Izak Odendaal – Old Mutual Wealth Investment Strategist

Is 2024 the year of geopolitics? It certainly feels as if risks lurk around every corner, and investors are bombarded by scary headlines daily. Of course, that is much better than being hit by actual bombs, something we’ve seen not only in Gaza in recent weeks but also in other parts of the Middle East, including the Red Sea, Iran, Iraq, Pakistan and Jordan. The ongoing loss of life is tragic, and we must ask whether these separate but interrelated conflicts are escalating to a point where the global economy is severely impacted.

The obvious place to start is the Red Sea, a major maritime channel where attacks by Iranian-backed Houthi rebels are forcing many ships to take the longer and costlier route around the Cape (sadly with little benefit to the South African economy). About a third of the world’s shipping containers usually flows through the Red Sea and the Suez Canal, a route that connects Europe with China and the rest of Asia.

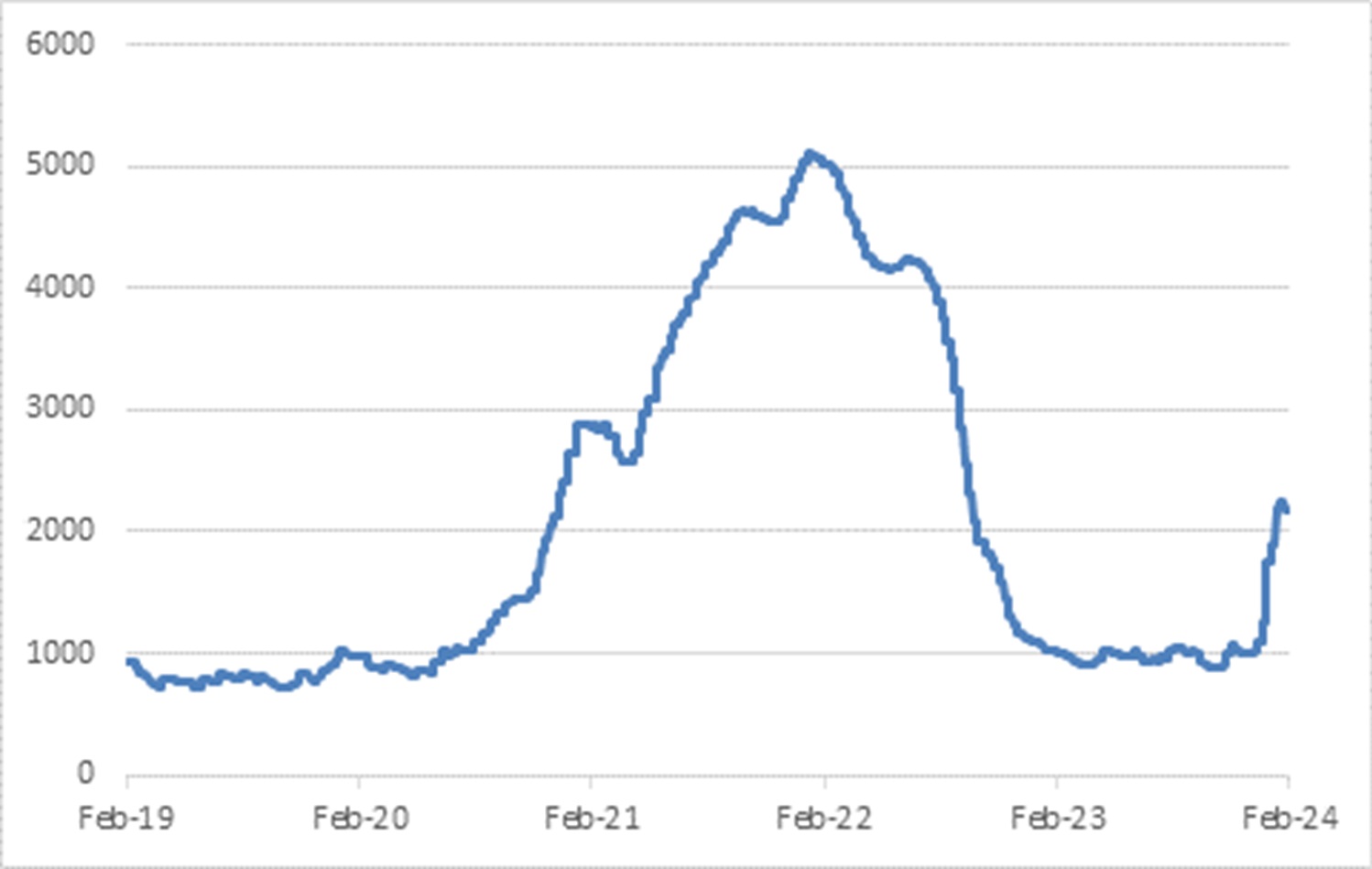

The memory of the worldwide supply-chain snarl-ups of 2021 and 2022 and associated surge in inflation is still fresh. Will we see another jump in goods prices as shipping costs rise? Possibly, but as Chart 1 shows, the increase in shipping costs is not as big as during 2021. The disruption is only on one (albeit important) shipping route. Trade across the Pacific is unaffected, and unlike during the pandemic, operations at the world’s major ports are running smoothly.

Chart 1: Shanghai Freight Cost Index

Source LSEG Datastream

Secondly, higher shipping costs by themselves do not equate to inflation. Remember that inflation is not a one-off increase in the price of some goods or services. It is a sustained process where price increases in one corner of the economy lead to price increases across a broad front elsewhere. It is not the first round of price increases – whether it is freight rates, fuel prices or a shortage of eggs – that matters as much as whether firms will raise selling prices to consumers in response to higher input costs. In 2021/22 they did so en masse and across the globe. That was partly because demand for goods was so strong due to pandemic-related shifts in consumption, but also because they had an excuse, namely that everyone else was doing it.

In today’s environment, it is harder to make a case for the same thing happening. Goods inflation is running close to zero, and consumers will not necessarily tolerate higher prices. And while economic growth in the US is solid, Europe is skirting recession and China is still weak.

There is one country for which this is a massive blow. For Egypt, revenues from the Suez Canal is a major source of hard currency in an economy that is perpetually short (hence the need for a $3 billion IMF bailout in 2022). This already hints at the complexity of the politics of the region. While there is sympathy for the Palestinian cause across the Arab world, there isn’t broad support for the actions of the Houthis.

