Izak Odendaal, Investment Strategist at Old Mutual Wealth

Investors have suffered serious whiplash over the past five weeks. After shaking the foundation of the global trading system on “Liberation Day”, as he termed the 2nd of April, US President Donald Trump has been backing down. The good news is that the most extreme scenarios are now much less likely. Recession risks have fallen and so has the possibility of a severe market response. The main reason is that the US and China agreed to a trade truce last week, putting most of the tit-for-tat import taxes on hold for 90 days. The bad news is that this is unlikely to be the end of Trump’s trade wars. More uncertainty and, probably, volatility lie ahead. But for now, we can all sleep a bit sounder.

Embargo

Tariff levels between the two largest economies jumped so high that it would have effectively been an embargo. The trade truce will come just in time for American retailers to keep shelves stocked for the second half of the year, particularly for the Christmas shopping season. It will also be a huge relief for Chinese manufacturers.

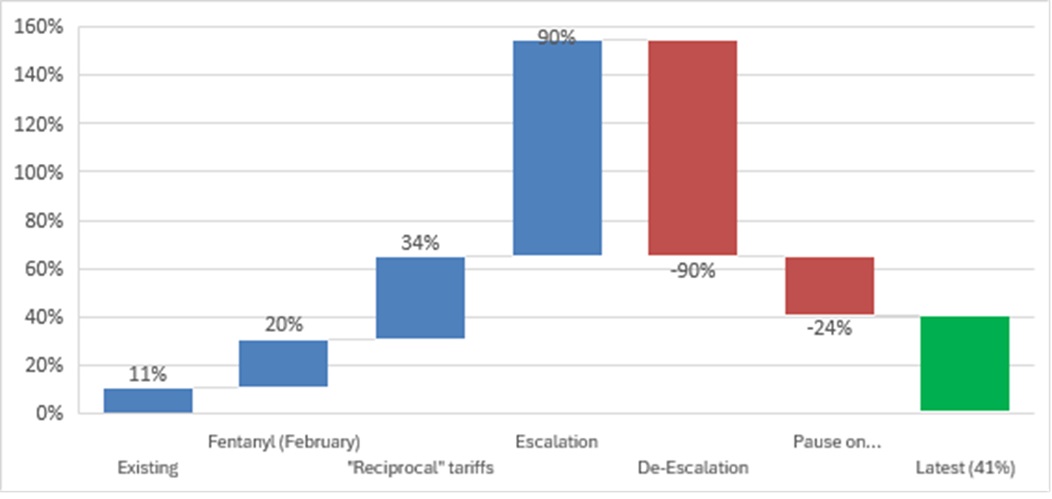

Chart 1: Change in US tariffs on Chinese imports

Source: Yale Budget Lab

As for the broader US-China relationship, the trade agreement should be seen as a ceasefire, not a complete reset. For one thing, it does little to address the unbalanced trade relationship between the two countries that led to the tariffs in the first place. Moreover, the tensions that have built up in recent years are likely to continue as the US strains to maintain its military and technological lead over China. However, both sides recognised that mutually assured destruction in trade is in neither country’s interest.

Still high

After all the sound and fury, US import tariffs on Chinese imports have fallen from 145% to 41%. China’s retaliatory import tariffs have been lowered from 125% to 10%. Your degree of optimism will depend on your starting point. The 41% tariff level looks fantastic if you are anchoring off 145%. However, it is still very high when compared to 11%, where it was at the start of the year.

Since China is a large supplier to the US, the effective tariff rate on the overall American import basket is still around 14%, according to calculations by Yale University’s Budget Lab, compared to less than 3% when Trump took office. While the “reciprocal” tariffs imposed on the 2nd of April on 60 countries were suspended (including those on Chinese imports), the 10% across-the-board tariff looks set to remain, as was the case in the recent US-UK deal.

Therefore, American consumers still face higher prices, while businesses are likely to experience disruptions to their supply chains. This is likely to put downward pressure on US economic growth, and business activity across the globe. For instance, Walmart, the largest retailer in America, warned last week that it would not be able to absorb the full impact of tariffs, and would have to pass some of the cost increase on to consumers. It is the biggest single importer of goods in the US. Trump posted on social media that Walmart and other businesses should “eat the tariffs” instead, but this would imply smaller profit margins.

In other words, the trade war is not over, but its intensity has eased for now. It is anyone’s guess what happens after the 90-day grace period, but the pattern so far suggests that Trump will continue making deals. As one commentator put it, we’ve gone from “Liberation Day” to “Capitulation Day.”

