Izak Odendaal, Investment Strategist at Old Mutual Wealth

To a year already packed with political intrigue, drama and a record number of elections, we can now add the sudden unexpected collapse over the weekend of the Bashar al-Assad dictatorship in Syria after years of violent stalemate. No one knows what lies ahead for Syria, ruled with an iron fist by the Assad family for five decades. Since the 2011 ‘Arab Spring’, civil war has raged in Syria and Assad’s regime was propped up by support from Russia and Iran. However, these two countries have been distracted by other conflicts, and rebels seized the opportunity. These events bring more uncertainty and potential instability to the world’s great geopolitical fault line, the Middle East. So far, the oil price, the main financial barometer of Middle Eastern tensions, remains muted.

Days earlier, we saw unbelievable scenes from South Korea, where the president tried and failed to impose martial law. It is not a large country and has a minimal impact on global markets apart from Samsung and a few large multinational firms, but South Korea has been a beacon of stability sitting atop another geopolitical fault line. With its nuclear-armed neighbour now involved in the Ukraine war, the last thing the world needs is chaos in the south. However, the country’s institutions have held up well, and it seems President Yoon Suk Yeol will be on his way out eventually.

Elsewhere, a budget stand-off in the French parliament led to Prime Minister Michel Barnier losing a no-confidence vote, the first time since 1962. This comes just a few weeks after the ruling coalition in Germany fell apart, also because of budget disagreements, leading to elections scheduled for early next year.

More debt, less debt

The difference between France and Germany is that the former has too much debt and the latter too little. France’s government debt-to-gross domestic product (GDP) ratio is 110%, while it is 62% in Germany, one of the few countries where the ratio has declined over the past decade. To address this, Barnier tried to narrow the French fiscal deficit through tax increases and spending cuts, while in Germany there were plans to increase borrowing to fund necessary investments in infrastructure, green energy and military capacity, that face opposition. A limit on borrowing, the so-called debt brake, is enshrined in the constitution, a sign of how seriously fiscal matters are taken in Germany. Nonetheless, releasing this debt brake to invest in the future is crucial for Germany’s longer-term economic health.

