Izak Odendaal, Investment Strategist at Old Mutual Wealth

The unexpected recent passing of former Reserve Bank Governor and Finance Minister Tito Mboweni robbed South Africa of one of its most distinguished policymakers and most colourful public figures. Aged only 65, he still had a lot to offer. Tributes have rightly poured in from all corners, and there is no need to repeat those here. It does, however, provide an opportunity to consider the policy framework he helped build and assess its performance, especially ahead of next week’s Medium-Term Budget Policy Statement (MTBPS).

Mboweni’s first stint in government was as labour minister, between 1994 and 1998. He was instrumental in setting up a labour market architecture that gave workers real rights for the first time. However, many years later, Mboweni questioned whether the pendulum had not swung too far, with labour laws being too rigid, discouraging hiring.

It was as Reserve Bank Governor that Mboweni really made a name for himself. Despite his self-described radical leftist background, he ultimately became the quintessential central banker, and a hawk on inflation. The fact that he was able to make the switch says a lot about his own intellectual strength and flexibility, but that was also true of many of his generation of leaders who were often staunchly socialist but ended up embracing orthodox macroeconomic policies. For instance, the Reserve Bank’s independence was enshrined in the Constitution in 1996, fairly unique by global standards.

It also says something about how strong institutions, like the Reserve Bank, mould their leaders as much as the other way around. This is an encouraging thought given that South Africa has now fully entered the age of coalitions, and there might be greater unpredictability in who is appointed where in the years ahead.

As an aside, the vital role of institutions in economic growth and prosperity was acknowledged when Daron Acemoglu, Simon Johnson and James Robinson were awarded the Nobel Prize in economics last week. Institutions include organisations or agencies like the Reserve Bank or Constitutional Court that have a clear role to play in society and the economy, but also more informal sets of rules and conventions that limit overreach by powerful actors (notably the state). This supports the stable and predictable environment in which markets can function and scarce resources are allocated.

On target

Under Mboweni’s watch, the South African Reserve Bank (SARB) followed other central banks in adopting inflation targeting as its policy framework in 2000.

