Izak Odendaal, Investment Strategist at Old Mutual Wealth

Early morning on 7 August 1974 – fifty years ago – New Yorkers noticed a strange sight on their famous skyline. A young French artist named Philipe Petit had snuck up onto the roof of the South Tower of the World Trade Center. Using a bow and arrow, he shot fishing line across to the North Tower, which his accomplices used to guide a tightrope between the two skyscrapers, then still the tallest buildings on earth. Petit carefully walked across six times with nothing but a balancing beam to assist him, the giant city awakening 400m below, and only summer sky above. It was an act that was at once crazy and captivating.

Walking a metaphorical tightrope remains a daily duty for most investors, though admittedly the stakes aren’t as high, nor is the backdrop as spectacular. It is a balancing act between the need for inflation-beating returns over time, and the risk that comes from equity investing. True, there are times when cash returns are high – in fact, South African cash currently yields 3% in real terms – but this rarely lasts as interest rates are cyclical. Therefore, wealth creation comes ultimately from investing in companies that grow their earnings in excess of inflation over time. Unfortunately, their share prices can be very volatile in the short term. This trade-off between short-term volatility and long-term growth never really goes away. And while it sounds simple in theory, in practice the emotional response to falling prices often overwhelms the rational.

Don’t look down!

The events of the past two weeks are a case in point. Having ended the month of July on a high, global equity markets corrected sharply in the first few days of August. Several crowded trades, some of them leveraged, reversed sharply. Picture a small rowing boat where several occupants are sitting on the same side. It is unstable and at risk of tipping over as soon as it hits a wobble. Heading into August, popular trades included “short volatility” strategies, like the Artificial Intelligence (AI) theme (aka the Magnificent Seven), and the Japanese yen “carry trade,” a version of which involves borrowing cheaply in yen and investing elsewhere for a higher return. There is some speculation as to which of these is the real culprit, but what is ultimately important is that each amplified the shock on the others as they were being unwound.

Moreover, all of this happened during the Northern Hemisphere summer holiday, when liquidity is typically thinner.

