Daniel Mulugeta, Research Analyst; Luke Dawson, Research Analyst; and Charlie de La Pasture, Fund Manager, at High Street Asset Management

The Good: Navigating a Strait of Uncertainty

Global markets have quickly been swept up in the disruptive effects of the US and Israel’s offensive on Iran. The most affected were Iran’s Middle Eastern neighbours, as Iran counter-attacked by launching strikes on nearby nations that housed US military bases. As the conflict has ensued, Iran has been severely damaged, and the reach of the conflict’s disruptions has spread. Central to Iran’s war strategy is applying pressure on US President Donald Trump by effectively closing the Strait of Hormuz, a key passage for seaborne oil exports from the Gulf nations as well as other significant commodities. These exports account for 20-25% of global oil exports, about 20% of Liquefied Natural Gas trade, as well as significant fertiliser volumes. Iran’s underlying strategic rationale is that Trump is particularly sensitive to market woes, so closing the Strait, which has caused oil and other key commodity prices to skyrocket, puts political pressure on the president to back off in the war.

The situation has been further complicated by shifting strategic signals from the United States. Public statements from the administration have varied significantly, ranging from demands for decisive outcomes to indications of limited engagement, as well as evolving positions on the management of the Strait of Hormuz. These fluctuations make it difficult to form a clear view of long-term geopolitical intentions. Fortunately, we are not in the business of geopolitical prognostications. However, we do design our offerings with geopolitics in mind.

Following the disruption caused by the war and up until the end of March, the JSE All Share Index is down 11.3%, and the Rand has depreciated 6.3% against the Dollar, from 15.94 to 16.94. The mechanism is straightforward: a surging oil price raises input costs globally, triggering a risk-off rotation in which emerging market currencies like the Rand take the hit as capital flees to the safety of the Dollar. The High Street Balanced Prescient Fund, with its +90% Rand-hedge, is built precisely for this environment. As the Rand weakens, the Fund’s offshore and Rand-hedge exposure appreciates in Rand terms, cushioning the blow that unprotected portfolios absorb in full. The result: although down 3.8% since the war began on the 28th of February 2026 up to the end of March, the fund has delivered 2.0% alpha against all funds in our ASISA category. The risk-off mechanism worked similarly during quite a different disruption: the outbreak of COVID-19. During the COVID selloff (January–March 2020), the Rand depreciated 27.4% against the Dollar, from 14.00 to 17.84, and the High Street Balanced Prescient Fund delivered 9.6% alpha across the broader ASISA category. For South Africans saving for retirement, this is not a fortunate coincidence; it is the portfolio doing exactly what it was designed to do.

The Bad: Rate and See

One month ago, the question facing most central banks was not whether to cut interest rates but how quickly. In Iran, Trump hoped for a “Venezuelan outcome”. However, that desired short and swift military operation has turned into a prolonged economic standoff. Four weeks later, the conflict rages on, and the Strait of Hormuz remains closed. Potential inflationary effects of the closure are significant and far-reaching. No country is immune. The ripple effects have been swift; central banks that were pricing in cuts are now holding firm and discussing hikes.

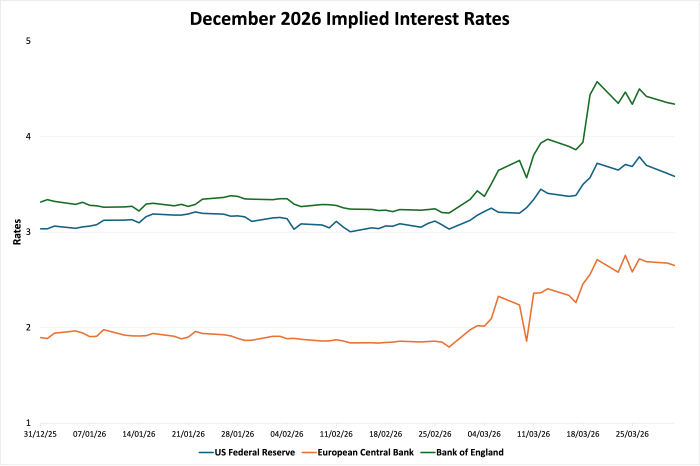

Nowhere is the market’s reassessment starker than in the United Kingdom, where implied rate expectations swung from 55 basis points of cuts to 85 basis points of hikes for 2026. This 140-basis-point move in just three weeks is one of the most dramatic reversals in rate expectations in the modern era. The European Central Bank tells a similar story: from pricing a modest cut below 2% to hikes priced above that level, as illustrated above. The US Federal Reserve is the outlier. No hikes, but cuts are off the table for 2026, partly reflecting the country’s position as a net oil producer.

So, why can’t central banks simply cut rates to cushion the blow? A global supply-side shock, where rising energy costs push up inflation and slow growth simultaneously, is a central bank’s worst nightmare. There is no clean exit, only a choice of which pain to bear. Cut rates and inflation get worse. Raise rates and growth weakens further. The playbook across developed markets has been identical: hold and watch carefully. At home, the South African Reserve Bank unanimously held rates at 6.75%, and the cut expected weeks ago is off the table as the conflict puts petrol and diesel on track for a record increase in April. For South African households already under pressure, the global crisis has arrived at the forecourt.

& Leaving the Clouds Behind

The world’s most powerful technology firms are entering a new space race, as compute infrastructure builders look towards the stars. SpaceX recently filed with the US Federal Communications Commission (FCC) to launch one million satellites, while firms like Blue Origin and Axiom also plan for massive orbital data centre constellations. While NVIDIA recently unveiled its Space-1 Vera Rubin module to bring AI to orbit, Google’s “Project Suncatcher” has provided the most rigorous technical validation to date. By testing their latest Trillium TPUs against proton beams, Google researchers confirmed that high-end AI chips are surprisingly resilient to cosmic radiation, surviving triple the expected five-year mission dose. This move from speculative “moonshot” to viable engineering suggests that space-based compute is no longer a question of if, but when.

Historically, computing has followed energy, with data centres clustered around cheap power sources like hydroelectric power in the Pacific Northwest and geothermal energy in Iceland. Companies are now extending this logic even further: moving compute directly to the most abundant energy source available. In the right orbit, a solar panel is up to eight times more productive than on Earth, providing near-continuous power without the regulatory hurdles or water-intensive cooling requirements of terrestrial locations. As rocket launch costs fall toward a projected cost inflection near $200/kg, shifting compute into orbit could become strategic infrastructure rather than science fiction.

However, the transition involves significant trade-offs, and formidable engineering challenges remain. While the frigid vacuum of space seemingly offers attractive cooling capabilities, it is actually a notoriously difficult environment for thermal management: without air for convection, heat must be bled off via massive, fragile infrared radiators. Furthermore, the sheer scale of proposed networks raises urgent environmental concerns about orbital debris and the degradation of the night sky for global astronomy. Sceptics like OpenAI’s Sam Altman argue that the economics and logistics are not yet feasible at scale. Even so, the investment thesis is compelling. Rapid advances in launch, semiconductor design, and satellite networks suggest that space may become the next critical frontier for the global compute economy.

ENDS