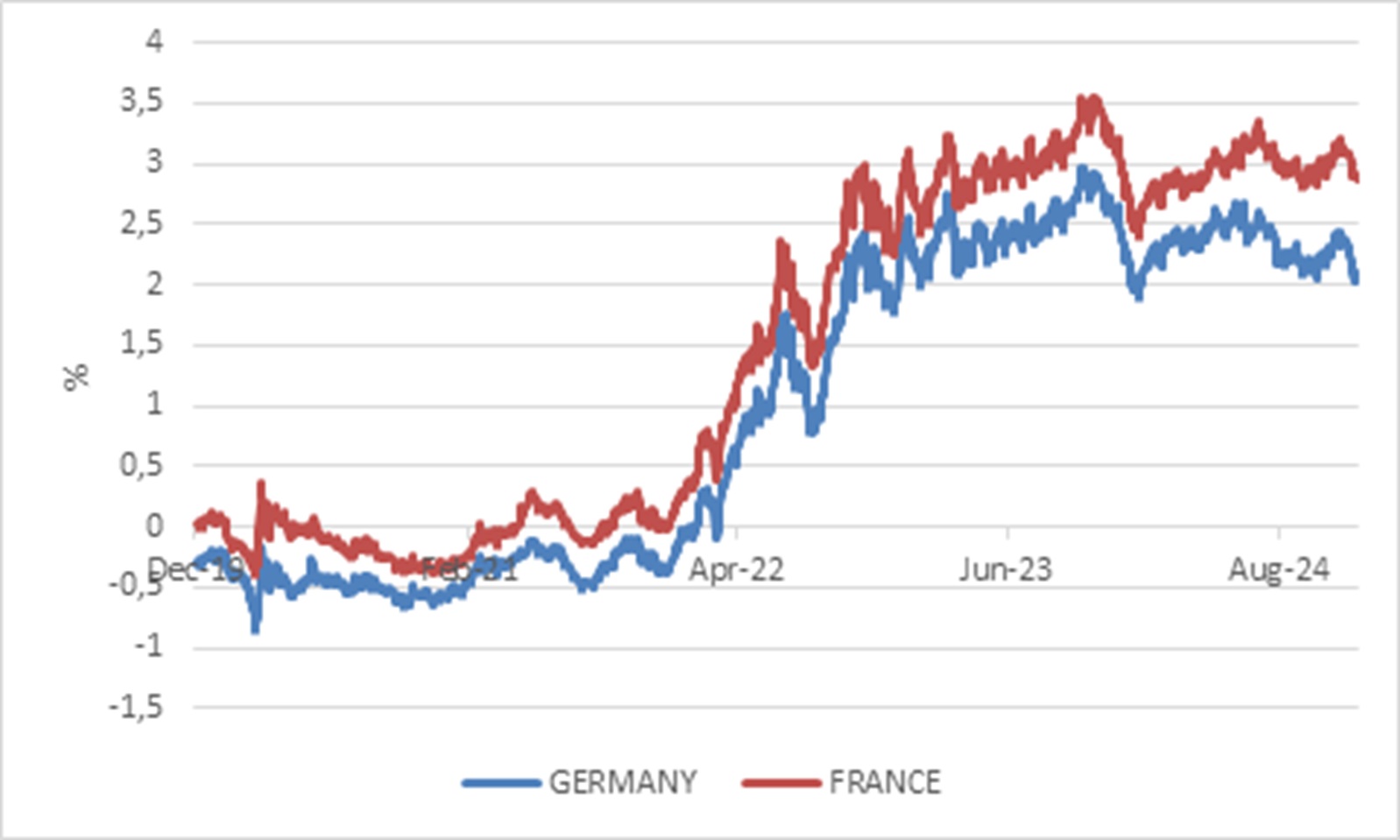

Chart 1: French and German 10-year government bond yields

Source: LSEG Datastream

The spread between French and German bond yields has therefore widened, uncomfortably echoing the Eurozone fiscal crisis of 2010-12. This comes at a time when the Eurozone economy, particularly Germany, is already under pressure and European leaders await Donald Trump’s second term with some trepidation. However, we are nowhere close to a fiscal crisis since French bond yields remain low in absolute terms around 3% and the French government can still easily fund itself. The risk of a chaotic breakup of the single currency, the fear underlying the crisis of a decade ago, has also diminished substantially since even the populist parties that have been as ascendent across the continent in recent years have no plans to abandon the euro.

GNU in context

All of this puts South Africa’s big political year in context. Though the May election result was unexpected, with the ruling ANC doing worse than expected, the formation of a centrist coalition, styled as a government of national unity (GNU), was also a surprise, a positive one from the market’s point of view. It is also worth highlighting again how important it was for the long-term credibility of South African democracy that the ANC immediately accepted the loss of its majority after 30 years in power. Violence is still simmering across the border in Mozambique where the opposition claims the election outcome was rigged. Things also didn’t go smoothly in Namibia’s recent election, but it has been peaceful, and the glass ceiling has been broken as Netumbo Nandi-Ndaitwah will become the first female president in Southern Africa.

The GNU was founded on a set of agreed core principles that include fiscal discipline, growth-enhancing economic reforms, and an adherence to the rule of law. There are obvious areas of disagreement between the ANC and DA, the largest coalition partners, including contentious health and education acts (NHI and BELA). But there is also a strong incentive for all parties to make it work, at least for now. Whether it lasts the full five years remains to be seen, especially since the local government elections in 2026 could alter the political landscape, followed by internal ANC elections in 2027. However, a lot can be done in two years to cement crucial and long-lasting economic reforms. The progress in stabilising Eskom’s operational performance and restructuring the electricity market has already had a major impact. There has not been nationwide loadshedding since March.