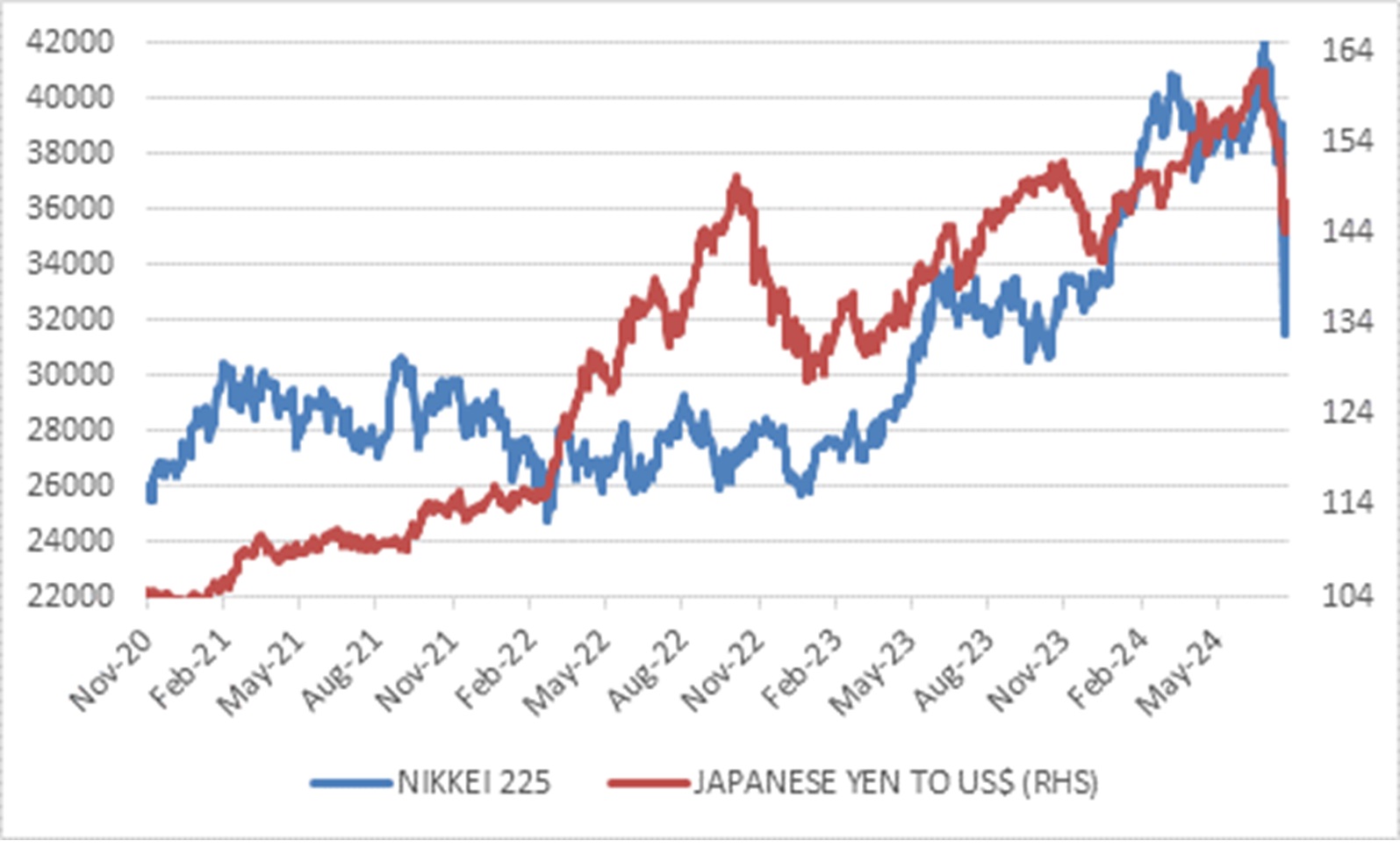

The biggest victim so far has been the Japanese equity market, where the Nikkei Index slumped 12% last Monday, the worst decline since Black Monday in 1987. The next day, it jumped 10%. Clearly, economic fundamentals did not change in the space of two days. But risk appetite swung massively.

Chart 1: Japanese equities and the yen

Source; LSEG Datastream

In fact, the October 1987 Black Monday crash is a useful example. In a well-known study, Robert Shiller, who later won a Nobel Prize for his work, sent a questionnaire to nearly 1 000 individual and institutional investors as the market was crashing. He found that respondents largely did not sell stocks in reaction to news or rumours, but basically sold because prices were falling amid a sense that the market was overvalued. Most investors interpreted the crash as a psychological reaction from other investors, and few pointed to a change in economic fundamentals as the reason for the sell-off as it was happening. Of course, after the fact, there were many rationalisations from amateurs and professionals alike, as well as hearings in Congress. But in the end, Professor Shiller’s work showed simply that selling begat selling.

Slowdown versus slump

Returning to the idea of the crowded and imbalanced rowing boat, in the end it doesn’t really matter what causes it to capsize, since it is a near-inevitability. To switch metaphors from water to fire, when there is much dry kindling about, a spark from any source can ignite a blaze.

In this instance, however, the nature of the spark does matter, since it concerns growth prospects for the US economy. If the US was to enter a recession, it would have a much greater market impact than the volatility of the past two weeks.

Here’s what we know. The US economy is slowing, which is perfectly normal after a period of strong growth. To put it slightly differently, when unemployment is already near record lows, it can really only rise. However, nothing screams recession or a substantial rise in unemployment yet.