Oil spotting

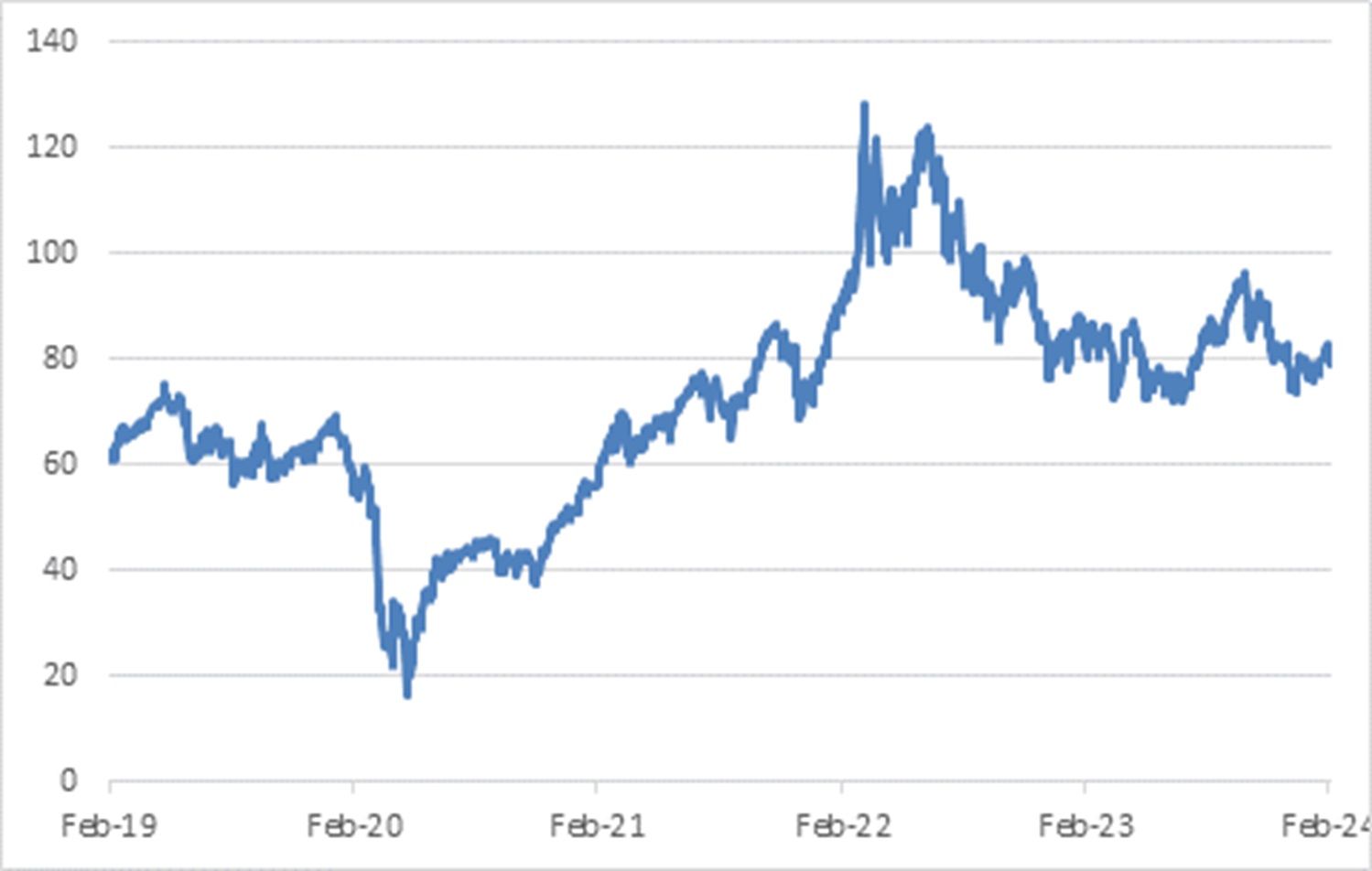

The second key area to monitor is the oil price. Oil is the main reason the Middle East matters to the world economy (a fact that ambitious leaders in the UAE and Saudi Arabia is trying to change by diversifying their economies).

The deadly attacks on American soldiers in Jordan (the work of another Iranian-backed group) saw the oil price jump above $80 per barrel, but only briefly. A full-scale war between Iran and the US would see a devastating price spike, but both sides have reined in the rhetoric in recent days. Neither side really wants war. The US has barely extricated itself from long and costly conflicts in Iraq and Afghanistan, while war would crater Iran’s already-weak economy and probably undermine its’ rulers grip on power.

All in all, the oil price remains well behaved, unlike in the wake of Russia’s invasion of Ukraine in early 2022. This is partly because American oil production is at record levels, and partly because global oil demand has been softer than expected. This means the broader global economy is not really affected.

Chart 2: Brent Crude oil, $ per barrel

Source: LSEG Datastream

Flashpoints and fault lines

In thinking about geopolitics, it is helpful not to focus exclusively on the current flashpoints (like the Middle East or Russia’s assault on Ukraine) at the expense of the bigger picture. The 20 to 30 years that followed the collapse of the Berlin War saw the reintegration of the former Soviet Bloc and China into to global economy, while many other countries cut tariff barriers and embraced free trade. Multinational firms spread their operations far and wide to where production costs were lowest. All of this was underpinned by the American security blanket, the dominant role of the US dollar, and a belief that democracy and free markets would ultimately prevail.

However, for better or worse, this era of so-called hyper-globalisation is over. American leadership is being challenged. China is asserting itself on the global stage, particularly in its own back yard. So is Russia. Other developing economies have shifting allegiances (like the BRICS grouping). Deliberate attempts are being made to shift away from the dollar. A multipolar world is emerging. Countries are increasingly focusing on national security issues, while companies look for suppliers closer to home in countries that are considered friendly. Industrial policy – government support for key industries and ‘national champions’ – is back with a bang on both sides of the Atlantic and the Pacific.

A Donald Trump victory in November’s US presidential election would likely accelerate these trends, as he has made it clear that he will withdraw from some of America’s multilateral obligations, hike tariffs on imports from China (and elsewhere) and halt funding to Ukraine.

In other words, geopolitics will be a noisy and messy feature of our lives in the years ahead. Investors need to have a framework for thinking about these things. One consideration comes from Macquarie strategist, Victor Shvets, who argues that geopolitics is a process, not an event. The event (like the Houthi attacks on ships) is what will grab the headlines, and the headlines will make some investors panic. However, this is usually short-lived volatility. More important are the trends that sit underneath the surface. As a rule of thumb, people often overestimate short-term implications of these developments and underestimate the long-term consequences.