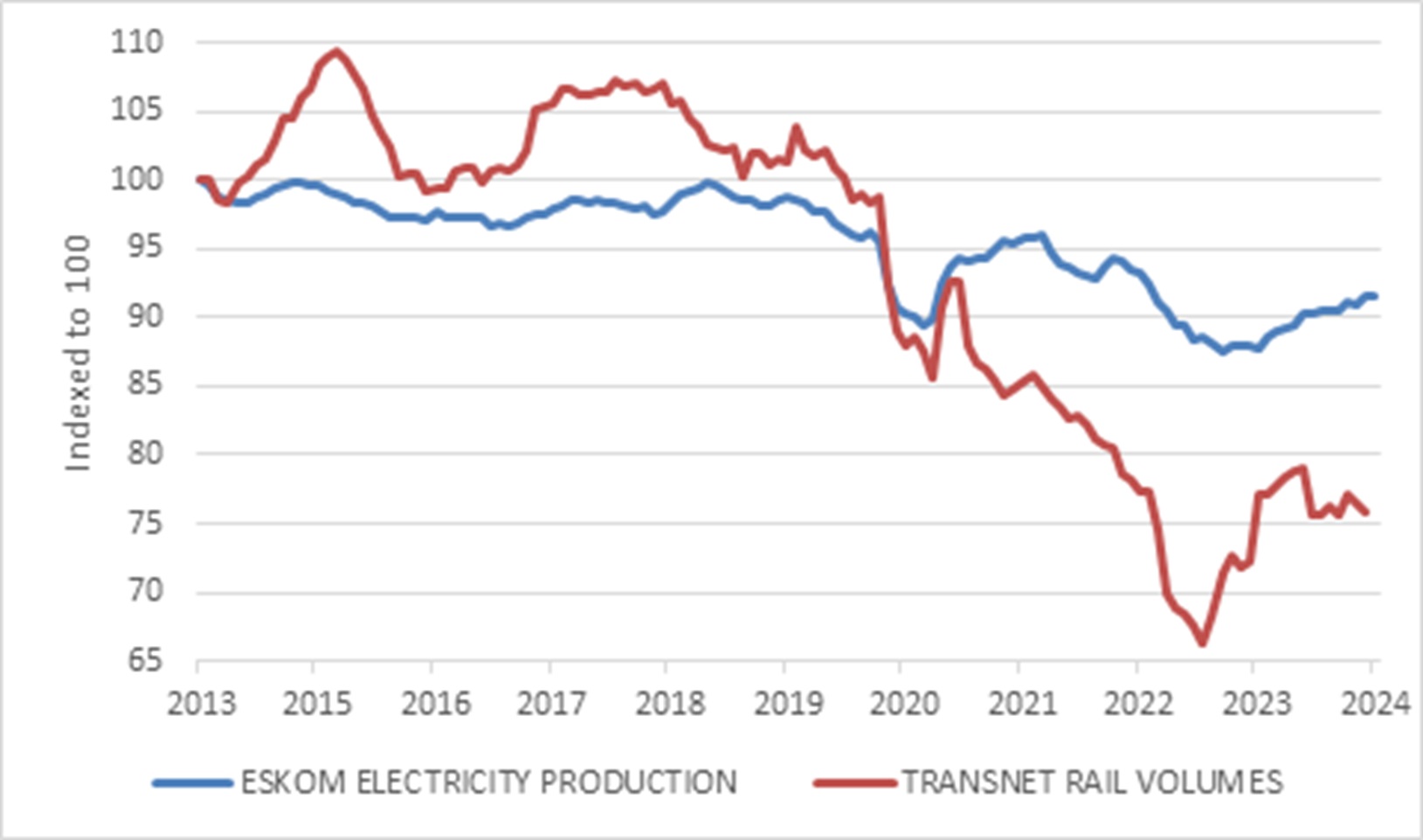

The next key area of reform should be logistics, and 2025 must be the year where there are not only ongoing operational improvements at Transnet, but tangible evidence of private sector participation in rail and ports. Deals need to be signed, concessions issued, and wheels must hit the steel. This will be crucial for the economy’s performance and for investor confidence.

Chart 2: South Africa’s electricity and logistics delivery

Source: Stats SA

Apart from electricity and logistics, water has emerged as the next frontier of economic crisis. This is largely a localised problem, centred on weak municipal performance. But if water runs out in the largest city, Johannesburg, it is a headwind for the whole economy. The private sector can also get involved in running bulk water systems. So much precious water is lost through theft and leaks (euphemistically called “non-revenue water”) that private investment in infrastructure can pay for itself.

As in Germany, South Africa needs to spend more on infrastructure, but the bulk of this spending needs to come from the private sector as government’s finances are constrained. This means creating a regulatory, financial and operational environment that attracts private capital from home and abroad. 2025 must see more progress on this front.

