Sanisha Packirisamy, Chief Economist; & Tshiamo Masike, Economist; at Momentum Investments

Fitch Ratings upgraded South Africa’s (SA) sovereign credit rating from BB- to BB on 5 June 2026, marking the first upgrade since 2005, while maintaining a stable outlook. The upgrade primarily reflects SA’s “record of prudent fiscal management and progress in fiscal consolidation despite weak economic growth and domestic and global shocks”. Fitch noted that stronger fiscal outcomes, together with revisions to gross domestic product (GDP) data, have left the debt-to-GDP ratio materially lower than anticipated when the sovereign was downgraded to BB- in 2020.

Fitch highlighted that SA has recorded primary budget surpluses, averaging around 1% of GDP, over the past four fiscal years, a notable improvement from the average primary deficit of 0.6% of GDP recorded between fiscal year (FY) 2011/12 and FY2019/20. The primary surplus is projected to widen to 1.7% of GDP in FY2027/28, supported by expenditure restraint, including lower real transfers to households and local government, a public sector wage agreement that caps salary increases at 4% and an early retirement programme to rein in the civil servant wage bill. Higher commodity prices are also expected to support stronger tax revenue collection. As a result, the consolidated fiscal deficit is expected to narrow, while government debt is projected to stabilise at around 80% of GDP (including local government debt) over the next two fiscal years. Fitch also highlighted a lower risk of contingent liabilities, reflecting improved financial performance at major state-owned enterprises, a view shared by Moody’s and S&P.

Progress on structural reforms has eased some of the supply-side constraints that have weighed on economic growth, particularly in electricity and logistics. As a result, Fitch revised its growth forecasts modestly higher, with real GDP growth expected to improve from 1.1% in 2025 to 1.4% in 2027. However, growth remains a key credit constraint, with the 2027 forecast of 1.4% well below the projected BB median of 4%.

Political risks were assessed as being elevated ahead of the local government elections scheduled for 4 November 2026, with tensions within the Government of National Unity (GNU) expected to rise. Nevertheless, Fitch’s base case is that the GNU remains intact through its full term until the next national elections in 2029. The agency also expects President Cyril Ramaphosa to remain in office despite an impeachment committee being set up regarding the Phala Phala matter, noting that the ANC remains the largest party in Parliament with 40% of the seats. A two-thirds majority would be required for impeachment and this is a high threshold.

Fitch also views the fiscal impact of the Middle East conflict as manageable. While the announced temporary fuel levy relief will reduce revenue, Fitch expects this to be offset by stronger corporate income tax collections, supported by elevated commodity prices. Inflation is expected to remain above the SA Reserve Bank’s (SARB) new 3% target and 2% to 4% tolerance band, reaching 4.5% at the end of 2026. As such, Fitch expects one additional 25-basis point interest rate increase later this year.

Despite the credit rating upgrade, SA’s credit profile remains constrained by relatively high debt levels, weak economic growth and elevated debt-servicing costs compared with similarly rated sovereigns. Government debt is expected to stabilise at around 80% of GDP over the next two years, compared with a projected BB median of 53%, while the interest-to-revenue ratio is forecast at 19% in 2027 versus a BB median of 11%. However, Fitch highlighted several important strengths, including the long average maturity of government debt, a low share of foreign-currency-denominated debt and stronger reserve adequacy with the SARB’s international reserves expected to remain above 5.5 months of current external payments compared with the BB median 2027 forecast of 4.8 months.

According to Fitch, a further upgrade would require a sustained decline in government debt-to-GDP and stronger medium-term real growth prospects, while a failure to stabilise debt or a material deterioration in growth and fiscal outcomes could place downward pressure on the credit rating.

Fitch’s sovereign rating model generates a rating equivalent to BB+, but the agency applies qualitative overlays to reflect factors not fully captured by the model, pulling down the final rating to BB. Importantly, Fitch removed the negative adjustment previously applied to public finances, reflecting greater confidence in the government’s fiscal trajectory and debt stabilisation efforts. However, it retained a negative one-notch qualitative adjustment for SA’s weak medium-term growth prospects, underscoring that economic growth remains the key constraint on the sovereign rating.

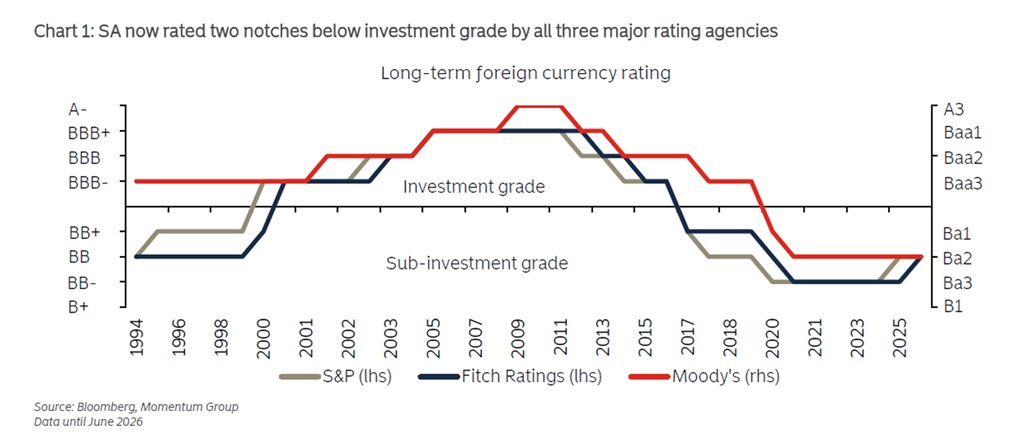

At BB, Fitch’s rating is now aligned with Moody’s and S&P (see chart 1). However, Fitch maintains a stable outlook while both Moody’s and S&P have positive outlooks. The upgrade was somewhat unexpected given Fitch’s previous stable outlook and the heightened uncertainty arising from the Middle East conflict.

The next reviews by Moody’s and S&P are scheduled for 27 November 2026, just over a month after the Medium-Term Budget Policy Statement on 28 October and shortly after the local government elections. If fiscal performance continues to improve and government debt has indeed peaked in FY2025/26, further positive rating actions from Moody’s and S&P remain plausible, provided geopolitical developments and a potential El Niño event does not materially weaken the growth outlook or fiscal trajectory.

ENDS

Author

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

-

@Sanisha Packirisamy, Momentum Investments

@Tshiamo Masike, Momentum Investments

-

@Tshiamo Masike, Momentum Investments

-

@Tshiamo Masike, Momentum Investments

-

@Tshiamo Masike, Momentum Investments

-

@Tshiamo Masike, Momentum Investments

-

@Tshiamo Masike, Momentum Investments

-

@Tshiamo Masike, Momentum Investments

-

@Tshiamo Masike, Momentum Investments

-

@Tshiamo Masike, Momentum Investments

-

@Tshiamo Masike, Momentum Investments

-

@Tshiamo Masike, Momentum Investments

-

@Tshiamo Masike, Momentum Investments

-

@Tshiamo Masike, Momentum Investments

-

@Tshiamo Masike, Momentum Investments

-

@Tshiamo Masike, Momentum Investments

-

@Tshiamo Masike, Momentum Investments

-

@Tshiamo Masike, Momentum Investments

-

@Tshiamo Masike, Momentum Investments

-

@Tshiamo Masike, Momentum Investments