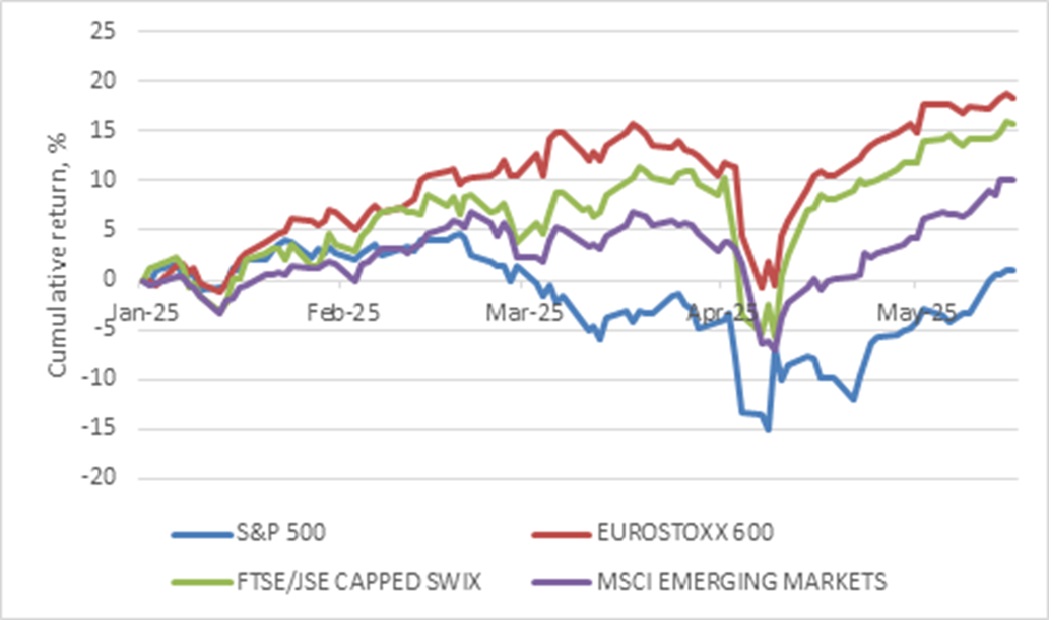

The stock market response borders on euphoric. The S&P 500 has gained 19% since the April 8 low and is back into positive territory for the year. Other equity benchmarks from around the world are also above pre-Liberation Day levels, as if nothing changed.

Chart 2: Equity benchmarks in dollars

Source: LSEG Datastream

On the one hand, this is a reminder of how difficult it is to time the market, since the rebound can be just as fast as the crash. Investors who stuck to their strategy have been rewarded for their patience and grit.

On the other hand, however, a lot has changed. US import tariffs might not at settle at extreme levels, but they still look set to end up at multi-decade highs with negative economic implications. Confidence in the US as the source of stability in the global economic and financial system has been shaken. By one count, Trump has changed tariff policy 50 times since taking office on the 21st of January. This is no way to run the most important economy on earth. It also means that, even when they secure deals with the US, leaders of other countries will know that Trump can shift the goalposts later, as he has done before.

