Marcus Rautenbach, Principal Investment Consultant at Simeka

South Africa continues to confront one of its most entrenched socioeconomic challenges: unemployment.

Despite decades of policy debate and reform attempts, joblessness remains alarmingly high and deeply structural. Research institutions have repeatedly highlighted this crisis, warning of the long‑term economic and social risks if the country fails to change course.

The recent improvement in the unemployment rate is a positive development, but does it tell the full story?

According to Stats SA’s Q4 2025 Quarterly Labour Force Survey, 17.099 million South Africans are employed, while 11.550 million are unemployed or discouraged work seekers. The official unemployment rate stands at 31.4%, with the expanded definition reaching 40.3%. These figures demonstrate not only the scale of the crisis but also the persistent inability of the economy to absorb new entrants into the labour market.

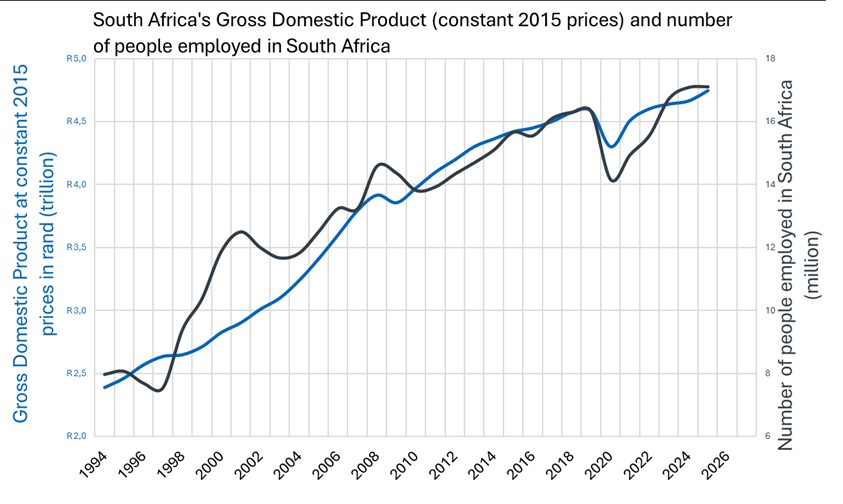

Growth and jobs: An inseparable relationship

South Africa’s employment levels track closely with GDP performance. When economic activity contracts, employment stagnates or declines; when growth accelerates, job creation follows. The data confirms this tight coupling: the correlation coefficient between GDP (constant 2015 prices) and employment is an exceptionally high 0.95.

Source: IRESS

Unfortunately, economic growth has been inadequate. Since the pre‑Covid peak in 2019, GDP (constant 2025 prices) has grown by just 0.6% per annum (p.a.). Since the period prior to the Global Financial Crisis, in 2007, the growth rate has been only 1.2% p.a. Over both periods, population growth outpaced economic performance.

Employment growth has been similarly sluggish:

- 7% p.a. since 2019

- 5% p.a. since 2007

Meanwhile, the number of unemployed and discouraged individuals has grown dramatically:

- 4% p.a. since 2019

- 4% p.a. since 2007

In some provinces, the crisis is even starker. In the Eastern Cape, and in the Northwest during 2024 and 2025, unemployed and discouraged individuals have outnumbered the employed. If current trends persist, by 2040, South Africa could reach a point where unemployed citizens exceed the number of employed – placing immense pressure on social support systems and fiscal sustainability.

Sectoral realities: A mixed and an uneven landscape

Not all sectors contribute equally to South Africa’s employment picture. Private sector job creation has been particularly weak, increasing by only 0.8% p.a. since 2019, while public sector employment has grown at 1.1% p.a. Over the long term since 2007, public sector employment has grown 3.4% annually – significantly outpacing the private sector.

Manufacturing has endured the deepest losses:

- 172 000 fewer jobs than in 2019

- 440 000 fewer jobs than in 2007

Its share of national employment has dropped from 15% in 2008 to 9% in 2025 – evidence of ongoing deindustrialisation. While productivity improvements could offset job losses, the data does not show this is happening at a meaningful scale.

From 2009 to 2016, public sector hiring masked weak private sector performance. However, this pattern is neither fiscally sustainable nor conducive to long‑term growth.

The growth-employment debate

A long-standing question in economic policy is whether job creation drives growth or whether growth drives job creation. The evidence suggests that while the relationship is complex, weak growth almost always results in fewer jobs. Conversely, job losses do not necessarily reduce GDP growth immediately.

In 2025, South Africa’s GDP totalled:

- R7.6 trillion in current prices

- R4.5 trillion in real terms (constant 2015 prices)

Every R1 billion in GDP growth translates into 2 000 to 4 000 additional jobs, depending on the measurement basis. Yet despite this, corporate sector employment has expanded by only 0.8% p.a. over the past six years – while a key labour‑absorbing sector such as manufacturing has contracted.

Capital formation – investment in productive assets such as factories, machinery, technology and infrastructure – remains crucial. It drives both job creation and higher wages. But this is overwhelmingly a private sector function, and South Africa has not been attracting this type of investment at the scale required for meaningful employment gains.

A narrowing window for reform

If job creation and inclusive growth are truly national priorities, policymakers must address the regulatory and structural barriers holding back economic expansion. The upcoming labour legislation review, the first since 1994, represents a critical opportunity to modernise outdated frameworks and remove disincentives to investment and hiring.

Without decisive action, South Africa faces a shrinking tax base, rising dependency on social grants, and the real prospect of becoming a country where the majority of working‑age adults are unemployed.

Sources: Statistics South Africa, IRESS

ENDS