Ndivhuho Netshitenzhe, Senior Economist at Stanlib

SA’s much-anticipated two-pot retirement system will take effect on 1 September 2024. Under the new system, retirement fund members will be able to access a portion of their pension funds before retirement age. In the current system, members can only access these funds when they retire, are retrenched, or resign.

The temptation to access this pool of funds by resigning has proven too strong for many people. This is damaging for both the individual as well as the economy, especially given the country’s low savings rate. Between 2011 and 2020, over 6.1 million people have opted for early pension fund withdrawal, with an average of around 700 000 withdrawals every year since 2016.

According to the Association for Savings and Investment South Africa (ASISA), because of early withdrawals, only 6% of South Africans can retire comfortably. Although this statistic emphasises the urgent need for pension reform, the new retirement system is likely to have unintended short-term as well as long-term consequences for the economy, both positive and negative.

Why a new retirement system is needed

To dissuade individuals from accessing their retirement savings before retirement, higher tax rates are levied on early withdrawals. Since 2016, the tax on early withdrawals averaged over R12 billion a year, far higher than the tax paid upon retirement (see graph).

Unfortunately, the large number of withdrawals indicates that severe tax implications were not enough to minimise early withdrawals.

The growing amount of withdrawals reduces the amount available for employees on retirement, something that the two-pot system aims to address. It does this by allowing individuals some access to their retirement savings during times of difficulty without their having to resign. At the same time, the aim is to ensure that most of their retirement savings are off limits until retirement. The flexibility is meant to reduce households’ financial stress while improving long-term savings.

How the two-pot retirement system will work

From 1 September 2024, existing and new retirement contributions will be split into three components (pots):

1. A third of total retirement contributions (made after the implementation date) each year will go into the savings component.Funds in this pot will be accessible at any time without the need to resign. The only restrictions are that withdrawals must be a minimum of R2 000, can only be made once a year, and will be taxed at individuals’ marginal tax rate.

2. The remaining two-thirds of contributions from 1 September will go into the retirement component. Funds in this pot cannot be accessed until retirement.

3. All accumulated pension fund contributions made until 31 August 2024 will go into the vested component. Access to this pot is possible upon resignation or retirement. In addition, 10% of the value of this component (up to R30 000) will be transferred, once-off, to the savings pot on 1 September.

Possible economic impact of the two-pot system

The implementation of the two-pot system will provide some additional economic stimulus, with the magnitude depending on uptake of the available funds and how they are used. There are different estimates of the amount that could be withdrawn, ranging from R20 billion to R100 billion over 2024-25. We are assuming a relatively conservative withdrawal of R50 billion, which would equate to a R40 billion after-tax boost to consumers’ disposable income (assuming an average marginal tax rate of 20%).