As in France, fiscal consolidation is necessary. In fact, though the South African government has less debt relative to the size of its economy (about 75% of GDP) than its French counterpart, it pays almost three times as much to borrow money. Even after a rally in South African government bonds this year, the 10-year yield is still elevated at 9% (bond yields and prices move in opposite directions). The market is still demanding a premium for lending to South Africa and will continue to do so until there is evidence of stabilising debt and accelerating economic growth.

The progress to date has been noticed, however. Ratings agency S&P Global raised the outlook on the rating of South African government debt from ‘stable’ to ‘positive.’ Its rating is still three notches deep into ‘junk status’ at BB- on foreign currency debt, so there is a long way to go to retain an investment grade rating (BBB or above), but this is the first step. S&P Global recognised ongoing efforts to reduce government borrowing and the improved economic outlook, expecting GDP growth to average 1.4% over the medium term. This is still lower than many other forecasters (including the Reserve Bank) but points in the right direction. It noted that the government of national unity (GNU) has improved political stability and that the increased “impetus for reform” should boost private investment and economic growth.

Their competitor, Moody’s, has not been so generous, and last week maintained the outlook on its rating of South African government bonds at ‘stable’. However, Moody’s expects a gradual increase in real economic growth to 1.7% by 2026, and a stable government debt burden at around 80% of GDP. It expects the GNU to continue implementing structural reforms to ease growth bottlenecks. It also notes South Africa’s strong institutions such as the judiciary and the central bank, its deep financial sector and lack of foreign debt. However, it also acknowledges challenges posed by the country’s “extensive inequalities” which make reforms difficult and increase social risk.