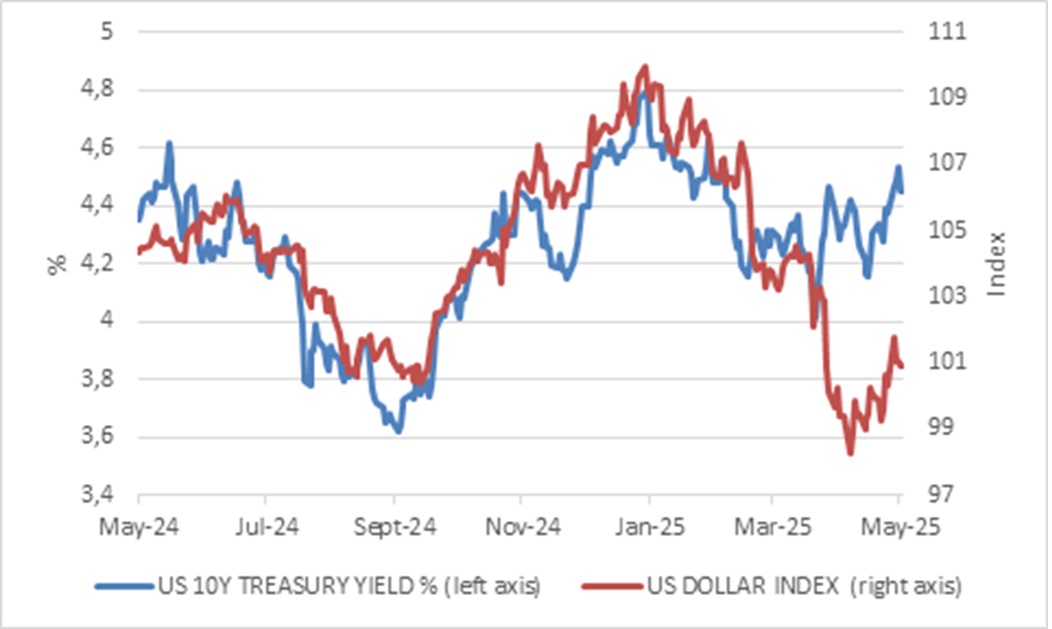

While equities staged a V-shaped recovery, the US dollar has not. US government bond yields are higher since the tariff announcements were made, meaning bond prices are lower. The higher bond yields partly reflect a dialling back of interest rate cut expectations, and partly the shift in attention from trade policy to fiscal policy. A new budget bill is making its way through Congress with the potential to further increase the already-sizable US government deficit (more on that next week). Fiscal policy risks also led to Moody’s cutting the US government’s credit rating from Aaa for the first time since 1919 over the weekend.

Chart 3: US dollar index and 10-year Treasury yield

Source: LSEG Datastream

In terms of monetary policy, the Federal Reserve has taken a wait-and-see approach. It kept interest rates unchanged at its last three meetings, including the most recent one on the 7th of this month. Fed officials will feel vindicated that this has been the right course of action. Like the rest of us, they did not know what would happen to tariffs. And we still don’t know. Though it does appear that Trump will not steer the car over the cliff, he might still drive very close to the edge in the months ahead.

This uncertainty will have an impact on business activity and employment. The US economy was likely to slow this year anyway, but tariffs and uncertainty will add extra downward pressure. This means that the Fed is still likely to cut rates later this year, though the market now only discounts two rate cuts this year, down from four a few weeks ago.

Importantly, US inflation data remains well behaved, but it is still early. Though the first tariffs were imposed in February already, importers built up inventory over several months and customers have largely been spared higher prices to date. This won’t last forever. However, it helps that the oil price is about $10 per barrel lower since the start of the year, and down 20% over 12 months.

For central banks outside the US, the situation is easier. The trade war is a demand shock that risks sending growth and prices lower, and interest rate cuts is a tried-and-tested response. Since the 2nd of April, 15 central banks have cut interest rates, including the Bank of England, the European Central Bank, the Bank of Mexico and the People’s Bank of China.

Last but not least

The South African Reserve Bank is now more likely to join that list. The rand-dollar exchange rate has stabilised after the steep declines in the wake of the 2nd of April tariff shock. It hit a low of R19.89 on the 8th of April as global markets were gripped by panic. As global investors started exhaling, the rand regained lost ground, repeating a pattern we’ve seen many times before. Here too, trying to time the market would have been difficult.

If global market conditions stabilise, the Reserve Bank can put more emphasis on domestic inflation dynamics. Consumer inflation fell below its 3% to 6% target range in March, meaning that the real repo rate is now sitting at 4%. The rand oil price is 20% lower than a year ago and will detract from inflation readings for the next few months until base effects kick in later this year. There is a Monetary Policy Committee (MPC) meeting on the 29th of this month, and then again in late July, September and November. May’s meeting is a close call, but by the July meeting the MPC (and the rest of us) will know what happens after the 90-day tariff pause passes. Further interest rate relief will support the nascent recovery in consumer spending; however, the extent of rate cuts could be limited by a shift to a lower inflation target. The Deputy Finance Minister suggested at an investors conference last week that an announcement on discussions between the Bank and Treasury on the matter will be made soon.

And then there is the matter of trade. The 10% across-the-board tariff applies to non-mining South African exports to the US. This means AGOA is effectively dead, and is a headwind for the local economy, though not a catastrophe. National Treasury is likely to downgrade its growth assumptions in next week’s Budget 3.0 but is still likely to show a notable improvement from 0.6% growth 2024. President Ramaphosa will meet Trump in the White House next week, hopefully leading to a thaw in US-SA relations and ultimately a trade deal. This would reduce the risk of extreme outcomes for the local economy too. Failure to secure an agreement could see US tariffs on South African goods jump to 30%.

Diversification, not big bets

In summary then, the global economic and market outlook has improved compared to the 2nd of April but is still worse than what it was on the 1st of April. Uncertainty remains, and with it, the likelihood for further market volatility. Of course, investors always face uncertainty, since the future is unpredictable. What makes this situation different is that the upheaval is caused by one man sitting in the Oval Office. Over the past century or so, it didn’t really matter to markets who the US president was, because policymaking was done by a range of government bodies, including Congress, and was relatively predictable. However, a loophole in US trade law allows the president to set tariffs unilaterally, and Trump has taken that gap like none of his predecessors. Therefore, investors making big bets on where things are headed next are taking bigger risks than previously. Worst-case scenarios seem less likely, fortunately, but it is still a time for prudent diversification and patience.

ENDS