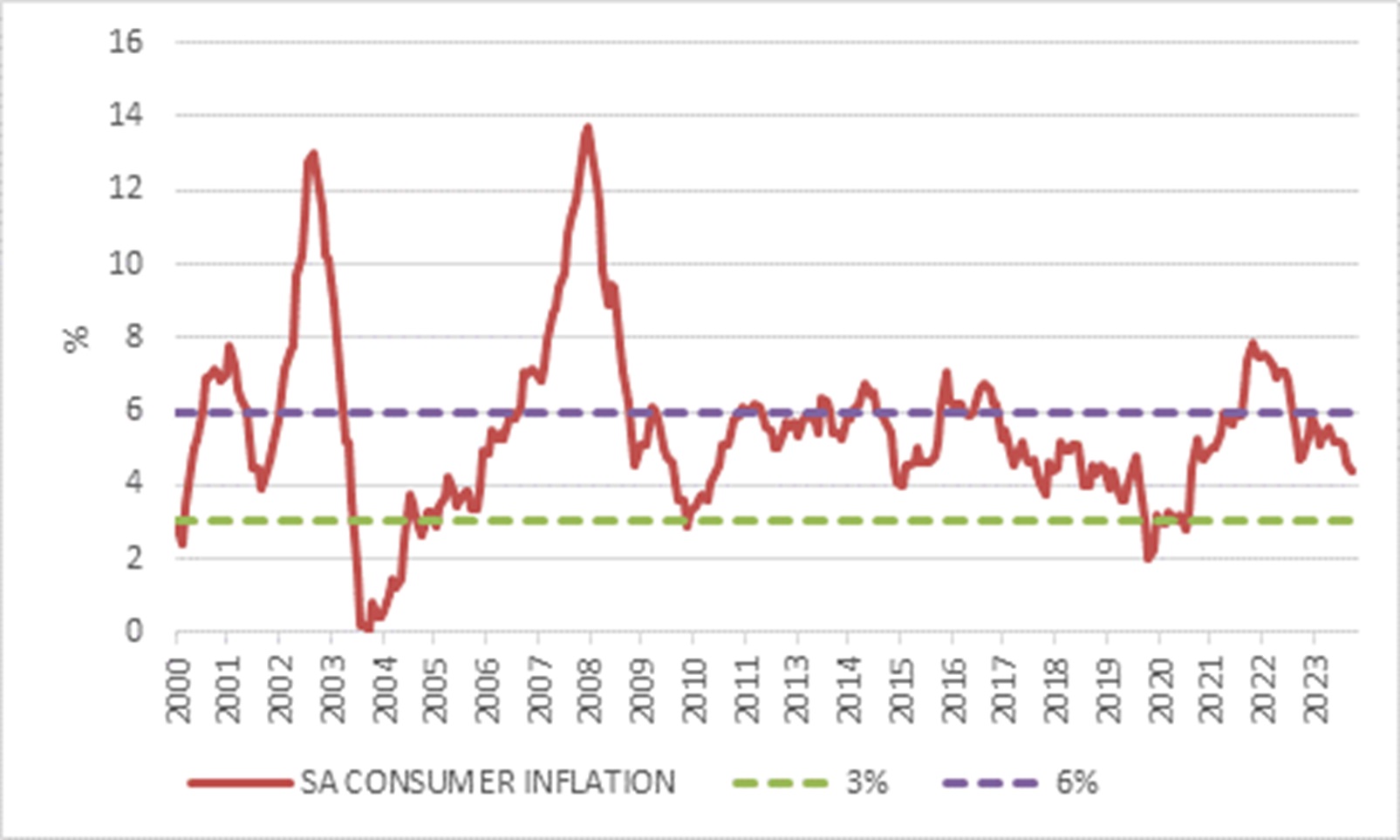

Inflation targeting has been mostly successful. On average, inflation has certainly been lower in the 25 years after 2000 than the prior quarter of a century. On average, it has also been in the target range, but the 5.8% average has been close to the top end. There were also notable spikes above 6%. Since we can’t run controlled experiments, it’s impossible to say whether inflation would be lower on average under a different policy framework.

Chart 1: South African inflation

Source: LSEG Datastream

What we can say is that inflation targeting has given the general public an inflation number to anchor on, which influences what it expects future inflation to be and how to respond. The trick now is to get that anchor lower, so that people believe average inflation in future will be lower, impacting their pricing decisions. To this end, the Reserve Bank explicitly started talking about the 4.5% midpoint of the range in 2017, to get the anchor down from 6%.

At some point in the future, it wants to lower the target further, probably to 3% where most of our emerging market peers are. It is the government, not the Reserve Bank, that sets the target, but the Bank might start subtly introducing the idea in its communication before government formally approves a change.

In a speech at Stellenbosch University last week, the current Governor, Lesetja Kganyago noted that South Africa and Chile adopted inflation targets around the same time. Chile chose 3% and South Africa a range of 3% to 6%. He argued that the lower target in Chile resulted in inflation running 1.8 percentage points lower on average than in South Africa. This means that the price level in Chile is 2.8 times higher than in 2000, while ours is 4.5 times higher.