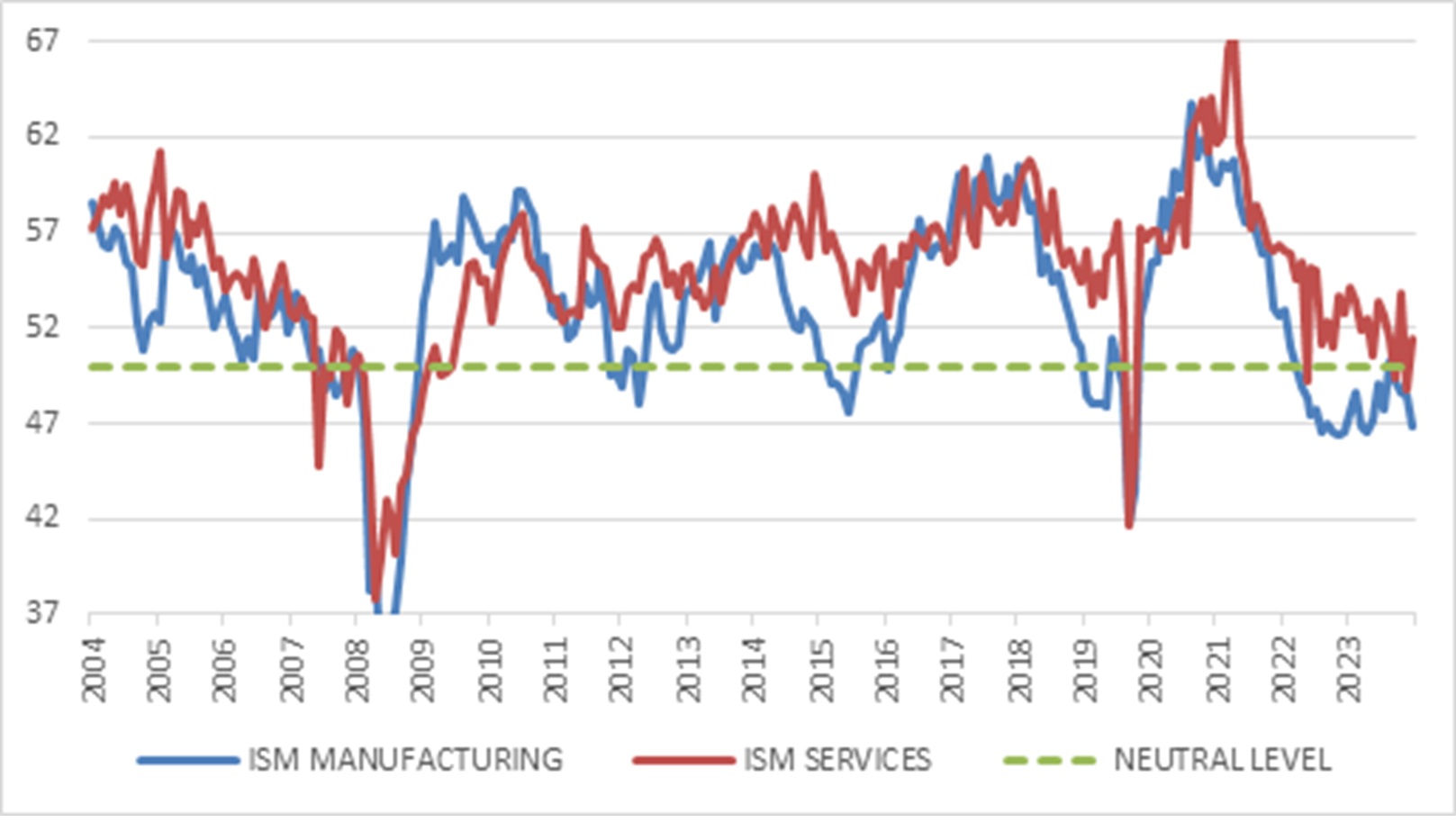

It was weak manufacturing data from the Institute of Supply Chain Management (ISM) that ignited the August growth scare, but the latest services ISM Index, covering a much greater portion of US economy activity, was in positive territory above 50 points though clearly not as strong as a year or so ago. Similarly, though the US government’s monthly labour market report for June was weaker than expected, one should never draw big conclusions from a single data point. These are often revised later, and any single monthly number can be subject to noise. A broader range of labour market indicators tells a story of a slower pace of job creation and less job switching, but no surge in layoffs. Slower wage growth does imply slower consumption growth, but it also reduces upward inflation pressure – a positive from the Federal Reserve’s point of view.

Chart 2: US ISM indices

Source: LSEG Datastream

How does the Fed react to all of this? It is also walking a tightrope of sorts. It needs to respond based on how it sees the economic outlook evolving, not on market moves. Equity volatility by itself is no reason to rush into cutting rates. In fact, the emergency rate cuts some have called for might even worsen the sense of panic. Central banks also shouldn’t reinforce the impression that they will always bail out investors who’ve made bad bets, creating what economists call moral hazard, though it might be a bit late. The idea of a “Fed put” (that the Fed will always backstop markets) is by now well ingrained.

