Izak Odendaal, Investment Strategist at Old Mutual Wealth

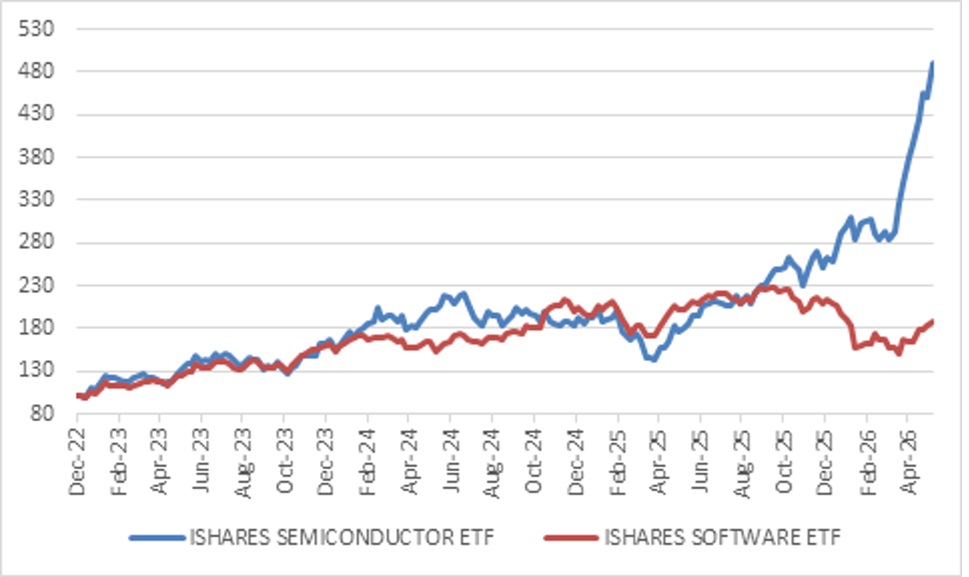

The artificial intelligence (AI) capex boom provided an important boost to global economic activity, offsetting some of the drag from elevated oil prices. It has certainly driven stock markets higher, although the list of beneficiaries seems to be narrowing. As chart 1 shows, it is not entirely correct to talk about a “tech” boom anymore, since semiconductor shares have increasingly diverged from software companies. The latter have come under pressure amid concerns that their business models could be disrupted by AI. For the producers of semiconductors (microchips), on the other hand, the gains have been nothing short of spectacular. Demand for microchips has been exceptionally strong as hundreds of billions of dollars are invested into datacentres and related AI-infrastructure.

While many fear that a bubble is blowing, this is not a bubble in the narrow sense. Semiconductor companies have experienced rapid profit growth, unlike the dotcom bubble of the 1990s, when expectations became completely detached from underlying profitability. However, it can still be a bubble in a broader sense. If the datacentre build-out were to stop tomorrow, for whatever reason, the demand for semiconductors will drop dramatically. Although it’s hard to imagine this now, it has historically been a highly cyclical industry.

Chart 1: Tech hardware versus software performance

Source: LSEG Datastream

It is very difficult to know if enough, too few or too many datacentres are being built today. It will ultimately depend on how businesses and consumers use AI and how much they are prepared to pay for it. It also depends on how disciplined the builders of this infrastructure are in matching supply with real demand. For instance, past real estate cycles show that more speculative construction takes place the longer the good times last. Similarly, later stages in commodity cycles are usually characterised by the development of low-quality, high-cost mines as current strong demand is projected into the future. While technology evolves, human nature does not.

What is beyond doubt is that concentration risk has increased. There are at least three dimensions to this. Firstly, it is well known that the S&P 500 has become more concentrated, with the top 10 stocks making up a larger share of market value than in the past at around 40%.

A different way of showing it is looking at the outperformance of the S&P 500, which is weighted by market capitalisation so bigger stocks count for more, against an equal weighted version, where each share accounts for 0.2% of the index, as shown in chart 2.