Farming fiasco

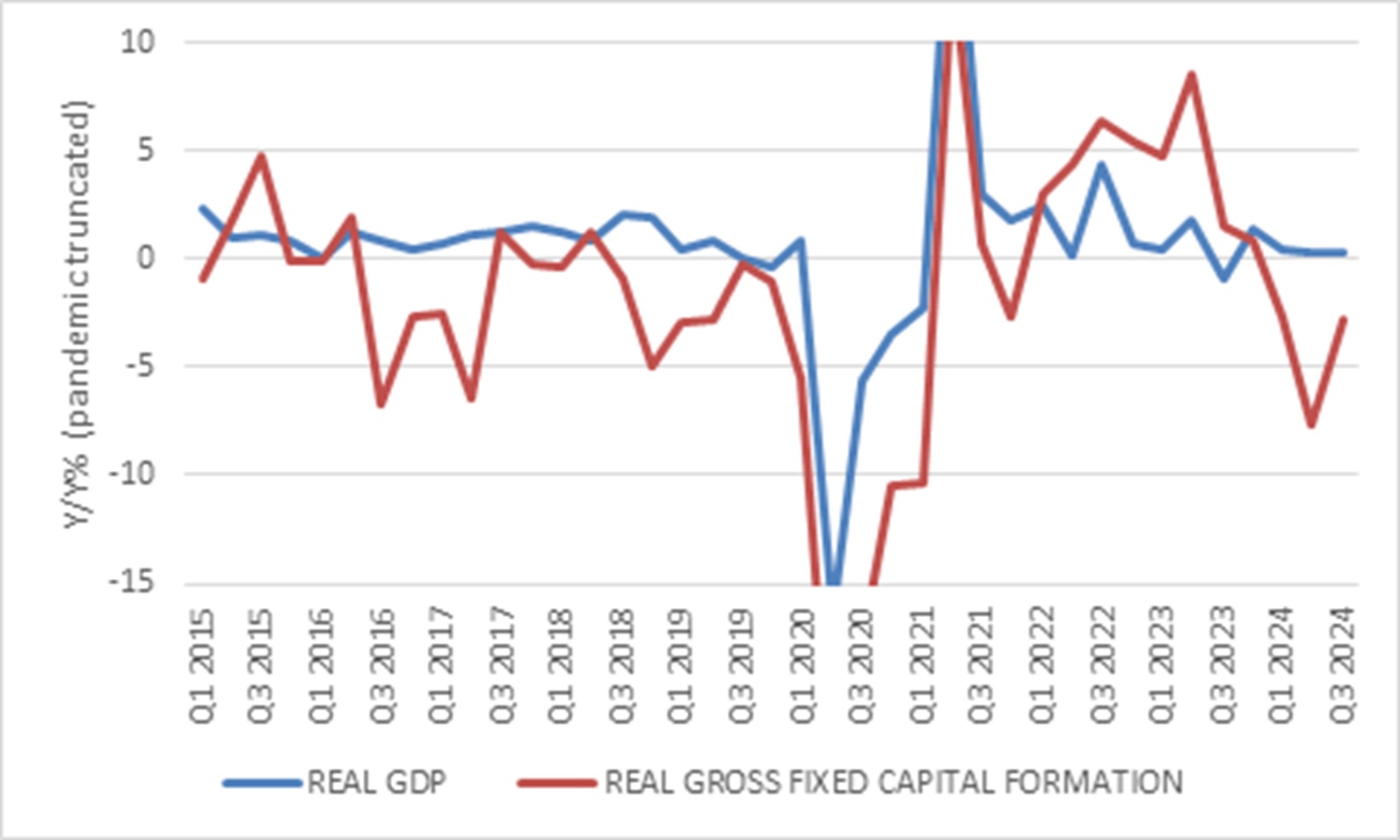

It is against this backdrop that the third quarter growth number was such a disappointment. According to Stats SA, third quarter GDP declined by 0.3% quarter-on-quarter in real terms, while the consensus expectation was for modest growth. The year-on-year growth rate was only slightly positive at 0.3%.

The negative surprise was due to a 29% decline in agricultural value add in the quarter, which more than offset the positive growth in the rest of the economy, even though farming is a small sector. Agricultural experts have questioned the extent of the reported contraction, which means this is probably another case where we don’t want to read too much into a single data point. It is probably more noise than signal.

Excluding agriculture, the GDP report contained good news and bad news. On the negative side, fixed investment growth remains disappointing. However, it is too soon after the formation of the GNU to expect companies to have not only committed to big spending plans, but to start implementing them. As Moody’s noted, the “under-investment over the last 15 years, especially in electricity and logistics will require time to rectify”.

Chart 3: Real economic and fixed investment growth

Source: Stats SA

Fixed investment should pick up in line with higher business confidence and in particular as infrastructure investment opportunities open up.

The positive news relates to the green shoots in consumer spending. Again, the third quarter is too soon to see the impact of lower interest rates, but real household spending was positive, buoyed by falling inflation. More recent data, such as vehicle sales numbers for October and November, and initial (unofficial) reports on Black Friday sales certainly point to consumers loosening the purse strings. Pension fund withdrawals under the new two-pot system are also more likely to reflect in fourth quarter data than in the third quarter.

