Izak Odendaal – Old Mutual Wealth Investment Strategist

The battered and bruised South African economy contracted by more than expected in the fourth quarter of 2022, the latest in a bleak landscape of bad news stories.

According to Stats SA, gross domestic product, the broadest measure of economic activity, declined by 1.3% from the third to the fourth quarter, adjusted for inflation and seasonality. This was much worse than expected and is a big number in absolute terms.

Eskomplicity

It does not take a trained economist to realise that loadshedding carries much of the blame, with big declines in the energy-sensitive manufacturing, mining and agricultural sectors. Electricity production itself is a meaningful contributor to overall economic activity in its own right, responsible for R100 billion a year in real value added. No surprises that it contracted 1.9% in the quarter.

However, there was also an unusually large 3.2% decline in the financial sector that is generally less affected by loadshedding. Given that it is the biggest sector in the economy – it was responsible for the fact that the overall growth number was so much worse than anticipated. On the plus side, its poor performance is unlikely to repeat.

Feel the base

Part of the reason for the big decline in the fourth quarter was the strong 1.8% growth in the third quarter, which creates a high base for the quarter-on-quarter comparison. Base effects are one of the reasons why economic data should always be analysed from multiple angles. Another reason is simply that data is often updated, as was indeed the case with third quarter data. Stats SA doesn’t physically count every single transaction or follow every worker, farmer or delivery van in the economy – maybe one day central bank digital currencies will make this possible – and so GDP is an estimate and gets revised, usually upwards, when new information is available. In understanding where we are and where we are headed, it is important to corroborate various data items with one another, and sometimes, with what you can see with the naked eye.

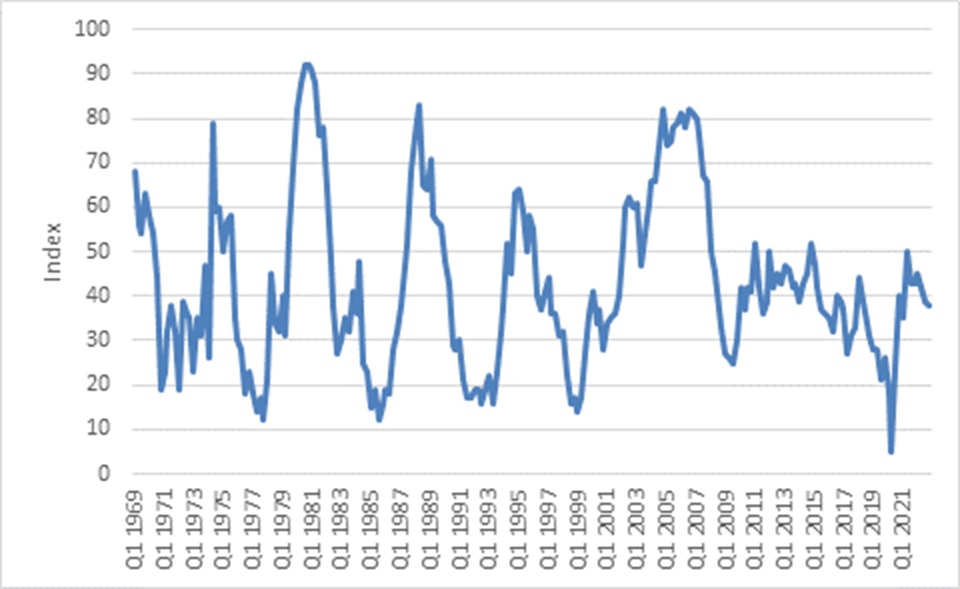

For instance, listed companies report regular sales numbers from different sectors, and we can compare that with the official data. We also have survey data from the likes of the Bureau for Economic Research. Its RMB Business Confidence Index has been measuring swings in sentiment in key cyclical industries since 1970. It fell further from 38 in the fourth quarter of 2022 to 36 in the first quarter. Any reading below 50 suggests respondents are on balance negative about business conditions. Strikingly, the index has been stuck below 50 for most of the past decade. In contrast to the boom-bust cycles that are clearly evident before 2010, the period since can only be described as treading water. Many businesses chose to expand offshore in this time, and few had success.