Chart 2: S&P 500 market cap weighted vs equal weighted

Source: LSEG Datastream

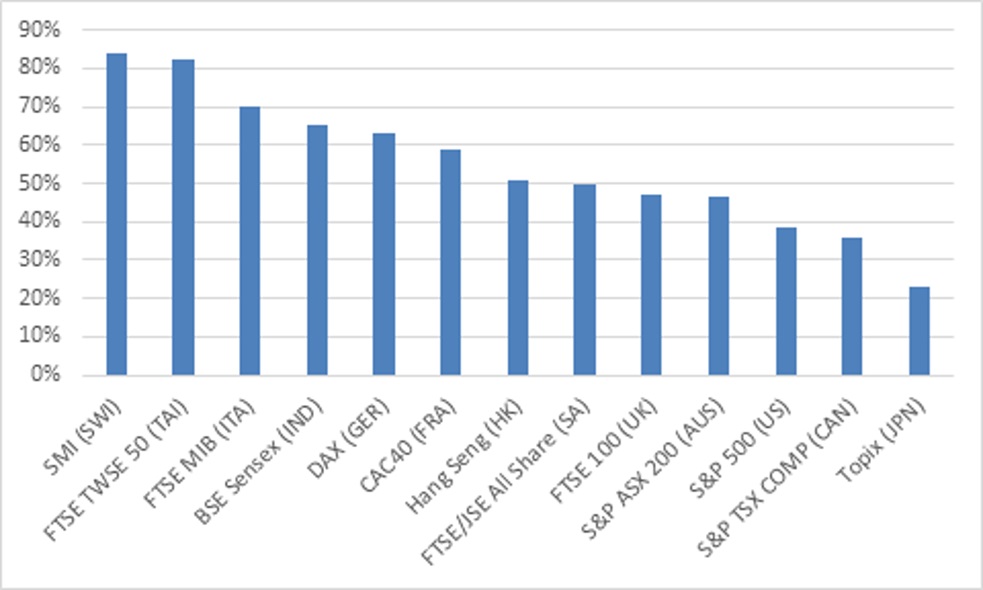

Concentration is not unique to the US. Indeed, the S&P 500 remains one of the least concentrated country stock indices. On the FTSE/JSE All Share, for instance, the top ten counters make up around 50% of market value.

Chart 3: Top 10 companies share of national index market value

Source: FTSE, BlackRock, S&P, LSEG as at 31 January 2026

The main problem with the concentration in US markets is the increase over time, and the fact that it spills over into global equity benchmarks. While the US share of global economic activity has remained steady at around a fifth in recent decades, its weight in benchmarks produced by MSCI, FTSE Russell or others has increased to around 63%. Over the next few months, it is expected that OpenAI, Anthropic and SpaceX will list on US markets, with a value of between $3 and $4 trillion between them. This will further increase the concentration of the US market and the share of the US global benchmarks.

Concentrated markets are not necessarily expensive, with the JSE as an example. However, a rapid increase in concentration is often based on sentiment and expectations of future growth, in other words rising price: earnings ratios. If reality fails to meet those expectations even slightly, prices can fall. Even if there is no sharp decline, long-term upside is limited if the good news is already priced in. At current valuations, the long-term return outlook for the S&P 500 seems muted.

Rising stock market concentration is often – though not always – driven by a single underlying factor. When the oil price hit $150 per barrel in mid-2008, it was no surprise that four of the top 10 most valuable global companies were oil majors. The problem is that the oil price more than halved over the next year. When a single theme underpins such a large portion of total market value, any repricing of that theme can cause trouble. This is the case today with the AI theme, particularly the circular nature behind some of the massive profits that are being, for instance, when Microsoft buys Nvidia chips and sells cloud computing services to OpenAI, while also owning a small stake in OpenAI.

The worst episodes of stock market concentration go back to the railway booms of the 19th century, when railway companies made up 50% to 60% of the market value of London and New York Stock Exchanges. When boom turned to bust, the damage was significant. The analogy with the current age is notable. Railways were one of the most transformative technologies ever and fundamental to economic development all over the world, but often not a win for the initial shareholders. There were at least three major crashes (1847, 1873 and 1893) and typically only investors who picked up railway stocks and bonds at pennies to the dollar afterwards made good money.

