Sanisha Packirisamy, Chief Economist at Momentum Investments

Headline inflation, as reported by Statistics (Stats) SA, rose to 3.6% y/y in December 2025 from 3.5% y/y in November, resulting in an average inflation rate of 3.2% for 2025.

December’s inflation rate matched the Reuters median consensus of 3.6%, while the 2025 average inflation rate was below our estimate, the Reuters consensus and the SARB’s forecast of 3.3%.

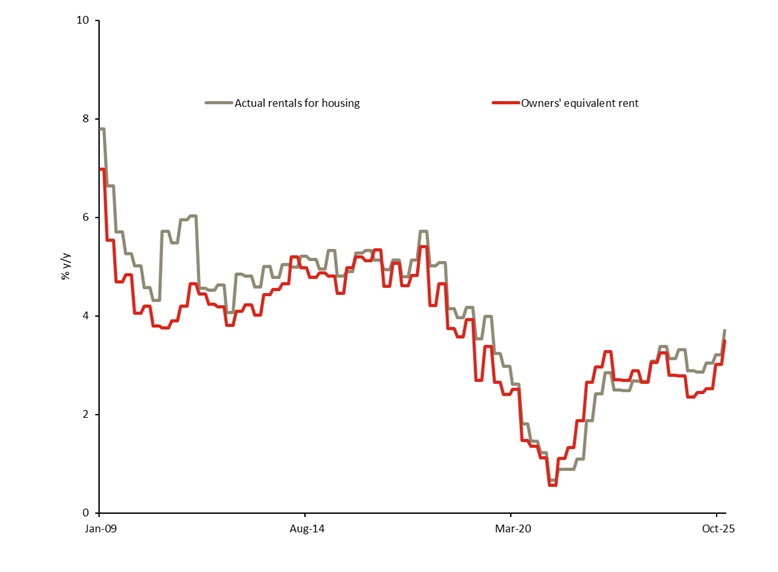

Transport inflation edged up to 1% y/y in December from 0.7% y/y in November and restaurant and accommodation services prices increased by 2.9% y/y from 2.3% y/y over the same period. In terms of housing prices, actual rentals were up 3.7% y/y in December from 3.2% y/y in in November and owners’ equivalent rent was up 3.5% y/y from 3% y/y over the same period.

Chart 1: Housing inflation edges higher after a prolonged pandemic-induced slump

Source: Stats SA, Momentum Investments (Data until December 2025)

According to an article in BusinessDay, the property rental market continues to display divergences. The residential sector is experiencing robust momentum, driven largely by a persistent shortage of available rental stock. This supply constraint is fuelling expected rental escalations between 4.5% and 5.5% for 2026, especially in key growth areas within Gauteng. This signals upward pressure in rentals going forward. However, buy-to-let activity is increasing, with ooba reporting that buy-to-let investment properties accounted for 12% of all home loan applications in 2025, up from 10.9% in 2023. Furthermore, there is ongoing commercial-to-residential conversions, particularly in Gauteng. This increase in supply could limit the upward rental pressure. In contrast, the commercial property sector (most notably office space) remains subdued, with rental escalations expected to moderate to about 3% in 2026.

Core inflation rose to 3.3% y/y in December from 3.2% y/y in November, largely due to the rise in housing costs.

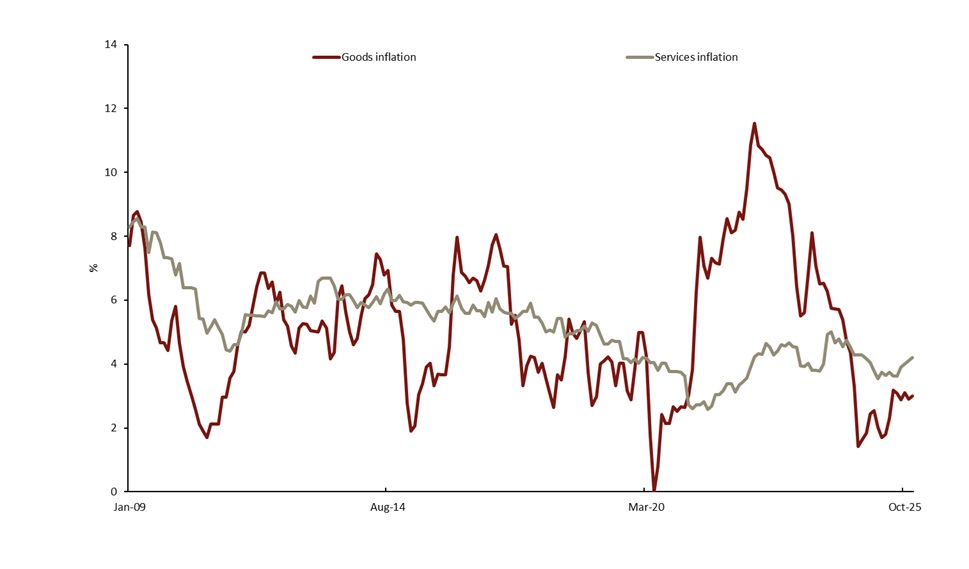

Chart 2: Services inflation remains sticky

Source: Global Insight, Stats SA, Momentum Investments (Data until December 2025)

Goods inflation accelerated to 3% y/y in December, from 2.9% y/y in November, but was lower than the peak rate of 3.2% y/y recorded in July 2025. Contained goods inflation can be attributed to the strengthening of the currency and a reduction in fuel prices, both of which have helped to contain input costs, imported inflation and retail prices. Services inflation climbed to 4.2% y/y from 4.1% y/y, reaching its highest level for 2025. The persistent elevation in services inflation signals a degree of stickiness in underlying price pressures. This stickiness may complicate efforts to bring overall inflation to target, as services represent a slightly larger portion of the consumer basket (51.6% vs 48.4% for goods). We may see a downward trend in services inflation once contracts start to adjust to the new lower target.

For Momentum’s full note on the latest CPI figures, click here.

ENDS