Chart 2: RMB/BER Business Confidence Index

Source: Bureau for Economic Research

The low growth trap

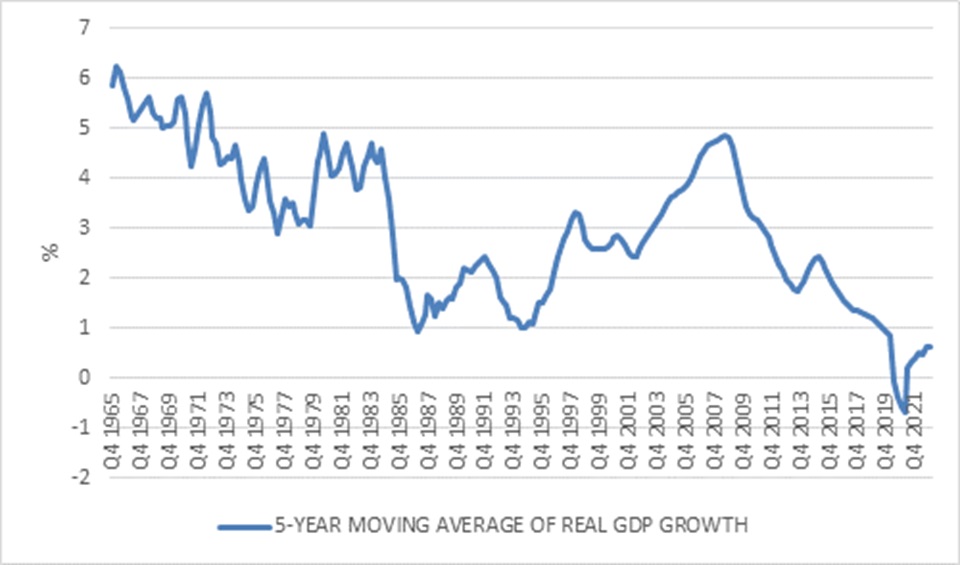

The economy is considered to be in a technical recession when it experiences two consecutive negative quarters, and this might very well happen (first quarter growth data will only be available in June). But the concept of a technical recession is fairly meaningless in a slow-growing economy. Though the long-term average growth rate of the economy is 3% (since 1960 when GDP was first estimated), the average over the past decade is 1%.

Chart 2: South African Growth History, %

Source: Stats SA

A low-flying airplane is at greater risk of crashing if it hits an air pocket compared to one at cruising altitude. Similarly, an economy with trend growth of 1% is going to experience negative quarters quite often, whereas if the economy is chugging along at 3%, two negative quarters will be unusual and noteworthy.

Unfortunately, South Africa is stuck in such a low-growth environment (some would say trap), but this is not necessarily a recession. Household spending was positive in the fourth quarter, and this is the largest component of economic activity when viewed from the expenditure side (as opposed to the production side). A recession is best thought of as a deep, long-lasting decline in production, employment, and income across a broad range of sectors.

Invest for success

What gets you out of the low-growth trap? Investment. When the public and private sector invests in the country’s capital stock, it raises productivity and supports faster growth. Pumping more money from the fiscal side or slashing rates won’t do the trick. We don’t have a shortage of workers. The South African labour force continues to grow steadily, and therefore is not a constraint on long-run growth as is the case in developed economies and China where the labour force growth has ground to a halt or even gone into reverse, pulling down long-run potential growth rates. The lack of skilled workers is a constraint, however, and therefore investment in education and training is also important. This doesn’t necessarily mean university degrees. Many of the skills in short supply are technical and hands-on in nature, such as electricians.

When an economy invests more, it gets a double whammy of short-term and long-term growth. In the short term, the act building the factory or upgrading the software adds to gross domestic product, but it also facilitates future economic activity.

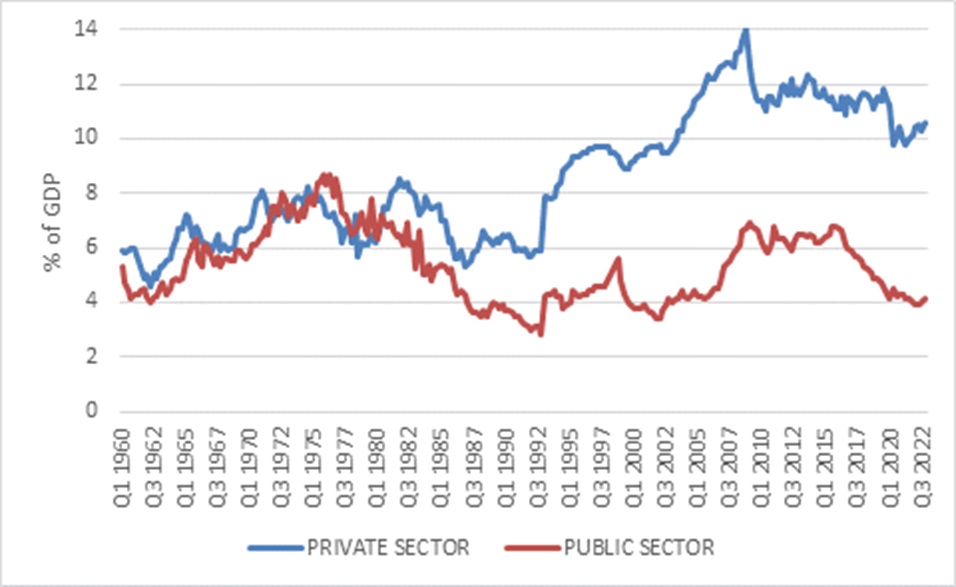

The ideal number for investment is often stated as 30% of GDP, but in truth, any improvement from current depressed levels will do wonders. As chart three shows, private fixed investment has been improving over the past few quarters – encouragingly – but remains below the pre-pandemic peak, which is itself still below the pre-2008 peak. Public investment (general government and state-owned enterprises) has declined sharply over the past eight years due to increasing financial constraints. Since these constraints are not going to ease, the importance of public-private partnerships is increasing. In total, fixed investment spending was only 14% of GDP in the fourth quarter. This still amounts to R900 billion a year, so the notion that there is no investment that takes place is false. But clearly it is not enough.