For instance, the combination of globalisation and technological advances put downward pressure on prices for much of the 1990 to 2020 period, keeping inflation and ultimately interest rates low. We don’t know what the world will look like 30 years from now, but we definitely can’t take it for granted that it will look like the previous three decades.

Or a more specific example: equity markets fell sharply after the 9/11 attacks but rebounded within a matter of months. The impact on the US economy was minimal. However, the US then launched two costly wars, squandering not just trillions of dollars, but also its credibility.

It’s in the tails

This doesn’t mean that the events are meaningless. A full-blown war between the US and China over Taiwan would be directly and immediately devastating to the global economy, but it is also a very unlikely outcome. It is just very difficult to position a portfolio in anticipation of such a very specific, low probability-high impact (tail risk) outcome.

It might never happen (let’s hope) or happen only much later or unfold in a completely unexpected way. The general principle remains having broad diversification in a portfolio with enough exposure to the upside – after all, the human capacity for inflicting harm on one another is more than matched by its capacity for innovation (in fact, ironically, wars often turbocharge technological development that makes its way into day-to-day use) – but also defensive assets that offer downside protection.

The risks within

Finally, it is worth remembering that in modern times most instances of catastrophic wealth destruction have not been due to geopolitics or war, but rather due to the unsustainable build-up of imbalances within the financial system.

There are several categories, the worst usually being a dangerous surge of private debt linked to real estate, most notably the 2008 Global Financial Crisis, which saw global equity values halve, while house prices also fell sharply in many countries and several large banks failed. China might well be going through a slow-motion replay of this movie. Another category is the so-called “original sin” of emerging markets, where too much borrowing is done in hard currency, exposing the domestic financial system to a currency mismatch. Nigeria has just devalued its currency by 40%, the right thing to do to attract capital and finally address the chronic hard currency shortage, but obviously a massive blow to Nigerians who have dollar liabilities.

A third category is the old-fashioned bubble. Investors are gripped by a narrative of unending growth in some country, sector, or asset class. As they pile in, values rise and more investors are attracted. Eventually valuations completely diverge from reality and the only way anyone can make a profit is to sell to the “greater fool”. Speculators who buy at the top will suffer huge losses. If they used leverage, they are wiped out. The Japanese equity market experienced an epic bubble that burst in 1989 and is only now finally closing in on that record high – 34 years later. But you don’t need a bubble to lose money. Overpaying for any asset can be detrimental to your wealth, which is why investors should pay attention to valuations – and look for investments where there is a sufficient margin of safety.

Chart 3: Long road back to the top for the Nikkei

Source: LSEG

A fourth category is simply inflation, which erodes wealth much more insidiously, but can do so just as thoroughly as a crash. As noted above, inflation is a complex phenomenon, but it tends to be more severe in countries with weak domestic institutions and counterproductive policies – Argentina comes to mind immediately, with its 211% current inflation rate, as does Zimbabwe, which experienced hyperinflation not that long ago.

In other words, we should spend as much time monitoring financial sector developments as we do analysing geopolitical fault lines. A rising interest rate cycle is a particularly vulnerable moment for the financial sector in any jurisdiction. To quote Warren Buffet, you can see who has been swimming naked when the tide goes out. The good news is twofold. Firstly, there don’t appear to have been too many major instances of skinny-dipping, remarkable given how interest rates were very low for a very long time. A handful of emerging markets have defaulted on hard currency debt (Zambia, Sri Lanka, Ghana) and a few banks have failed, notably the storied Credit Suisse. But the broader banking system has so far come out relatively unscathed. Secondly, the rate cycle has peaked. There is still uncertainty over when rates will fall and how fast – the US Federal Reserve pushed back against expectations for a March cut at its policy meeting last week – but the direction of travel is clear, including in South Africa.

In summary then, there are big tectonic shifts underway in the geopolitical landscape, and as any high school geography student can tell you, tectonic shifts lead to tremors, earthquakes, or volcanic eruptions. These tensions will be a source of uncertainty for investors for the years ahead. It could lead to slower economic growth, and, at worst, to crises, recessions, and wars. But we should not pretend that we can predict when, where and what will happen. The worst thing to do – especially in this age of rampant disinformation – is to make investment decisions based on hype, fear or simply misunderstandings. There will be opportunities to make money in this uncertain emerging new world order, and a calm, measured approach will remain key to doing so.

ENDS