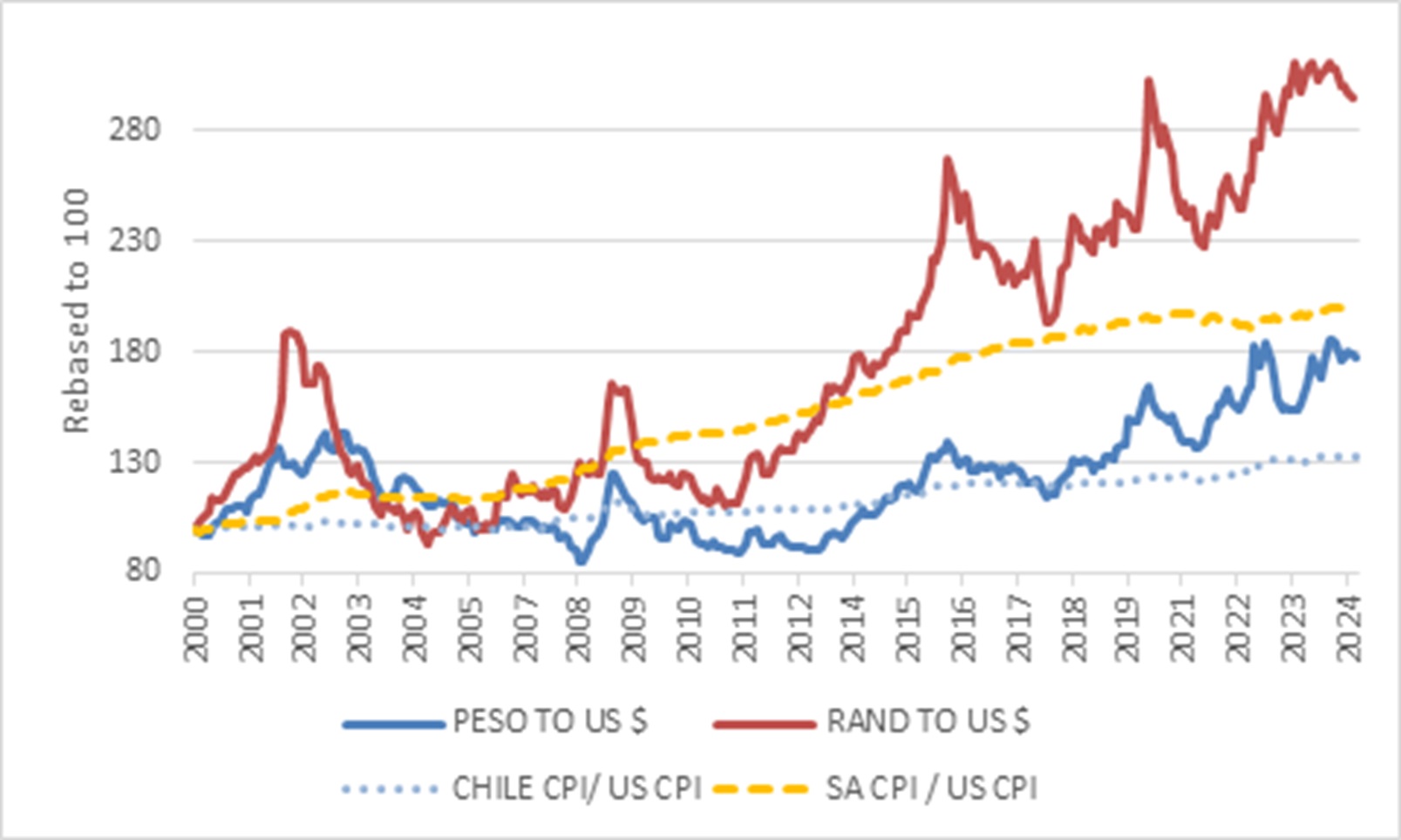

Chart 2: Exchange rates and inflation differentials

Source: LSEG Datastream

The theory of purchasing power parity suggests that higher inflation relative to trading partners results in a weaker currency over time. While there are other factors in play, it is notable that the rand weakened by two percentage points more against the US dollar than the Chilean peso did over this period. The rand has in fact weakened by more than what inflation differentials would suggest.

Governor Kganyago, who is also on the hawkish side, therefore argued that the economy’s average inflation rate is ultimately a policy choice, implying that we should now make the choice to have sustained lower inflation rates in future. While getting inflation down to a new, lower target implies somewhat higher interest rates in the shorter term, it would ultimately allow for lower interest rates over the longer term. Kganyago firmly believes the short-term pain would be justified by the long-term gain, but he also argued that recent experience showed that the cost of moving to a lower inflation rate – the ‘sacrifice ratio’ of foregone economic growth – is not necessarily as high as many think.

Jaws

Mboweni became finance minister in 2018, at a time when South Africa had largely lost fiscal credibility after the state capture years. The wage bill was threatening to spiral out of control and the rash decision to fund free higher education added billions in unexpected costs, while bailouts for underperforming state-owned entities continued to swallow billions more. A weak economy simply was not delivering the tax revenues needed to cover all these costs

True to style, Mboweni used a simple metaphor to describe the problem: the gap between government spending and government revenue had widened like the jaws of a yawning hippo. Action was needed to close the jaws again, since the gap was financed by borrowing at high interest rates which is unsustainable. The gap be closed through faster economic growth and fiscal discipline, which could ultimately get the country its investment grade credit rating back.