Chart 3: Fixed investment spending, % of GDP

Source: Stats SA

To raise investment levels, businesses need confidence about the future. This means regulatory certainty, but also the knowledge that the rule of law will hold. This requires tackling the various extortion mafias that have mushroomed recently. But on a more mundane level, it also means making it easier to get permits and approvals and the like. Importantly, the government and state-owned enterprises should not hoard investment opportunities, such as in railways and ports, and then fail to invest themselves. Fortunately, on the energy side, the crisis of stage six loadshedding has been so severe that the government has thrown the doors wide open to let the private sector invest as much as it wants. This, and not the work of the new Electricity Minister, will ultimately ease the pain of loadshedding.

Investing in a low growth environment

A slow-growing economy has several investment implications. Globally, low potential growth rates associated with ageing populations and excess savings, resulted in low interest rates for much of the past two decades, not just central bank policy rates, but long bond yields too. It is an open question whether the post-pandemic inflation surge has resulted in a permanent break from this era, or whether we will return to it in two or three years.

Investment will play a big part in this story too. If there is going to be a global capex boom to ride the waves of automation, AI, reshoring and the green transition, it might well soak up the savings glut and permanently raise rates.

In South Africa, unfortunately, a slow-growing economy has the opposite effect on interest rates. This is because it worsens the government’s fiscal position. A sluggish economy does not deliver the tax revenues needed to service government debt and its perceived creditworthiness deteriorates. It is not a huge surprise that S&P Global lowered its outlook on government debt from positive to stable last week, citing the negative impact of sustained loadshedding and declining commodity prices. Investors demand higher yields to compensate for this increased credit risk. South African government long bond yields are above 10%, meaning debt compounds at a faster rate than the ability to service that debt (nominal GDP growth). This results in interest payments rising relative to tax revenues, squeezing out other areas of spending. In the end there is no choice but to turn to austerity to slow the growth in government debt and reduce the risk premium in the bond market.

This is not easy or costless. Spending cutbacks impact frontline service delivery, indirectly in the case of the violent public nurses strike underway. It also puts pressure on capex as noted above, which can further hurt long-term growth rates. Breaking this vicious cycle is crucial, and the solution is to crowd in private sector expertise, capital, and risk appetite.

Faster growth would mean more money for nurses and infrastructure, but also lower borrowing costs, freeing up money for long-term investments that support long-term growth. A virtuous cycle in other words.

But we are not there yet. South African bond yields do not move in isolation and will rise and fall with global yields. But in a slow-growing economy bond investors should not expect major capital gains that stem from a rerating relative to peers as the risk premium declines (bond yields and prices move in opposite directions). However, they can continue to earn generous interest rates. And importantly, the risk of inflation eroding that interest income declines when growth is tepid and the Reserve Bank remains committed to price stability.

In fact, despite the downside GDP surprise, the Monetary Policy Committee could still raise the repo rate later this month since the global interest rate cycle – particularly the US rate cycle – is still going strong.

For JSE-listed equities, the picture is more complicated. Some companies are heavily exposed to the domestic economy and its challenges, but others aren’t. Most of the real giants on the JSE (Naspers/Prosus, Richemont, Anglo American and BHP) are global. Therefore, the link between the local economy and local stock market is weaker than most imagine. Nonetheless, the same pessimism that stalks the bond market applies to SA equities and the JSE trades at a wide discount to global markets and its own history.

Globally, the best long-term returns are usually generated by buying investments at discount. When bad news is already priced in, you don’t need things to go exactly right, you just need them to go somewhat less wrong. This is very possible in South Africa. The economy is battered but not broken, neither are the key institutions that govern and sustain it. It generated R6.6 trillion in income last year, R446 billion more than the prior year, and continues to offer tremendous business prospects. Smarter policymaking and more effective implementation will go a long way to improving the business climate and unlock some of these opportunities, and there is evidence of this happening, electricity being the best example. Nonetheless, prudent diversification means South African investors should continue to maintain appropriate offshore exposure to hedge against all the domestic risks we are so familiar with. Indeed, the relaxation of offshore limits for retirement funds allows investors to completely rethink what that appropriate number is, and how best to execute on it.

ENDS