currently envisaged in the dot plot. As such, our expectation remains that the committee will deliver 25 bps rate cuts in both March and June next year before pausing to take stock of the 150 bps of cumulative easing it will have delivered by then. Providing inflation subsequently remains contained, this ought to open the door to further modest easing in 2026.

Nevertheless, the risk to our rate forecast is clearly to the downside. It is unclear whether the market pushed the Fed into cutting rates by 50 bps in September, but if so, the committee should not make a habit of it. Our latest forecasts included an “aggressive rate cuts” scenario, under which jitters about the growth outlook convinces the committee to deliver the aggressive rate cuts priced into markets. Our view is that this would ultimately cause inflation to re-accelerate and prompt the FOMC to have to start hiking again. And so, our message to the Fed is simple: keep at it until the job is done.

ENDS