Nonetheless, central banks also shouldn’t let panicky investors run riot. Sustained market volatility can negatively impact business and consumer confidence. Most people don’t follow market movements closely, but if the newspapers headlines are bad day after day, they might start getting worried. More importantly, market stress could lead to a tightening of financial conditions, in other words, rising borrowing costs for households and corporates. This could accelerate the economic slowdown, the extreme example being the 2007 credit crunch that turned into the 2008 Global Financial Crisis and ultimately the Great Recession.

However, as investors rushed into the safety of bonds, prices rose, and yields fell. These lower bond yields imply lower borrowing costs for a range of borrowers. Mortgage rates, for instance, have declined to the lowest level in more than a year, as chart 3 below shows, while borrowing costs for riskier “high yield” companies have inched lower, instead of spiking higher as in 2020. However, in all cases, these rates are still elevated compared to pre-Covid levels.

Chart 3: Borrowing costs for US companies and households, %

Source: LSEG Datastream

In other words, all Fed officials need to do at this stage is send a clear message that they will be cutting rates, aggressively if necessary. The market will do the rest. However, it also implies that if the Fed ends up cutting by less than expected – for instance if inflation remains uncomfortably sticky – there could be more market ructions. The other big risk remains whether a gradual slowdown in US economic growth snowballs into something worse.

Resilient rand

Looking at things back home, it notable that South African investments have held up relatively well. Usually, South African assets are “high beta” to global markets, meaning they fall by more in times of stress.

The rand, in particular, is basically flat against the dollar in 2024, almost unheard of in a time of global market anxiety. This, together with looming cuts by the Fed means the SA Reserve Bank should have the confidence to start lowering the repo rate at its next meeting.