Better growth ahead

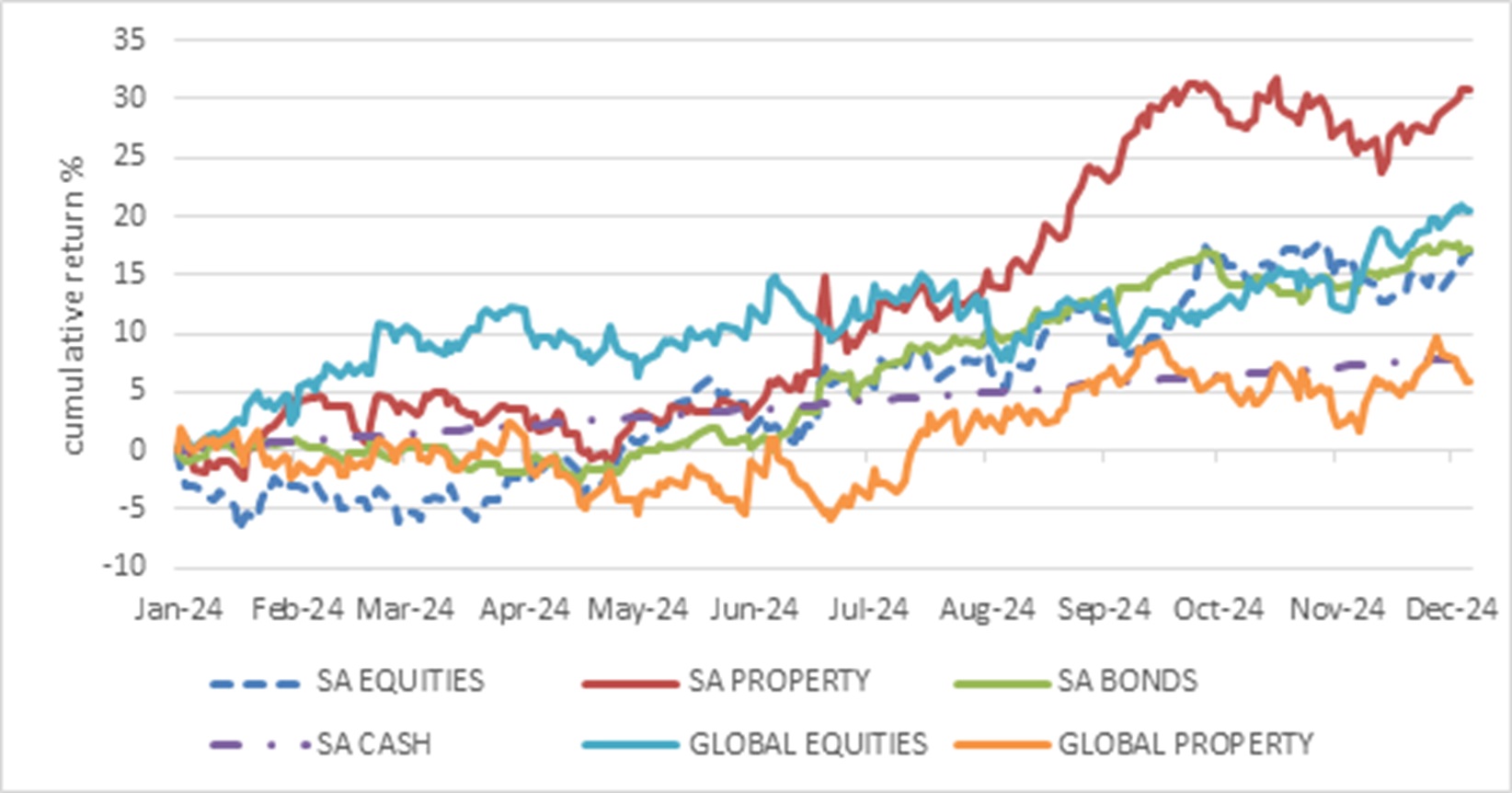

Despite the disappointing headline number, which will drag down 2024 calendar year returns, the outlook for better growth in 2025 remains unchanged. The consensus forecast is 1.7% for 2025 and 1.9% for 2026, according to the Reuters poll. This is still low by emerging market standards but would represent a major improvement from the sub-1% growth trend of the past decade. It would also allow for the further unlocking of value from domestic investments.

Chart 4: Asset class returns in 2024

Source: LSEG Datastream

In other words, patience will still be required. Yet, despite the uncertainty, surprises and moments of angst over the past 11 months, 2024 has shaped up to be a good year for domestic investors. With inflation averaging 4.5% this year, we are looking at double-digit real returns from global equities (in rands), local equities and bonds. In the case of the latter, it is shaping up to be the best calendar year in the past two decades. Coming off a low base, local listed property returns have also shot the lights out.

We shouldn’t expect 2025 to repeat these returns, since markets don’t move up in straight lines. In fact, long-term returns are made up of a few excellent years, interspersed with many slow years, and a handful of really bad ones. To capitalise on the bumper years requires sitting through the bad and the boring. But there is still juice to be squeezed from local bonds, equities and property given current valuations and the prospect for improved domestic fundamentals over the medium term, as discussed above. The same cannot be said for global equities, where a lot of good news is already priced in, and valuations are trading well above long-term averages. However, this is largely down to the richly valued and highly concentrated US market. Exclude the US, which is hard, since it accounts for 66% of global equity market capitalisation, and the rest is mostly fairly valued. Valuation is a useful guide to long-term return expectations but tells us nothing about the next 12 months. Anything could happen in 2025. That is why diversification will remain important, as always.

Wishing you a safe and peaceful festive season. This note will return early in the new year.