Alpha agonies

As large companies become bigger components of the main benchmarks, it is very difficult for active managers to generate “alpha” by outperforming the benchmark without taking excessive risk or completely ignoring benchmark weights. There are also regulatory limits on single stock exposure in many cases. In South African collective investment schemes (unit trusts, or mutual funds as they are known in other countries), a manager may not invest more than 10% of the fund in a single share. This limits the ability of a manager to have an overweight position in a large share relative to the benchmark. A decade ago, Naspers was not only the biggest stock on the SA market, but also the fastest growing one. However, active managers in collective investments were not allowed to match the benchmark weight of Naspers, let alone be overweight until the JSE introduced capped indices.

Supply chain risk

The second type of concentration risk is in AI supply chains, which are dominated by a handful of firms and countries. Taiwan and Korea are the leading suppliers of advanced semiconductors. The global AI supply chain runs through the Taiwan Straits and the Korean Peninsula, two of the world’s geopolitical flashpoints. The other Strait that has been in the news of late, Hormuz, is also a factor since helium is used in the production of advanced chips, and Qatar supplies around a third of the world’s helium. Nonetheless, a war in Taiwan or Korea could be more economically damaging than the war in the Persian Gulf, given that semiconductors are not just crucial for AI, but many aspects of ordinary life (a humble dishwasher will contain dozens).

In this context, the Financial Times reported last week on a draft European Union law that would allow intervention in Europe’s semiconductor supply chains during times of shortages, including forcing suppliers to break existing contracts. The biggest manufacturer of the lithography machines used to produce chips is Dutch-based ASML, but Europe only produces about 10% of global semiconductors and anxiety is growing about its dependence on the foreign suppliers. This anxiety also exists elsewhere and was behind the 2022 CHIPS Act to stimulate semiconductor manufacturing in America. The US also blocked exports of high-end chips to China. Last year, the Trump administration took a 10% stake in struggling chipmaker Intel. It will not be hard to see governments intervening even more forcefully in future to secure the supply of these tiny but crucial components.

Concentration of power

A third kind of concentration doesn’t reflect on fund fact sheets or portfolio statements. One of the defining images of the second Trump inauguration was the row of tech CEOs seated behind the President. They spent a lot of money to be there, not necessarily with altruistic motives. Companies will always try to engage governments on desired policies, and indeed they have both a right and a duty to do so. However, there is a line between where corporate influence of public policy is no longer benign, and at its worse, becomes a form of state capture, where big companies write the rules for themselves. There are political, social and economic consequences to the concentration of power in the hands of a few corporations.