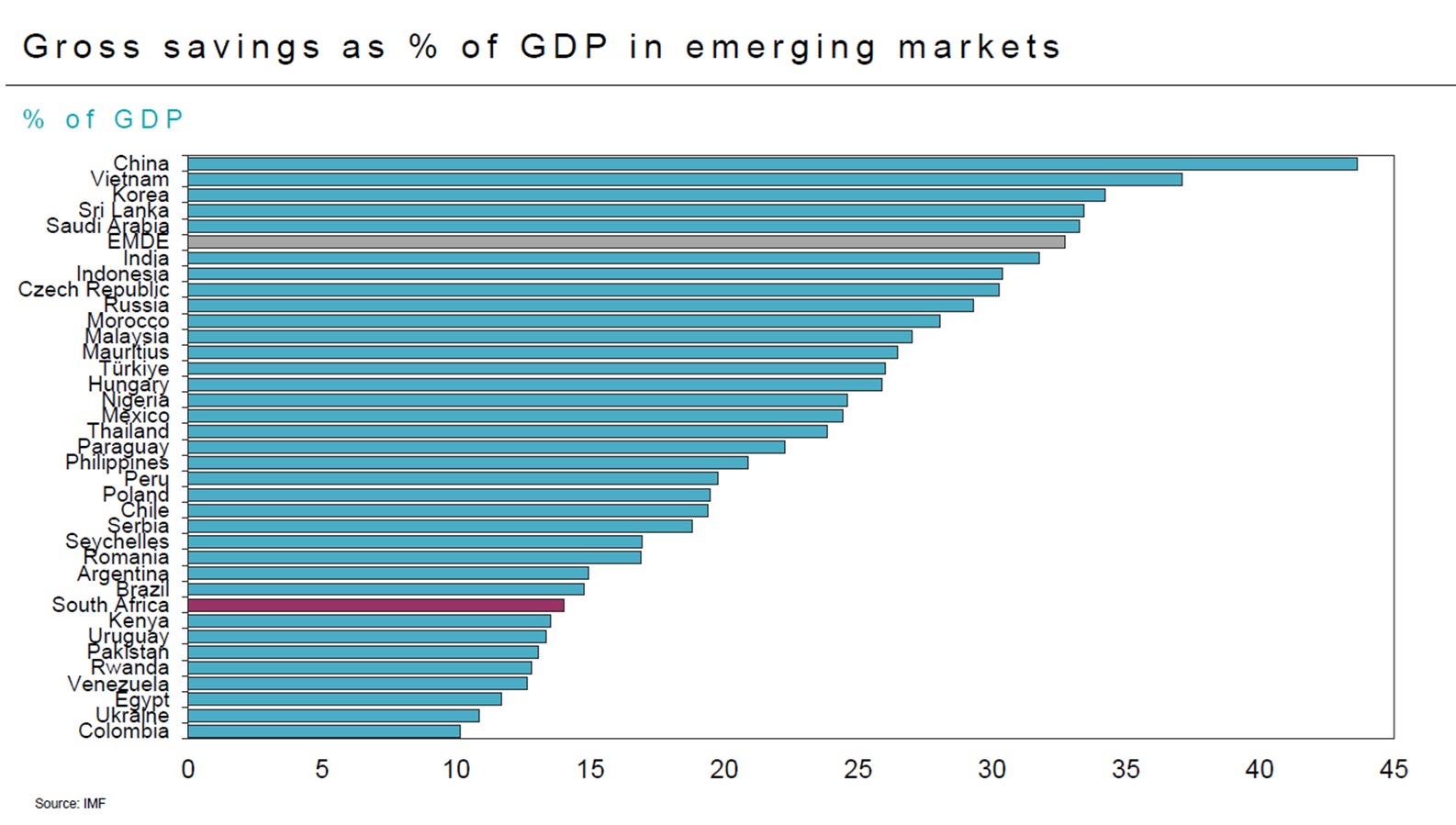

Unfortunately, this type of withdrawal will reduce SA’s savings in the short term. SA’s gross savings in the first quarter of 2024 represented only 12.7% of GDP, the lowest amount ever recorded. In addition, SA’s savings are extremely low even by international standards (see graph).

Household savings have been negative for the last six quarters, with net household savings at -0.9% of disposable income in the first quarter of 2024. Allowing withdrawals from contractual savings will further decrease SA’s savings rate. The reduction in savings will decrease the pool of funds available for investments, causing private sector fixed investment growth to decline.

While some surveys seem to suggest that up to 50% of the money withdrawn will go to paying down debt, we argue that a large portion will simply be used for general consumption. Consumers, especially middle-income earners (the most likely to withdraw from their savings pot), have faced some headwinds recently that have left them short of discretionary income.

Firstly, prices of essential goods and services like education, medical aid, electricity, and water have increased substantially, leaving less for discretionary spending. Secondly, banks have tightened lending standards, limiting consumers’ ability to use credit for discretionary spending. These consumers are also paying more for their debt. Thirdly, National Treasury has not compensated individuals for fiscal drag, so earners are giving proportionally more to taxes this year. Because of these developments, there is an element of pent-up demand for discretionary items like clothing and appliances.

Amid these pressures, government is giving access to long-term savings (effectively implementing a government-induced stimulus). It is therefore likely that consumers will use these additional funds for discretionary spending rather than reducing debt or building buffers against higher costs of medical aid, education, etc.

Positively, this means that the additional disposable income will boost consumption towards the end of this year and in 2025. It is important to note, however, that the increase in household consumption expenditure is likely to be import-intensive, limiting the upside benefit to overall GDP. We calculate that GDP is likely to increase by an additional 0.2 percentage points in 2024 and 0.2 percentage points in 2025.

There will also be a positive impact on government finances as tax revenue collection increases. We project taxes will increase by R16 billion (0.3% of GDP), led by increases in personal income tax, VAT and corporate income tax. If government spending is unchanged, this will result in the narrowing of the fiscal deficit-to-GDP ratio and thus the government debt-to-GDP ratio by 0.2 percentage points and 0.7 percentage points respectively in 2024/25. This should lower the risk premium, offsetting the potential rise in inflation from increased spending, meaning the South African Reserve Bank would still be able to cut rates this year and next year.

While the two-pot system aims to offer fund members flexibility to access their retirement funds in times of distress, it is essentially turning long-term savings into short-term consumption in a country that has very little savings to start with. Hopefully, expectations are correct that the magnitude of annual net outflows will dwindle over time, settling at levels lower than the current annual outflows. Unfortunately, international experience shows that if these types of reforms are not well designed and implemented, the boost to economic activity tends to be short-lived and results in a decline in pension savings over the long term. All this occurs without alleviating the financial pressure on consumers by reducing their debt or enabling them to build a buffer against higher costs.

ENDS