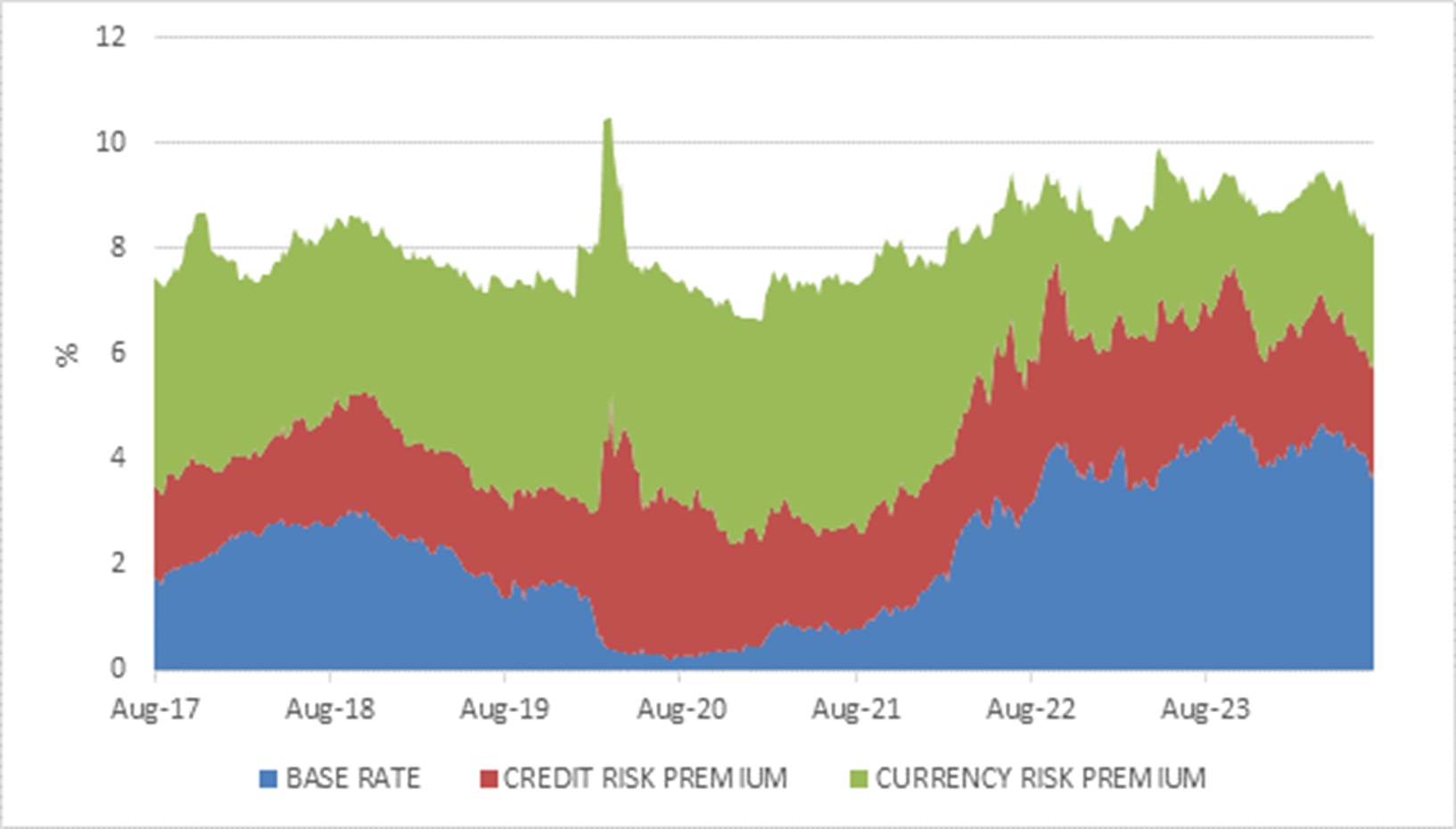

South African government bond yields have also declined, partly because of the fall in global yields, but also because the credit risk premium on South African bonds is lower since the formation of the Government of National Unity and its commitment to sensible economic policy. Without getting into the technical details, we can measure credit risk premium, how creditworthy the government is perceived to be, by dollar credit default swaps (CDS). A lower value is better. Chart 4 decomposes the 8.3% yield on a rand-denominated five-year South African government bond into a global dollar risk-free or base rate (the US Treasury bond yield), the credit risk premium (SA dollar CDS) and a currency or inflation premium. All three elements are lower in recent weeks.

Chart 4: SA 5-year government ZAR bond yield decomposed

Source: LSEG Datastream

One step at a time

Tightrope walking is also known as funambulism, and when done in the outdoors between buildings or across gorges, is known as a skywalk. A skywalker faces two great dangers. The one is environmental conditions, such as a gust of wind. The second is overconfidence, leading to a failure to prepare. One of the most famous skywalkers, Karl Wallenda, whose feats included crossing the deep Tallulah Gorge in Georgia, fell to his death in 1978 attempting to walk between two 10-story buildings in Puerto Rico. An improperly secured rope was blamed afterwards.

In a similar way, periods of market calm can lead to complacency and the ratcheting up of risk-taking. Sometimes, investors don’t even realise they are taking on more risk. Stability breeds instability, but instability breeds resilience. Therefore, as stressful as these kinds of market corrections can be, they also serve a useful purpose.

Unlike Petit or Wallenda, investors do have options for protection. These range from very explicit strategies that use derivatives to hedge against declines or guarantees from a life company, to simply tilting an asset allocation heavily to cash. A diversified asset allocation does not avoid market volatility altogether but offers balance. It remains difficult to completely avoid the trade-off between risk and return, however.

Another way to add some protection to a portfolio is by avoiding things that are overvalued. Needless to say, the higher the tightrope is strung, the harder the fall if something goes wrong. The recent sell-off showed how the more richly valued assets, such as the tech superstars tumbled further than the more modestly priced ones. Purely speculative investments like Bitcoin lost 20% at the drop of a hat. Importantly, though, whether something is cheap or expensive, doesn’t mean anyone can predict when the price will correct up or down. The timing of these events is not knowable in advance.

As investors, we also thankfully have a larger margin for error than skywalkers, since time heals many wounds. Markets usually recover from big selloffs, however how long it takes depends on the extent of the decline and economic conditions. Usually what turns a correction into a prolonged bear market is a recession in the US. Therefore, the US economic outlook remains key. Nonetheless, the recovery time after a market decline also depends a lot on how investors respond. Selling out into cash after the equity market has fallen locks in losses. It is highly unlikely that cash will outperform equities after the market has fallen.

In the end, just as tightrope walkers look ahead, not down, investors should remain focused on the end goal, and not get swayed by short-term volatility.

ENDS