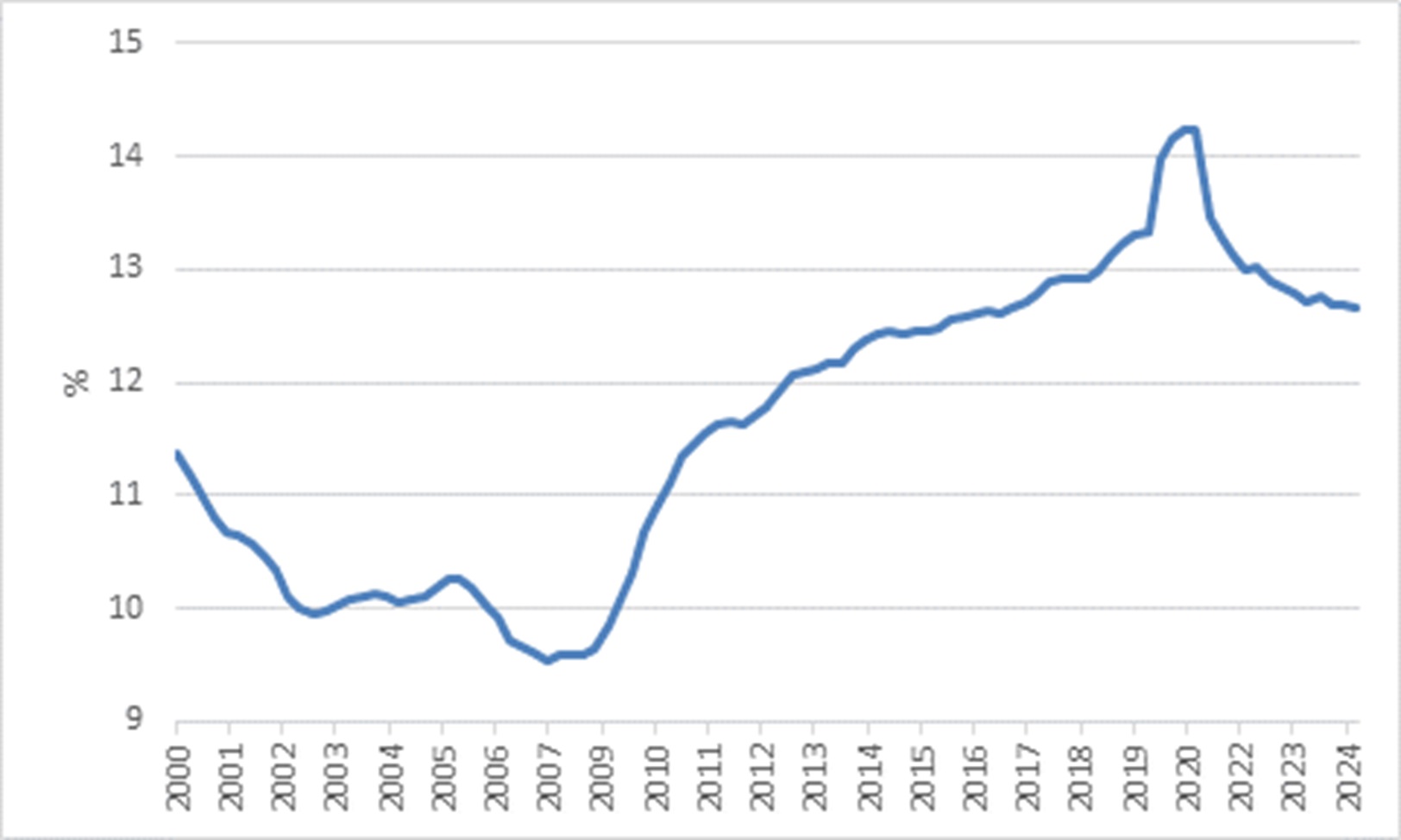

In terms of fiscal discipline, the big success of Mboweni and his successor Enoch Godongwana has been in stabilising the government’s salary bill after its rapid rise from 2009. Future public sector wage negotiations will be contentious and pose a risk to the budgeted numbers, but Godongwana is likely to hold the line.