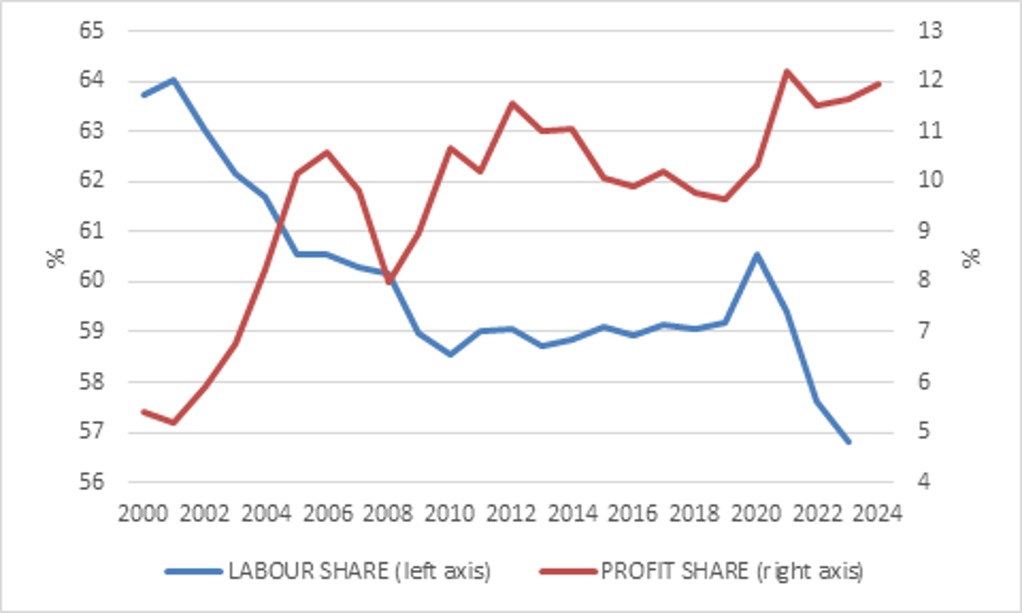

The flipside of this increased concentration is inequality. Corporations have taken an increased share of national income (GDP) in the US and other developed countries. This is good news for shareholders, including ordinary workers through their pension funds, although increasingly the ownership of companies has also become more concentrated. According to the Federal Reserve, the top 1% of households hold 36% of financial assets in the US, up from 25% in 1990. Rising inequality clearly long predates AI, but it risks increasing the wealth gap if there are widespread job losses while the benefits flow to the owners of the AI firms, already the biggest in the world.

Chart 4: US shares of national income

Source: LSEG Datastream

There could be a more optimistic outcome, as many have argued, where the benefits of AI are spread widely, for instance by lowering the barriers to education. This happy scenario is probably not good news for a concentrated stock market. The more “democratic” AI becomes, the less likely it is to be profitable for the current handful of leading firms, and the more likely it just becomes a commodity. Electricity, for instance, underpins both the modern economy and a quality of life that was undreamed of by even the richest in the world 150 years ago. But it has very much gone from a technological marvel to a commodity, and the economic benefits largely accrue to the users, not the providers of electricity.

Even the Pope weighed on these concerns in a new encyclical, Magnifica Humanitas. His warnings were largely in the philosophical realm, namely that we shouldn’t equate AI to human intelligence, nor should we forget that AI lacks any moral foundation and should not be allowed to substitute for human judgement in life-or-death decisions. More relevant for our purposes, however, he warned against technological infrastructure and algorithms being “concentrated in the hands of only a few people” leading to a widening gap between haves and have-nots.

For now, a large degree of pessimism seems to prevail. A headline in the Wall Street Journal two weeks ago warned that “The American Rebellion Against AI Is Gaining Steam”. It recounted how former Google chief executive Eric Schmidt was recently booed at a university commencement address when he waxed lyrical about AI. Opinion surveys reflect this negativity, more so in the case of Americans, perhaps because they can see how the leading AI firms have close access to Trump’s administration.

From a purely investment point of view, the risks run in two directions. The first is that the rich and powerful tilt the rules further in their favour and to the disadvantage of others, smothering competition for instance, or weakening shareholders’ rights (something that is already visible in the SpaceX listing prospectus).

However, there is an equal and opposite risk of a massive social and political backlash. Despite their wealth and influence, a tech billionaire still only has one vote in a democratic election. While AI will not necessarily dominate the upcoming November midterm elections in the US, it is not hard to see it on the ballot in major democracies in the years ahead. Forced breakups of companies, nationalisation or just tougher regulations could follow, with clear negative implications for the market values of these firms. Granted, this seems unlikely today. The Trump administration has gone out of its way to reduce guardrails for AI companies, but the mood is shifting.

Diversification benefits

The obvious anecdote to concentration is diversification. This can be more challenging when different asset classes are all exposed to the same theme. For instance, while the AI build-out was initially financed out of cashflows, it is increasingly being funded through debt, meaning that the corporate bond and private credit markets are also now exposed. Emerging markets equities are also tilted towards the AI theme, with three semiconductor companies namely TMSC, Samsung Electronics and SK Hynix now accounting for almost a quarter of the MSCI Emerging Markets Index.

The challenge is not insurmountable, however. For South African investors, the local stock market has little meaningful AI exposure and local interest rates are attractively high. It also creates opportunities for active management to find attractive stocks in less glamorous sectors, though the benefit might only be visible in the future. As noted, active management will struggle when a concentrated market rallies but should outperform when the inevitable correction arrives. The problem is that it is impossible to know when this happens or what the catalyst will be. The sensible approach is to position portfolios to be robust in a range of different scenarios, guided by valuations. The world is changing rapidly, but the basic recipe for investment success has not.

ENDS