Chart 3: Government compensation of employees as % of GDP

Source: LSEG Datastream

In terms of tackling the obstacles to faster growth, Operation Vulindlela (OV) was established by Mboweni and President Ramaphosa as a joint Treasury-Presidency task team to do exactly that, working across government departments to eliminate the barriers that discourage economic activity.

OV has a narrow mandate, focusing on a handful of key chokepoints in the economy, notably electricity, logistics, water, visas and mining licences. It has largely been successful, particularly with electricity, and will continue to operate under the government of national unity (GNU) with a new set of limited focus areas. It cannot and will not fix all the country’s problems, many of which sit with dysfunctional municipalities. However, by rolling the big boulders out of the way, it can clear the road for easier business conditions and more job creation.

OV predates the GNU. If economic growth does accelerate in the years ahead as expected, many people will associate it with the GNU. But the groundwork was laid well before the election.

Continuity

While the MTBPS will be the first post-GNU budget event, it will probably show continuity with the February Budget and its projections. So far this year, tax revenues are running somewhat behind target, but it is not particularly worrying. Spending is largely on track. Surprises are unlikely, and the focus will rightly remain on fiscal consolidation and growth-enhancing reforms.

Fiscal consolidation is where the feel-good factor of the GNU meets the cold hard reality. The government recognises that there is not much scope to squeeze more tax revenue out of a weak economy, particularly from strained consumers. Therefore, most of the emphasis falls on keeping a tight lid on spending, including the wage bill, but government departments have also seen their budgets cut. This impacts service delivery, which makes it politically difficult. But it will hopefully also force a far greater emphasis on efficiency and innovation in a state bureaucracy not known for those two characteristics. For its part, Treasury is pushing through. Here too, it is important to note that this started well before the formation of the GNU.

Its big achievement has been a primary surplus, which means that non-interest spending is now less than revenue. In other words, if we exclude interest payments, the jaws of the hippo have closed. However, while a primary surplus is the first step towards stabilising government’s debt ratio – around 70% of GDP and rising – there is still work to be done since interest payments now amount to almost R400 billion a year. Put differently, more than 20 cents of each rand SARS collects goes to debt service. Again, the solution is to borrow less, and at lower interest rates, and for SARS to collect more from a buoyant economy. This will be a slow grind, but we are moving in the right direction.

Chart 4: 10-year South African government bond yield, %

Source: LSEG Datastream

Finally, where the impact of monetary and fiscal policy meets is in the bond market. Bond investors are generally a pessimistic bunch, but two big fears stand out. The first is not getting interest payments or the capital repayment. This is known as a “default” and usually happens when the borrower is running out of money. Sound fiscal policy is meant to contain this risk. The second fear is a stealthy default, when inflation erodes the real value of interest and capital payments. The bond investor will try to price for inflation risk, but surprises do happen.

In South Africa’s case, the bond market was slow to recognise that inflation risk declined in the early 2000s, but bond yields eventually came down sharply, generating massive capital gains (bond prices rise as yields fall). Under the Jacob Zuma presidency, yields rose again. This time it was mostly reflecting deteriorating creditworthiness and rising default risk, not so much inflation worries.

The most recent rally in bonds reflects a more benign global environment, with lower inflation and interest rates in most major economies, but also that progress is being made in South Africa. Ultimately, the institutions that Mboweni helped to build remain a key source of strength when assessing South African bond valuations. The SARB is committed to achieving its inflation target and is likely to eventually adopt a lower target, limiting inflation risk for investors. National Treasury, for its part, is determined to reduce government debt levels and boost economic growth. This will take some time to materialise, but also suggests that default risk is lower than what is priced by the market. Therefore, bond yields remain attractive even after the rally and deserve a place in a diversified portfolio.

ENDS